By JOACHIM KLEMENT

Fund managers around the world are increasingly facing new regulations that will require them to disclose more information on the climate-related risks of their investments, as well as their fees and charges.

Talking to both fund managers and executives of businesses on these disclosure regulations, I encounter all kinds of reactions ranging from “I don’t have time for this. It makes no sense and is just an additional burden” to “Great, let’s get ahead of the crowd and be transparent about our fees and climate-related risks before everybody else does.”

As an investor, I always prefer more transparency, but from the perspective of a fund manager or a company executive, does it really make a difference to be more transparent? In a word: yes.

New research from Japan

That is the conclusion from a new set of experiments by Satoshi Taguchi and Yoshio Kamijo who asked people to participate in a set of trust games. In these games, participants (investors) were asked to hand over a portion of their money to another person (the executive) who uses this money to invest in a project. The executive can get either a high return or a low return on this project. Once the return has been achieved, the executive can then decide how much money to give back to the investors (i.e. how high the dividend should be).

The interesting thing is that the level of productivity and thus the return of the investment of the project is only known to the executive. Thus, the executive can either decide to not disclose the level of productivity of the project or voluntarily disclose the level of productivity of the project. Naturally, if the executive knows that the project doesn’t create high returns, she is likely to not disclose that information and if the executive knows that the project is going to be highly profitable, she is likely to voluntarily disclose that information to the investor.

However, the researchers also used some modifications to create other states. First, they simulated a situation when the information about the productivity of the project would be unintentionally disclosed (i.e. through an information leak) or situations in which the executive could not choose to disclose or the information, good or bad, had to be disclosed to the investor. Finally, in a fifth setting, the investors could ask the executives for the information and the executives could then voluntarily disclose the information based on the demands of investors.

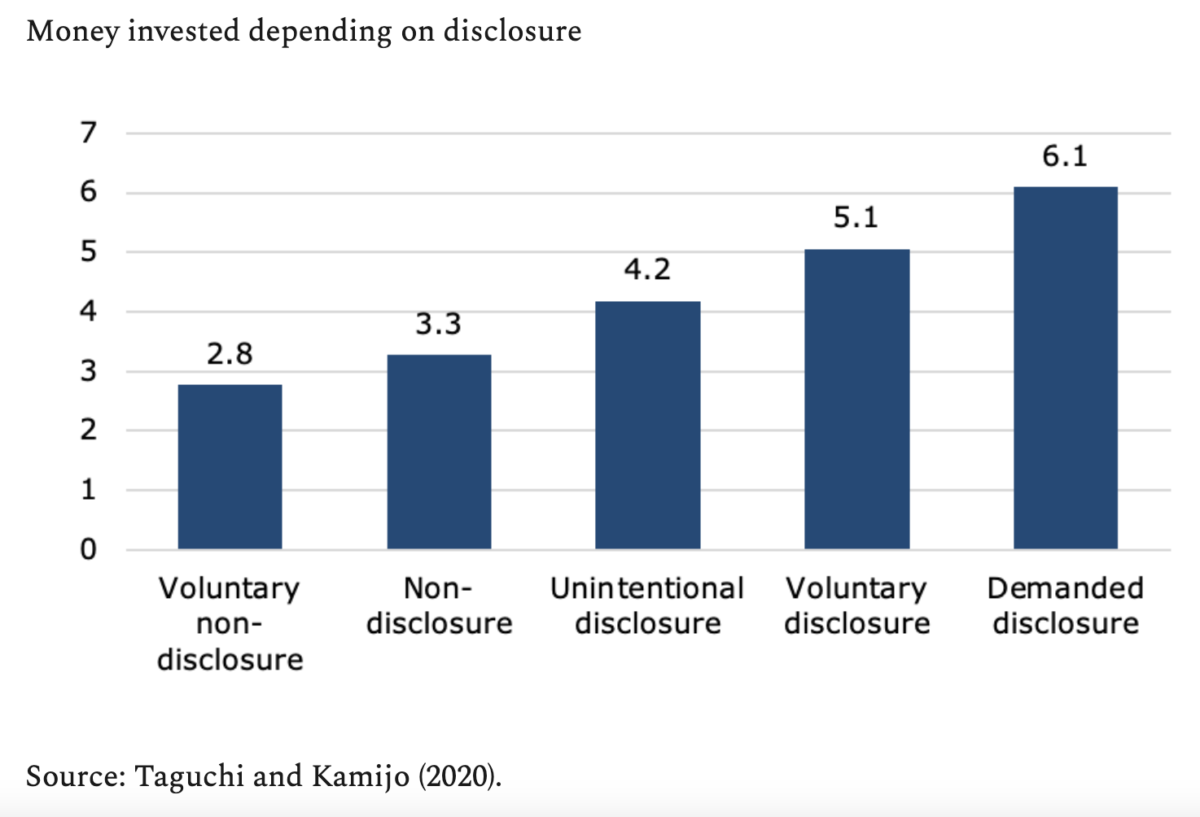

The chart below shows how much money of their initial endowment of ten units the investors chose to hand over to the executives.

Greater disclosure, higher investment

Note how trust in the executive builds up, the more transparent the executives become, and the more information they disclose to the investor. If the executive refuses to disclose vital information about the project, investments are low. If the executive cannot choose to disclose or not disclose the information investment gets a bit higher. It is a situation where investors are willing to give executives some benefit of the doubt and thus invest a bit more.

But note how investment increases once information about the project is disclosed. If the disclosure is unintentional (e.g. mandated by regulators) investments already jump compared to the situation where the information is not disclosed. But executives who voluntarily disclose the information receive an even bigger share of the portfolio of the investors.

Finally, if the investors ask for information and executives then voluntarily disclose it, investments are highest.

Transparency builds trust

What is going on here? In basic terms, deeper interactions between investors and executives build a deeper level of trust. By virtue of these interactions of asking for information and then receiving it, an additional layer of trust is built which drives higher investments.

Unfortunately, most investors never dare to ask for vital information or don’t have access to executives or fund managers to ask for it. Thus, the best course of action for fund managers and executives is to voluntarily disclose information about their businesses and funds.

The basic rule here is the more you disclose, the more your investors will trust you, and the more money they will invest.

JOACHIM KLEMENT is a London-based investment strategist. This article was first published on his blog, Klement on Investing.

Joachim is a regular contributor to TEBI. Here are some of his most recent articles:

Another sign that market efficiency is increasing?

How hard is it to find the next Amazon?

Practitioners still pay too little attention to academia

Stocks have lagged bonds since 1970. Why?

No more room at the factor zoo

Boohoo teaches ESG investors a lesson

WHAT TO READ NEXT

If you found this article interesting, we think you’ll enjoy these:

Social trading platforms are bad for your wealth

How “Britain’s Buffett” lost the plot

How predictable are government bond returns?

A lost decade for endowment returns

OUR SISTER BLOGS

If you’re a financial adviser or planner and you enjoy TEBI’s articles, why not try our sister blogs, Adviser 2.0 and Evidence-Based Advisers?