“Hedge funds are the only component of Wall Street that is built pretty much entirely upon myth. Few areas of financial endeavour have been a subject of so many hoary myths, moronic half-truths, goofy speculation, once-true falsehoods, and knucklehead fantasies.”

— Gary Weiss, Wall Street versus America

25 years ago the hedge fund industry had about $300 billion of assets under management. As of the end of third quarter 2023, assets had grown to about $5.0 trillion. Given that they have persistently delivered poor performance over the past two decades and have failed to effectively hedge exposure to conventional security classes, the growth of the industry has to be the greatest anomaly in finance.

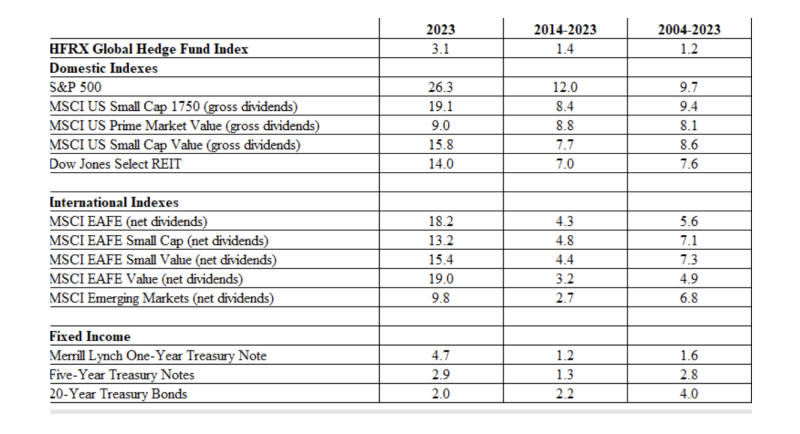

The following table provides the annualized returns of the HFRX Global Hedge Fund Index over the one-, 10- and 20-year periods ending December 2023:

Hedge funds destroyed wealth

- Over each of the one-, 10- and 20-year periods, hedge funds underperformed every single major equity asset class.

- Over the last one- and 20-year periods, they even underperformed virtually riskless one-year Treasury notes and outperformed them by just 0.2 percentage points over the last 10 years.

- Over the last one-, 10- and 20-year periods, they underperformed traditional 60% stock/40% bond portfolios by wide margins. The following table shows the performance of 60/40 portfolios, equal-weighting each equity asset class and then using either one-year, 5-year or 20-year Treasuries.

Surely, anyone who foresaw those results would have predicted that assets would flee the industry. Yet, in a triumph of hype, hope and marketing over wisdom and experience, assets grew dramatically.

Another problem for investors is that the evidence demonstrates that hedge funds in general don’t hedge anything.

Hedge funds don’t hedge

In 2022, while hedge funds managed to outperform equities and longer-term Treasury bonds, they provided negative nominal returns, losing 4.4% even before considering inflation — demonstrating that the term “hedge fund” is an oxymoron. Most hedge funds don’t hedge anything. While they may offer some diversification benefits, they are not hedges, which by definition increase in value when the assets they are supposed to be hedging lose value.

Strange anomaly

The anomaly that is the growth of the industry is even stranger given that the performance of hedge funds has dramatically worsened over the past 25 years. For example, William Bernstein, author of the mini book Skating Where the Puck Was: The Correlation Game in a Flat World, examined the returns of hedge funds, applying a three-factor analysis to the Hedge Fund Research global returns series for the period 1998 through 2012. Bernstein found that while hedge funds did produce large alpha in the first third of the period, as investor assets chased those returns, alpha shrank and then turned negative. From 1998 through 2002, hedge funds produced an incredible alpha of 9.0%. However, from 2003 through 2007, their alpha was -0.7%. And from 2008 through 2012, the alpha was -4.5%. The above table shows how poorly they have done since then. Yet assets continued to pour in.

While investors have ignored the poor performance, academic researchers have not.

Empirical evidence

Nicolas Bollen, Juha Joenväärä and Mikko Kauppila, authors of the 2021 study “Hedge Fund Performance: End of an Era?,” examined hedge fund performance over the period 1994-2016 and found a marked decline in performance over time. For example, the percentage of hedge funds with positive and significant Fung and Hsieh alpha fell from about 20% to 10% over the sample period, while the percentage with significantly negative alpha increased from 5% to about 20% at times. Their findings led Bollen, Joenväärä and Kauppila to conclude: “In sum, we confirm reports that hedge fund performance has weakened considerably over the past decade.” They also examined whether investors could use any of a set of predictor variables to select subsets of hedge funds that perform satisfactorily out-of-sample despite the general decline over time. They concluded that their results indicate “that an overall deterioration in hedge fund performance cannot be overcome by using the predictors.”

Bollen, Joenväärä and Kauppila’s findings are consistent with those of Rodney Sullivan, author of the study “Hedge Fund Alpha: Cycle or Sunset?,” published in the winter 2021 issue of The Journal of Alternative Investments; Javier Estrada, author of the 2021 study “No Hedge Funds, No Cry”; and David Forsberg, David Gallagher and Geoffrey Warren, authors of the 2022 study “Capacity Constraints in Hedge Funds: The Relation Between Fund Performance and Cohort Size,” who found significant decreasing economies to scale in the hedge fund industry.

Investor takeaways

In 1998 Charles Ellis wrote Winning the Loser’s Game. He presented evidence that while it’s possible to generate alpha (risk-adjusted outperformance) and win the game of active management (individual security selection and/or market timing), the odds of doing so are so poor that it’s not prudent to try. The surest way to win a loser’s game, like craps and roulette, is to choose not to play. In investing, that means using passively managed funds (funds that don’t engage in individual security selection and/or market timing and do use systematic approaches to implementation) such as index funds.

My book, co-authored with Andrew Berkin, The Incredible Shrinking Alpha, presented the evidence and the explanations demonstrating that since Ellis published his book, winning the loser’s game has persistently become more difficult. The four themes explaining the deterioration in hedge fund performance, and active managers in general, are:

- Academic research has been converting what was once alpha into beta.

- The pool of victims that can be exploited has been shrinking, as individual investors directly own a shrinking share of public equities.

- The competition has been getting tougher—today’s active managers are far more skilled and have far greater resources.

- The supply of dollars chasing alpha has increased.

The evidence reviewed begs the question: Why have hedge fund assets continued to grow, and why have investors ignored the evidence? One possible explanation is the need by some investors to feel “special,” that they are part of “the club” that has access to those funds. Those investors would have been better served to follow Groucho Marx’s advice: “I wouldn’t want to belong to a club that would have me as a member.” Another explanation is that investors were not aware of the evidence.

Larry Swedroe is head of financial and economic research for Buckingham Wealth Partners, collectively Buckingham Strategic Wealth, LLC and Buckingham Strategic Partners, LLC.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based on third party data and may become outdated or otherwise superseded without notice. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. All investments involve risk, including loss of principal. The portfolios shown in this article are comprised of indexes and are for illustrative purposes only and does not reflect the performance of an actual portfolio. The opinions expressed here are their own and may not accurately reflect those of Buckingham Strategic Wealth, LLC or Buckingham Strategic Partners, LLC. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the adequacy of this information. LSR-24-620

ALSO BY LARRY SWEDROE

Is higher inflation always bad news for stocks?

Active or passive Investors: Which is the “smart money”?

Commission-free trading and lottery stocks

FIND AN ADVISER

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

© The Evidence-Based Investor MMXXIV