Small-cap stocks essentially come in two varieties — small growth and small value. So which type of small-cap has historically produced higher returns? As LARRY SWEDROE explains, there is a very clear winner.

Charles Dickens’ novel A Tale of Two Cities opens with “It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness, it was the epoch of belief, it was the epoch of incredulity…”). This passage suggests an age of radical opposites taking place across the English Channel, in France and the United Kingdom, respectively.

Since the beginning of 2021, the universe of U.S. small-cap stocks has also been a tale of two opposite universes as the bubble in small growth companies (companies with high prices to value metrics like earnings, book and cash flow) with high growth in assets and poor profitability burst.

Historically, such stocks have provided poor returns. Yet every so often a mania develops built around some “this time is different” story, and these stocks have provided a short burst of spectacular returns when investment sentiment leads to speculative excesses — and the inevitable bad ending (we just don’t know when).

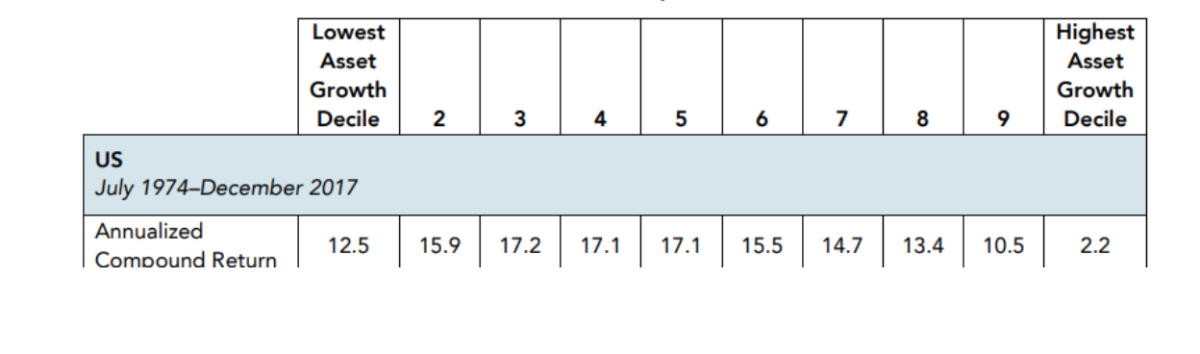

As an example, in 2018 the research team at Dimensional examined the performance of small stocks over the period 1974-2017 and found that small stocks in the highest decile of asset growth returned just 2.2 percent per annum, underperforming riskless T-bills by 2.5 percentage points per annum for more than four decades! They also underperformed small stocks in general in 81 percent of the years:

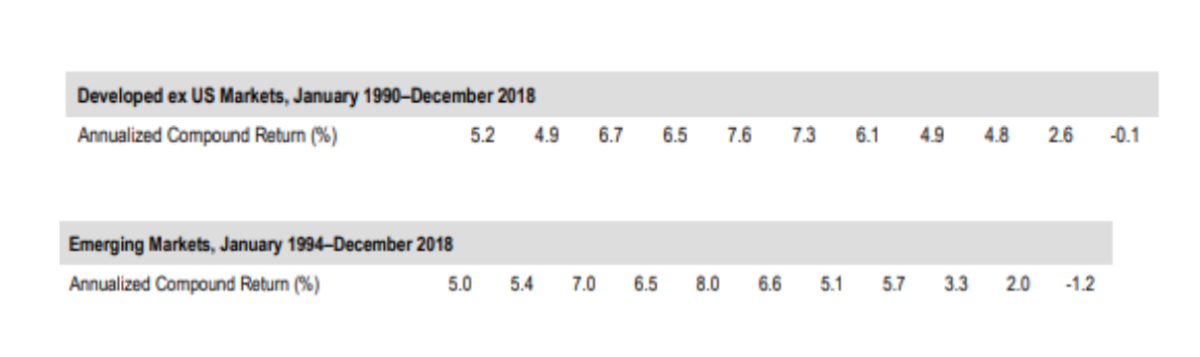

Similarly, poor results were found in international and emerging markets:

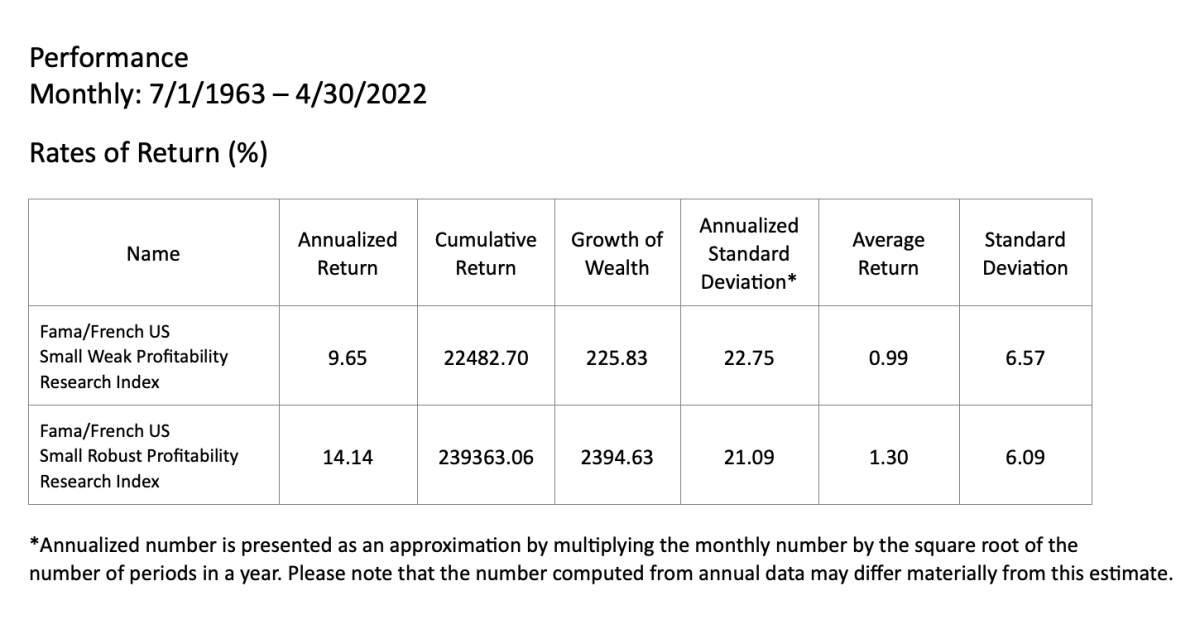

In terms of profitability, over the period July 1963-April 2022, the Fama-French U.S. small weak profitability research index underperformed the small high profitability research index by 4.49 percentage points (9.65 versus 14.14) and did so with even greater volatility.

The evidence suggests that investing in small-cap stocks without screening for profitability or investment is imprudent. It is also why Dimensional includes such screens in their fund construction rules.

One of my favourite expressions is that there is nothing new in the world of investing, only the investment history you don’t know. Speculative manias such as we have seen in biotech, dot-com stocks and “disruptive technology” stocks like those owned by the ARK Innovation ETF have always ended badly. Investors, on average, buy in well after the mania had begun and sell well after the rout was underway. In other words, investor returns in such assets tend to underperform the very vehicles they invest in. With that in mind, let’s take a look at what has happened since the beginning of 2021.

Recent evidence

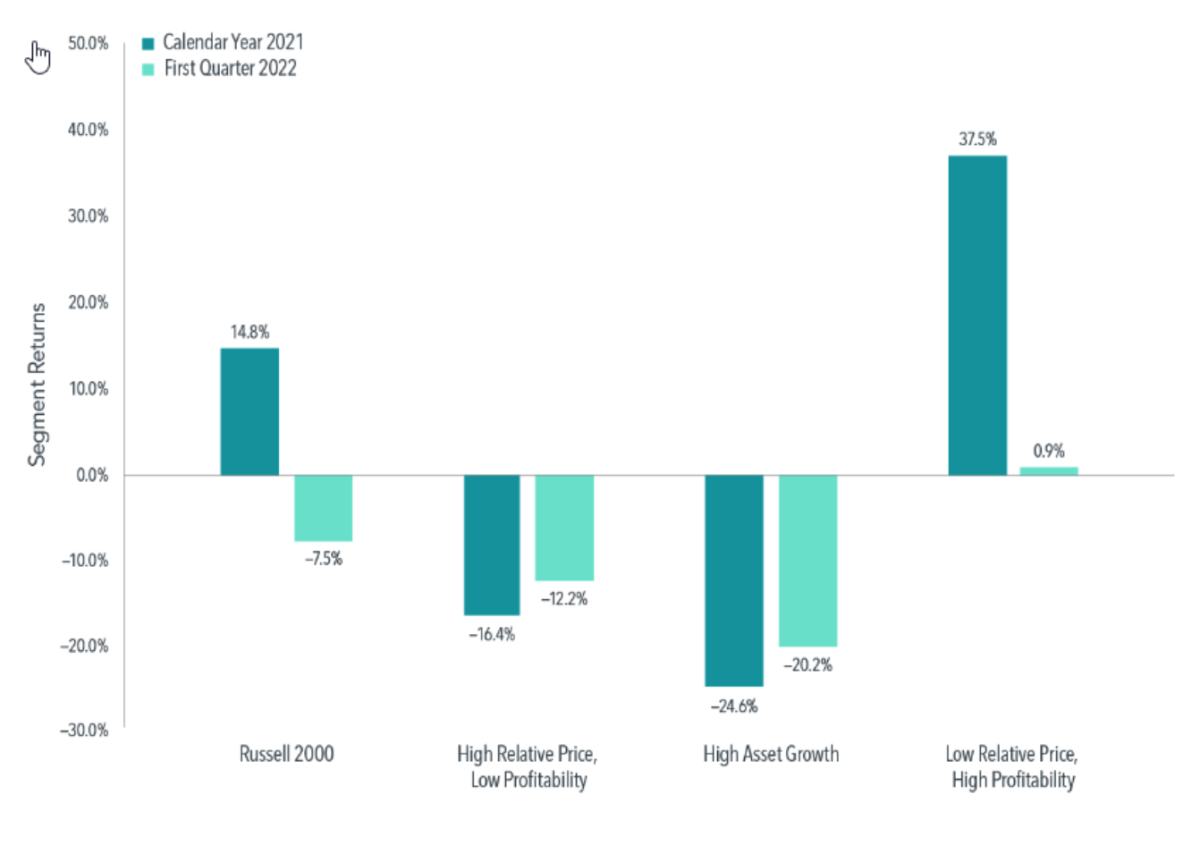

For those who do know their investment history, “it’s déjà vu all over again,” as Yogi Berra said. The following table provided by Dimensional shows the returns of small stocks across the factors of investment and profitability. Note the familiar tale of two small-cap universes during 2021 and the first quarter of 2022.

Source: Dimensional Fund Advisors

Anomalies persist

The poor performance of small growth stocks with high investment and low profitability is an anomaly that should not exist if markets were perfectly efficient. Markets are highly efficient, but not perfectly efficient, due to what are referred to as “limits to arbitrage.” To correct undervaluation, all an investor has to do is buy, with losses limited to the investment (assuming no leverage). However, there are four key limits to arbitrage that prevent sophisticated investors from correcting what they perceive to be obvious overvaluation:

- Many institutional investors (such as pension plans, endowments and mutual funds) are prohibited by their charters from taking short positions.

- The cost of borrowing a stock in order to short it can be expensive, and there may also be a limited supply of stocks available to borrow for the purpose of shorting. This can be especially true for small growth stocks, which tend to be disproportionally owned by retail investors, while it is institutional investors who provide most of the loans available in the securities lending market.

- Investors are unwilling to accept the risks of shorting because of the potential for unlimited losses. The recent GameStop short squeeze episode provided a reminder.

- Short sellers run the risk that their borrowed securities are recalled before the strategy pays off. They also run the risk that the strategy performs poorly in the short run, triggering an early liquidation.

Taken together, these factors suggest that investors may be unwilling to trade against the overvaluation of securities, allowing overvaluation to persist more than underpricing.

Investor takeaway

Over the long term, it is clear that small-cap growth stocks with low profitability and/or high asset growth tend to underperform. They underperform for very simple, logical reasons provided by valuation theory — paying a lot for a company that earns little profit or requires frequent investment is a good sign of a low discount rate and therefore a low expected return. By comparison, paying less for more profit indicates a higher discount rate and expected return.

While active small-cap managers try to pick a handful of winners from thousands of small-cap companies, the evidence demonstrates that doing so is a loser’s game — while it is possible to win, the odds of doing so are so poor it’s imprudent to try, as the annual SPIVA scorecards demonstrate. Instead, buying into the small-cap market while screening out what we might call “the black hole of investing” (small growth stocks with high investment and low profitability) can improve expected returns while still allowing investors to maintain a well-diversified portfolio. That is the strategy employed by such fund families as AQR, Avantis, Bridgeway and Dimensional.

Since I don’t know of any investor with a clear crystal ball, the prudent strategy is to allow the empirical evidence and valuation theory to be our guides, avoiding getting caught up in investor sentiment that leads to bubbles and their bursting. Over the long term, investors who focus on paying less and getting more profitability have the greatest odds of achieving their financial goals.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, but its accuracy and completeness cannot be guaranteed. Mentions of specific securities should not be construed as a recommendation and are only for informational purposes only. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements, or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability, or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products, or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this article. LSR-22-311

LARRY SWEDROE is Chief Research Officer at Buckingham Strategic Wealth and the author of numerous books on investing.

ALSO BY LARRY SWEDROE

What insider trades (and non-trades) tell us about future returns

Trading driven by attention leads to poor returns

The takeover effect: what it is and how to benefit

Generating alpha sows the seeds of its own destruction

Index investing: Is replication or sampling best?

VIDEO MARKETING FOR ADVISERS

Through our partners at Regis Media, TEBI provides a wide range of high-quality video content for financial advice and planning firms.

For firms in the UK, we can either come to you, or you can come to Regis Media’s studios in Birmingham, where we have a full white-screen set-up with lights and autocue. For firms outside the UK, we’re happy to talk through the options with you.

If it’s educational content you’re looking for, we have more than 200 pre-produced videos which can be tailored to include your branding, contact details and call-to-action.

Interested? Email Robin Powell, who will be happy to help you.

© The Evidence-Based Investor MMXXII