Robin writes:

Some say we may be reaching peak passive — the point at which the extraordinary rise in popularity low-cost index funds will end and the proportion of actively managed assets will start to grow again. For what it’s worth, I personally expect this story to run and run; indexing still has huge potential for expansion, especially outside the US. But when peak passive finally comes, will it make active managers any more likely to outperform? And will the benefits of indexing be any less than they are today? Active managers may well be disappointed by this analysis from CRAIG LAZZARA at S&P Dow Jones Indices.

With more than $7 trillion tracking the S&P 500 alone, we at S&P Dow Jones Indices estimate that index funds now encompass between a quarter and a third of the capitalisation of the U.S. equity market. This extraordinary growth must surely rank as one of the most important developments in contemporary financial history.

When will it end? For at least the last five years, critics of indexing have argued that the growth of passive management is a “bubble” and, like all investment bubbles, destined to end with weeping and gnashing of teeth. We saw the Information Technology sector peak in 2000, and Financials in 2007. Might we now be approaching what some analysts characterise as “peak passive?”

What index funds today and technology stocks in the late 1990s have in common is that both have attracted large inflows. But that is where the similarity stops. The technology bubble was driven by active decisions, as investors allocated more and more weight to one segment of the market. The growth of indexing is driven by investors eschewing active decisions—in other words, by recognising that most active managers underperform most of the time. As the technology bubble inflated, portfolios became more concentrated; as assets move from active management to index funds, portfolios become more diversified.

Despite these obvious benefits, we concede that indexing’s impact on market efficiency is ambiguous. It’s fair to describe the typical index portfolio as a price taker rather than a contributor to price discovery. This means that the valuation of index constituents is ultimately decided by active managers (and some factor indices) whose trades are motivated by their own research. And indexers do contribute to market efficiency indirectly, by taking assets from the least capable active managers, thus increasing the influence of their more astute competitors.

All this means that the idea of peak passive, while computationally unclear, isn’t conceptually wrong. But understanding where the peak might be requires us to distinguish between passive assets under management and passive trading.

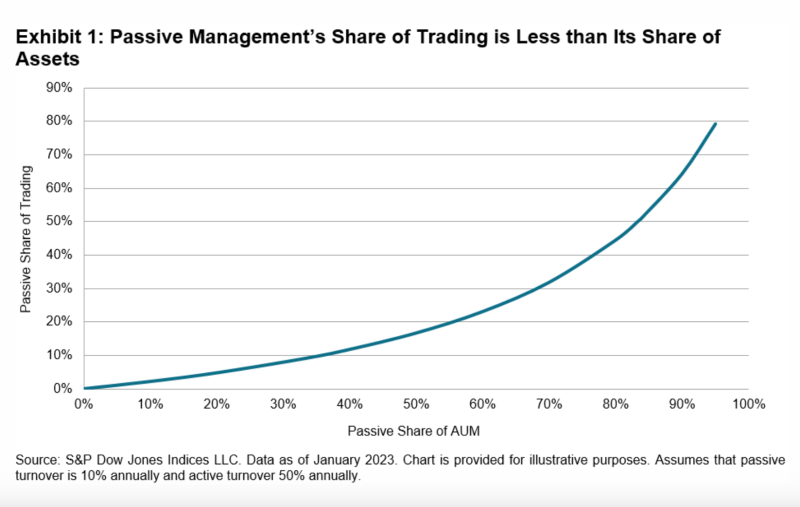

Comprehensive cap-weighted index funds trade relatively little in comparison to active managers. Exhibit 1 shows that, on reasonable assumptions, if indexers own a third of the market’s assets, active managers will still do 91% of all trading. Under these assumptions, index AUM share must rise above 83% before active managers’ share of trading drops below 50%. And even at that level, there’s no a priori reason to assume that market efficiency would be impaired. (After all, active research is not unfailingly prescient.)

How will we know, at some future date, that markets are no longer sufficiently efficient? Presumably one of the indicia of market inefficiency would be a sufficiently large number of mispriced stocks, so that the value of successful active management would increase. This is a plausible outcome. But remember: the only source of outperformance for the outperformers is the underperformance of the underperformers. Active investment management remains a zero-sum game.

Even if we do approach peak passive, therefore, the active manager’s life will be no easier, and the benefits of indexing will be no less.

CRAIG LAZZARA is Managing Director and Global Head of Index Investment Strategy at S&P Dow Jones Indices.

PREVIOUSLY ON TEBI

Stories almost always trump statistics

Why investors repeat the same mistakes

Five ways to get better with money in 2023

FIND AN ADVISER

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

© The Evidence-Based Investor MMXXIII