Few people have a better grasp of financial history than RUSSELL NAPIER, Keeper of the Library of Mistakes in Edinburgh.

We had an excellent response to Part 1 of my interview with Russell, and I suspect you’re going to enjoy Part 2 even more.

In it we explore some fascinating questions: What’s the most important lesson that financial history teaches investors today? How sure can we be that stock markets will stay on an upward trajectory over the long term? What causes market bubbles? Can anything be done to prevent them? And is there any way of spotting them in advance?

We also address a thorny issue for those, like me, who generally feel comfortable putting their faith in the wisdom of the market: Why, if markets are broadly efficient, do we see such wild fluctuations in prices from time to time?

Finally, though we don’t normally touch on macro-economic issues on TEBI, we’ve made an exception on this occasion. Russell has some interesting views on where the global economy may be headed.

Russell, it’s your view that financial history teaches investors valuable lessons. Presumably the most important of all is to diversify? Asset classes, countries and sectors go in and out of favour, but if you’re well diversified, and patient, you can be fairly confident of a positive outcome.

Yes, certainly for the investor, absolutely 100%, that’s the most important thing you can do as a lay investor. You simply won’t have the expertise to go and find the new Facebook. There may be some real genius investor who spends his entire life doing this sort of thing, who has that skill. But for the layman, that isn’t an option.

People sometimes ask me, “What is the number one book to read on finance?” My answer is Triumph of the Optimists by Dimson, Marsh and Staunton. It’s a road map of the historical returns from equities, bonds and cash over a very long period of time. And it allows you to work out what has been a reasonable return and an unreasonable return — in other words, what you can expect from a market and what you can’t expect from a market. I think the simple answer is that, as a layman, you need to diversify. And not just between equity markets, but between asset classes; I think that’s often forgotten.

They called that book Triumph of the Optimists because, generally speaking, the winners in the 20th century were the optimists who put their faith in equities despite huge recessions, world wars, the nuclear arms race and so on. Is there a danger that 21st century will see the pessimists triumph?

Highly unlikely. All that investors need to know is what the long term is. Once they know what the long term is, they can adjust accordingly. The long term, I think, is 18 years. For US equities, there’s never been a period over 18 years when we didn’t have a positive real return, with dividends reinvested.

The problem is that most people, when you say long term, think four or five years. Some may stretch to eight or nine. But there’ve been prolonged periods when equities have not delivered you a positive real return.

Some societies fail, Russia being the prime example in the last century. If you’d been in Russia, investing in the Russian stock market during their revolution, you would have lost your money. Many, many markets in 20th century closed because assets were sequestered by political regimes.

So Triumph of the Optimists is definitely about how equities always outperform in the long run, in societies that survive as societies orientated towards private ownership. It’s a fantastic lesson for investors, but you have to understand what the long run is. It can be a very long period indeed.

You mentioned 18 years, but some investors don’t have that long to wait.

Of course, the younger you are, the more you can accept equity risk. You shouldn’t be concerned too much about volatility when you’re young. In other words, you don’t have to cash in your chips at the wrong time. If things are going wrong after ten or 15 years, you can keep accumulating equities. And as Triumph of the Optimists shows, that will be a winning strategy, as long as it’s in a jurisdiction where private property ownership continues.

Clearly, if you’re 70, you may not have 18 years to wait, so your asset allocation has to shift as you get older. So the long run does differ depending on how much time you’ve got left. How long your long run is will make a difference to what your portfolio should be.

You mentioned earlier that the lesson of Triumph of the Optimists is that equity markets always go up over the very long term. But how sure can we be about that?

Fortunately, I’ve written a book on that. It’s my field of expertise. I’ve looked at the four occasions, admittedly only in the US ,where equities were incredibly cheap, which was 1921, 1932, 1949 and 1982. What happens with equities is that sometimes they get so cheap that there is virtually only one way for them to go, which is up. And what I discovered in the research for that book is that ultimately they get cheap because of deflation — not world wars, not nuclear armageddon, not bird flu, but the risk of deflation.

Those who’ve read about the 1929-1932 period will know that deflation threatens reduced corporate cash flows and the eradication of equity. Corporations become bankrupt. That’s what you have to fear most of all. In 2007-2009 clearly that is what we were worried about; that’s why equities got so cheap.

So the history of a nation which holds itself together as a private property owning nation is that sometimes the pain of deflation is so much that you can expect a remedy. The remedy we’ve just had is quantitative easing. The remedy we had in 1982 was to abolish money supply targeting. The remedy after World War 2 was to create more inflation to try and shift government debt. So societies find a remedy to too much economic pain. And if equities are cheap, then you buy them.

I can’t forecast the likelihood of a nuclear war. But I can tell you this: if there was one, you wouldn’t be worrying about your portfolio.

As you say, patient, long-term equity investors prospered in the 20th century. But they had to withstand some major crashes along the way. Are equity bubbles inevitable?

There are books and books written on this subject, so I’ll try to be brief and generalise as much as possible. The reason why we get equity bubbles is that we believe in a permanent combination of two things, which has always so far proved to be an illusion. The illusion is that interest rates will stay low and growth will stay high.

The current value of an equity is the present value of its discounted cash flows. If anyone plays around with these numbers on a spreadsheet and you put it in a really low discount rate, and a really high growth rate for earnings and dividends, you’re going to get a very high net present value, and that is how we get bubbles.

They don’t happen at the top of every business cycle. Investors have to see something which they believe is so structurally different that we can have these two things combined, and that’s where we are today. People look at the immense improvements in technology, they look at Amazon, and they look at all the things that are likely to keep inflation low, but growth high. And they conclude that this is sustainable. And all I can tell you is that there is no evidence that this is true.

The technological transformations of the UK and US over the last 150 years have been truly, truly immense. Each one of those technological transformations is deflationary in nature; it brings the price of things down. And yet over that long period of time, we have always had inflation coming back up again somewhere along the line.

Therefore that combination which gives you the bubble, thinking interest rates can stay low forever, and corporations can go on making profits forever, is an illusion. That is an important lesson: we have to realise that this isn’t going to go on forever.

And the second thing that contributes to bubbles is just the amount of leverage, the amount of debt. When you believe something has structurally changed, the temptation to add on so much more debt and asset price speculation becomes absolutely overwhelming. There is more we could do on that front to try and stop that from happening. We can reduce the amount of leverage that’s permissible, so that when these assets decline, the whole stability of the financial system doesn’t also crumble.

But as to how you stop the population en masse believing that we live in a new economy, with permanently lower interest rates and permanently higher growth rates, I’m not sure you can do much about that.

From an investor’s point of view, it would be extremely helpful to have some sort of clue as to when one of these events is about to happen. But they’re very difficult to predict, aren’t they?

That’s right. I wrote a book about the bottoms of markets and trying to identify them, and I’ve come up with some things that I think are useful for that. But the tops, I think, are much, much, much more difficult.

At the end of the day, at the bottoms we’re talking about an issue of value. We’re talking about cash flows and dividend yields. We’re talking about net present values that looks attractive, particularly if growth stabilises — just stabilises, it doesn’t even have to grow. At the top we are talking about a form of mass mania, a belief in that combination of stable and ever-low interest rates and high growth. It’s incredibly difficult to work out when it’s over, so I’m delighted I didn’t write a book about where the tops are.

But here is one thing I have to help on that. It’s not my advice; it’s the advice of someone who teaches on my Practical History of Financial Markets course. His name is Gordon Pepper, and he started in financial markets I think in 1961. He’s in retirement but he is still teaching. Having witnessed many, many of these bubbles, this is his advice: rationally assess how long you think this overvaluation can last, double it and take off a month.

The Library of Mistakes is full of books that try to tell you how to know when you’ve reached the top of the market. But I think that advice from Gordon Pepper is as accurate as we are going to get in terms of the tops. They are so much more driven by crowd psychology that I think it’s incredibly difficult to call the the tops. Having failed to do it myself a few times, I’m even more convinced that it’s difficult.

Apart from crowd psychology, markets are also driven by the aggregated information of lots of very clever people around the world. By taking a view that a market is overheated or whatever, you are actually expressing an interest or opinion that runs counter to collective wisdom of millions of people.

Sure, and that’s often been the correct thing to do. Not just in finance but in many things in life, it’s often being the correct thing to do, to take the opposite side of the aggregated opinions of millions of people. We’d better avoid politics, but I think politics is a pretty good example of that.

Maybe most of your blog’s readers viewers don’t believe in active management. If so, they probably side with Eugene Fama. But if you believe that human beings can get over-excited, then you do want to be selling things when the whole world thinks they can only go up. And you do want to be buying things when the whole world thinks they can only go down.

So if Fama was right and we were indeed homo economicus, if we were indeed entirely rational, then the coming together of all those people would give us the right answer.

So there are two different types of crowd, and I think it’s important to distinguish between the two types. There’s the type of the crowd where we are all in a room together and we are in a feedback loop, and there is another type of crowd where we are not in that feedback loop and we are all independently making decisions. When we are all independently making decisions, as a sort of weighing machine, perhaps there is significant value in that. When we are all in a room together, we can all persuade ourselves of anything; that’s what Charles Mackay referred to in his 1841 book, Extraordinary Popular Delusions and the Madness of Crowds. There’s a feedback loop there, and that is what a stock market is.

So there is no point in pretending that it’s the other type of crowd, that we are all independently making these great calculations and weighing decisions. We are all completely influenced by each other and the direction of prices themselves. So as long as the stock market is that type of crowd, I beg to differ with Eugene Fama as to its accuracy in correctly pricing things.

Generally, then, how worried, or otherwise, should people be about stock market crashes and corrections?

In general, I think it doesn’t really matter if you’re buying things when they’re cheap. So that’s a very simple and easy solution — buy things when there are cheap. The problem is you don’t always get that opportunity. So retail investors should be worried about having a good asset allocation among different asset classes. And when stock markets fall, they shouldn’t be concerned if they own things that are cheap, and they should be very concerned if they own things that are expensive.

So the problem is that we spend too much time looking at the price and not enough time looking at the value. You may remember that Oscar Wilde also had something to say about the difference between price and value.

Equities outside the US are actually reasonably priced. US equities are incredibly overpriced, and incredibly vulnerable to lower valuations. So I think we should be very concerned about equites markets.

If you’re a global equity index investor, more than half of your wealth will be in US equities. The MSCI World Index currently has a 54% weighting in US equities. That’s a good reason to be concerned.

If there’s one thing investors can do, then, to reduce their chances of making mistakes, what would it be?

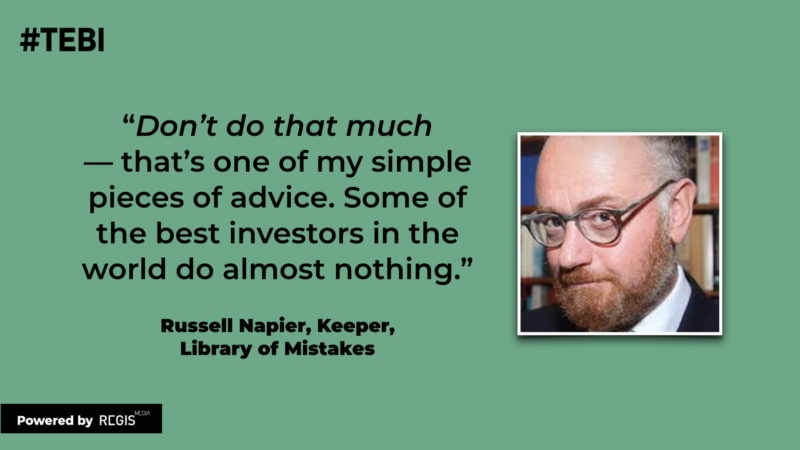

I think the most important thing to do is to try to understand ourselves. It’s very easy to look at the markets and say you need to understand a particular market. I would say every one of the greatest disasters I’ve seen in finance happened because people didn’t understand themselves.

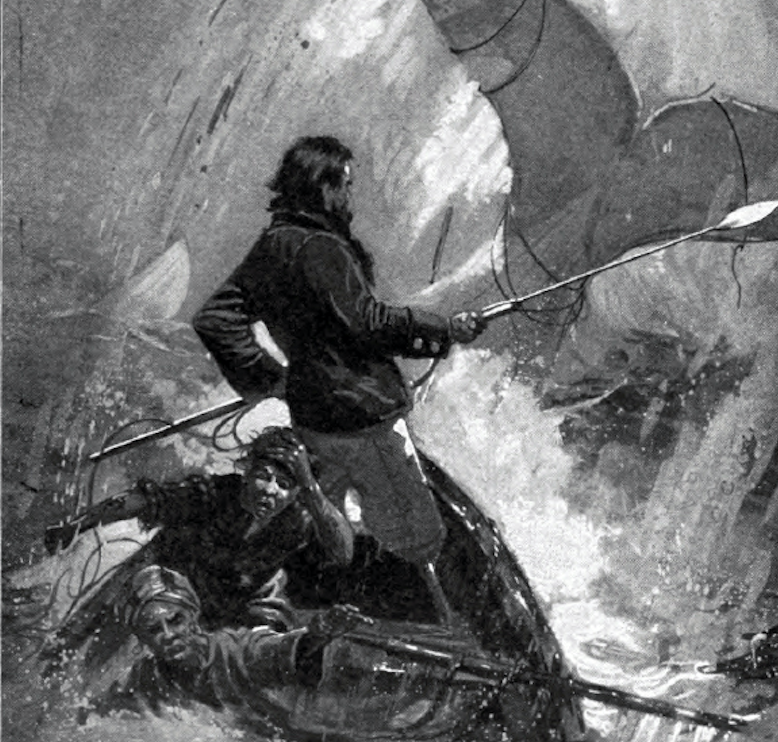

In the Library of Mistakes is we have a model ship called the Pequod, which was Captain Ahab’s ship in Moby Dick. Captain Ahab might have been one of the most intelligent people ever to captain a ship, but he also had some character flaws. And it really didn’t matter how smart Captain Ahab was, because these character flaws meant that he went down with the ship on the back of the great white whale.

What investors have to do is try to calibrate their own risk perspective, realise how much they know and how much they don’t know, hand over those bits to other people, and not get carried away constantly trying to prove that they’re smarter than the market. That is when the great calamities occur, when you try to be smarter than the market.

Don’t do that much — that’s one of my simple pieces of advice. Some of the best investors in the world do almost nothing. So buy things when they are cheap, hold them, diversify across a wider range of assets and markets, but truly try not to do very much at all.

So finally, how should investors go about trying to understand themselves better? And does it require the help of a financial adviser?

Often it does. Spend time finding a good financial adviser, and when you meet that adviser, form an opinion as to their character. John Bogle wrote a wonderful book called Character Counts. Character is as important as intelligence. It’s the easiest thing in the world to say that I want to give my money to the smartest guy in the room. No you don’t, you really don’t want to give your money to the smartest guy. You want to give you money to the guy who has got slightly above-average intelligence, but who has got the right sort of character. Make sure, a) that he has got your interests at heart, most importantly of all, b) that he doesn’t panic at the wrong times, and c) he is not massively overconfident, because the biggest disasters come from being overconfident.

These are the same questions you have to ask yourself when you calibrate yourself for what you’re capable of doing and not capable of doing — not from an intellectual perspective, but from the perspective of character. This all sounds very woolly, and they don’t teach it in finance school, but when it comes to investments, character is incredibly important and ranks at least equally with intelligence.

Missed Part 1 of the interview with Russell Napier? Click here:

Four must-read history books for curious investors

Picture: Illustration of the final chase of Moby Dick by I.W. Taber

Robin is a journalist and campaigner for positive change in global investing. He runs Regis Media, a niche provider of content marketing for financial advice firms with an evidence-based investment philosophy. He also works as a consultant to other disruptive firms in the investing sector.