Facts change, and Chancellors change! As we identify updates and corrections for our book “How To Fund The Life You Want”, we will list them below the form on this page. Click here to leap down to updates and corrections.

♦♦♦ A word about reviews: if you’ve enjoyed our book, we’d really appreciate you leaving a review on Amazon. It doesn’t need to be a long one. Most books in the UK are sold through Amazon, so even a short review there helps us to spread the word about the book. ♦♦♦

Send us your corrections (or comments)

If you find any errors of fact in the book (or our workbook), please use the form below to let us know about them. We also welcome your thoughts about how we can improve the book for future editions.

Updates and corrections

Chapter 2: Invest In … Yourself

Correction on EMPLOYER PENSION CONTRIBUTIONS, page 30. Although a typical employer must contribute 3% provided you contribute 5%, not all of your 5% is deducted from your salary. The deduction from your salary is 4%, the remaining 1% of “your” contribution is provided by HMRC, in the form of tax relief.

Chapter 3: Manage Your Money

Update on PENSIONS MOUNTAIN, pages 56–57. The state pension has increased; Which? updated its retirement spending survey in April 2022; the PLSA has recently updated its equivalent survey; and inflation has risen considerably. All these affect the underlying calculations that gave the approximate figures in the “pensions mountain” graphic. Please remember our caution that it is designed only to give a broad impression. We highly recommend you use worksheet 3b from our workbook to help you to use the same logic – but with figures you choose yourself, based on your own life and the latest data.

Chapter 6: Take The Right Risks

Update on “SAFE” WITHDRAWAL RATE, page 119. Morningstar have published a very detailed report (note: all based on US data) that gives a thorough testing against historical data to every possible variant on managing this withdrawal rate. You have to register your email address to download the report, but it’s well worth if you want to look into this issue more deeply.

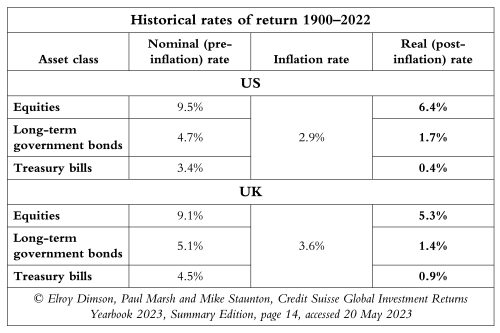

Update on LONG-TERM ASSET RETURNS, page 123. Elroy Dimson, Paul Marsh and Mike Staunton regularly update their Credit Suisse work mapping long-term returns. Their data as at May 2023, following the same table format we presented on page 123 of our book, is as below.

As might be predicted when the new data adds just one more year to a very long-term average, the returns on equities are not much changed.

The most notable change to us is the difference in the real return on long-term UK government bills, which has fallen from 1.8% to 1.4%. This is a significant change in such a short time. The crisis in the bond market initiated by the Liz Truss government has shown that bonds can experience significant volatility, a volatility that reduces their contrast with equities on the asset spectrum. This was an unpleasant shock to many people invested in portfolios towards the “defensive” end of the spectrum. In the book we challenged the widespread use of “lifestyling” portfolios that aim to reduce volatility as their owners approach retirement age, hiding an assumption that the owners will buy an annuity as a one-off life event. Many of these portfolios, which were heavily invested in bonds and bills, suffered particularly nasty setbacks during the bond crisis.

However, the drop in return on long-term US government bonds was less, again emphasising the value of international diversification.

Correction on COMMODITIES as an asset class, page 127. The real return is -2.6% (inflation averaged and subtracted only for the years that these commodities records are available, 2007 to 2022). Because of the short duration of the records, conclusions about this asset class need to be handled with care, but the same fundamental story appears: the real return has been negative.

Update on ANNUITIES, page 129. Since we published the book, annuities have become cheaper. That is, you can get more income from an annuity per pound you spend. This is because global interest rates have risen. We focused your attention in the book on the value of later-life annuities (covered in detail in Chapter 7: Manage Your Mix). We still maintain that is where the spotlight should fall.

We note that even though prices have fallen for annuities that are not index-linked against inflation, annuities that include inflation protection remain pricier. And the recent surge in inflation is a reminder of its insidious long-term effects.

However, we would not wish to discourage you from looking at online comparison tools such as the Moneyhelper annuity tool, just to gauge the costs and benefits of an annuity taken at any point in your retirement. Tools like these can help you look at the costs and constraints quickly (and without provoking an avalanche of sales calls). We also recommend this Financial Times article which gives a very well-rounded look at the issue and options (paywall).

Chapter 7: Manage Your Mix

Update on COMBINING PENSIONS, pages 149 and 166. For a great explanation of the issues to consider, see the excellent recent paper by Steve Webb and Dan Mikulkis: Five good reasons to consolidate your DC pensions – and five reasons to be careful. As well as considering whether you would lose employer contributions by combining your DC pensions, consider any other benefits you might lose: for example, your right to access money more easily if one of your pension pots is small.

Update on TAX FOR PEOPLE LIVING OUTSIDE THE UK, pages 156 and 157. We advise readers living under tax regimes outside the UK to note: even if you can benefit from any tax principles because of savings or income in the UK, if you are living abroad, your local tax authority will probably levy different tax principles that clash with them. For example, they may apply higher rates – or disregard the tax-free status of benefits available to people living in the UK, such as ISAs or tax-free pension cash. Nothing in our book should be read as commenting on any tax regime outside the UK.

Correction on INHERITANCE TAX AND PENSIONS, page 156. We’d like to thank the kind reader who wrote to us to point out that, while under most circumstances DC pensions will fall outside the scope of inheritance tax, there are some situations in which they fall within it. It depends on whether and how you instruct your pension provider about who inherits. If you provide them with an “expression of wish”, the pension provider retains discretion about who to pay the pot to, and this discretion keeps the pot away from inheritance tax. But if you give a more stringent “direction” (sometimes called a “nomination”), it is highly likely that the pot will go into the mix with your other assets for inheritance tax. This is also true if you forget to tell your pension provider anything at all about who should inherit. Of course, whether you will ultimately pay any inheritance tax depends on the total of all your assets. MoneyHelper has useful guidance on this topic.

Update on PENSIONS ANNUAL ALLOWANCE (page 158), which rose from £40,000 to £60,000 a year in April 2023. This meant that if you are a higher earner (or have cash to spare from other sources, such as an inheritance), you can put much more into your pension while benefitting from the tax subsidy that comes with it. For people in that happy situation, this will widen the advantage gap between investing for your future life in a pension, as opposed to investing in a stocks and shares ISA. This is because ISA contributions remained capped at £20,000 a year. However … see the next paragraph.

Update on ISAs, page 158. In the 2024 Budget a consultation was announced about increasing the stocks and shares ISA allowance by £5,000 a year – provided you invest the additional money in UK companies. If it is introduced, that will be in a later tax year, yet to be confirmed.

Update on DIVIDEND TAX and CAPITAL GAINS TAX, pages 157 and 159. For dividend tax, the £2,000 allowance was reduced in the 2022 Autumn Statement. It will fall to £1,000 in 2023, and £500 in 2024. A similar fall will take the capital gains tax allowance from £12,300 to £6,000 and then £3,000. These apply to investments held outside a pension, and don’t apply to a stocks and shares ISA.

Update on LIFETIME ALLOWANCE, page 161 onwards. In our book we described the lifetime allowance as a “distinctive and especially unpopular tax”. It looks like Chancellor Jeremy Hunt must have been as avid a reader of How To Fund The Life You Want as the rest of you, because in his Spring 2023 budget he announced its compete abolition. This is a major and very welcome simplification (although note that the Labour Party has said it will reverse the abolition if it takes power). It means that you can now grow your investment-based (DC) pension pot as large as you like, without suffering a punitive extra tax on growth above £1,073,100. This might seem like an implausible sum, but for those who start early and invest in an evidence-based way, it’s closer at hand than you think. A key consequence of the abolition is making the maximum you can claim as tax-free cash 25% of the final value of the lifetime allowance (£268,275), except if you had taken out specific protections that were available up to 2016. Some people who began accessing their pensions before the LTA abolition may want to apply for a transitional certificate to ensure that they are not, in the future, taxed as if they have exceeded the maximum tax-free cash if, in fact, they won’t have done so.

Update on VANGUARD AND ESG, page 169. Vanguard has disengaged from a Net Zero initiative, one supported by many other fund managers. This is only one area of ESG, but obviously an important one, as it focuses on climate change. The statement from Vanguard however says that this “will not affect our commitment to helping our investors navigate the risks that climate change can pose to their long-term returns”.

Update on SOCIAL CARE TAXATION, pages 156–7 and 180–184. The Health and Social Care Levy we referred to has subsequently been abolished. The reforms we explain in the book delivering new social care benefits (ie, caps and subsidies) are still the official plan, funded through general taxation instead, from October 2025. However, many political commentators are talking about these reforms as if they are also a dead letter. The 2024 General Election is almost certain to throw them into further doubt. In addition:

- Update on SOCIAL CARE COSTS, page 181, and ANNUITIES, pages 184–5. Given that state support is so uncertain, it is good that the Financial Times ran a useful 2023 article looking at private social care costs, which are (of course) rising; an article that provides fresh data to compare with the figures we gathered in the book. It also points out that “immediate needs annuities” can be bought (from a handful of providers) to pay care costs with defined income. Notably, this income will be tax free if it’s paid directly to the registered care provider. No doubt terms and conditions apply, but it’s worth knowing that this type of annuity can be part of the overall mix of choices for later-life annuities.

- Correction on “HOTEL” COSTS, pages 182–183. This correction relates to the new care cost rules referred to above, so carries all the questions about the future of that policy. In the book we said that hotel costs, which will be subtracted from residential care costs as you progress towards the cap, could be as much as 2/3 of the cost of residential care. A reader kindly wrote to us to clarify that hotel costs are capped under the new rules, at £200 a week (2022 figures). (In government jargon, these are referred to as DLCs or daily living costs.) This means that if, at the time of the new rules, you have to stay in a residential care home, you will progress towards the cap (currently £86,000) more quickly than we modelled on page 183. This will be because more of your care home costs will be spent on care itself, not the DLCs. Also, as things stand in 2024, the full state pension figure covers the DLCs.

- Further considerations on length of stay and offsetting costs in CARE HOMES (p180). The averages we quoted from the British Geriatric Society website no longer seem a good match for figures from the Office of National Statistics, which give an average life expectancy of 3.1 years for people over 80 in care homes (people receiving nursing care are likely to stay for a shorter time, but the ONS does not provide this as a subset of their data). This breaks down as 3.6 for women, 2.6 for men. Other sources give different numbers and there is a shorter median figure. This is clearly an area where it is difficult to measure agreed, meaningful data. We’d like to thank the kind reader who pointed this out, and also pointed out that if you go into a care home and pay the full costs you could expect to receive Attendance Allowance, which would help to offset costs to the tune of £70–£100 a week. Further, if you are registered as blind, Blind Person’s Allowance would add several thousand pounds a year.

Chapter 9: Find a first-rate adviser

Update on VANGUARD’S FINANCIAL ADVICE SERVICE, page 216. Sadly this innovative low-cost service has now been closed by Vanguard.

Update on OPEN MONEY, page 216. Open Money has since changed name to Octopus Money.

Update on SOURCES OF GUIDANCE, page 212. We also recommend HonestMoneyNow as a deep, wide source of impartial guidance about investing, targeted and written for people living in the UK. It is maintained by the ferociously independent UK Shareholders’ Association.