Sometimes, the best things in life really are free. One of them, says JONATHAN HOLLOW. is an online resource called MoneyHelper. Here he outlines its three most useful tools.

I used to work for the Money Advice Service. It had a troubled and controversial history between its founding in 2010 and rebranding in 2021. There’s no space here to go through those controversies. But much fuss centred on its website, and on the word “advice” as part of the service name. (Despite this word, the service only offered information and guidance, and this drove regulated financial advisers mad.)

After an unhappy decade these problems have been resolved. It’s under new management and rebranded as “MoneyHelper”.

This new MoneyHelper website contains many useful tools. I’m using this article to highlight top three most relevant to UK readers of this site. I’ll also suggest how you might get the most out of them.

A free tool to help you find the best pension fees comparison

In our forthcoming book, Robin Powell and I devote pages to the issue of how to reduce the fees you pay to others for them to manage your money. It’s one of the few investment variables you can control.

MoneyHelper offers a great free service in the form of its pension drawdown tool. This compares a selection of providers who are offering “guided investment pathways” for “DC pensions drawdown”. That is, providers who will manage your pension investments through a sensible lifestage-based approach. And will allow you to draw down your money in a convenient way.

Very importantly, it gives a pension fees comparison.

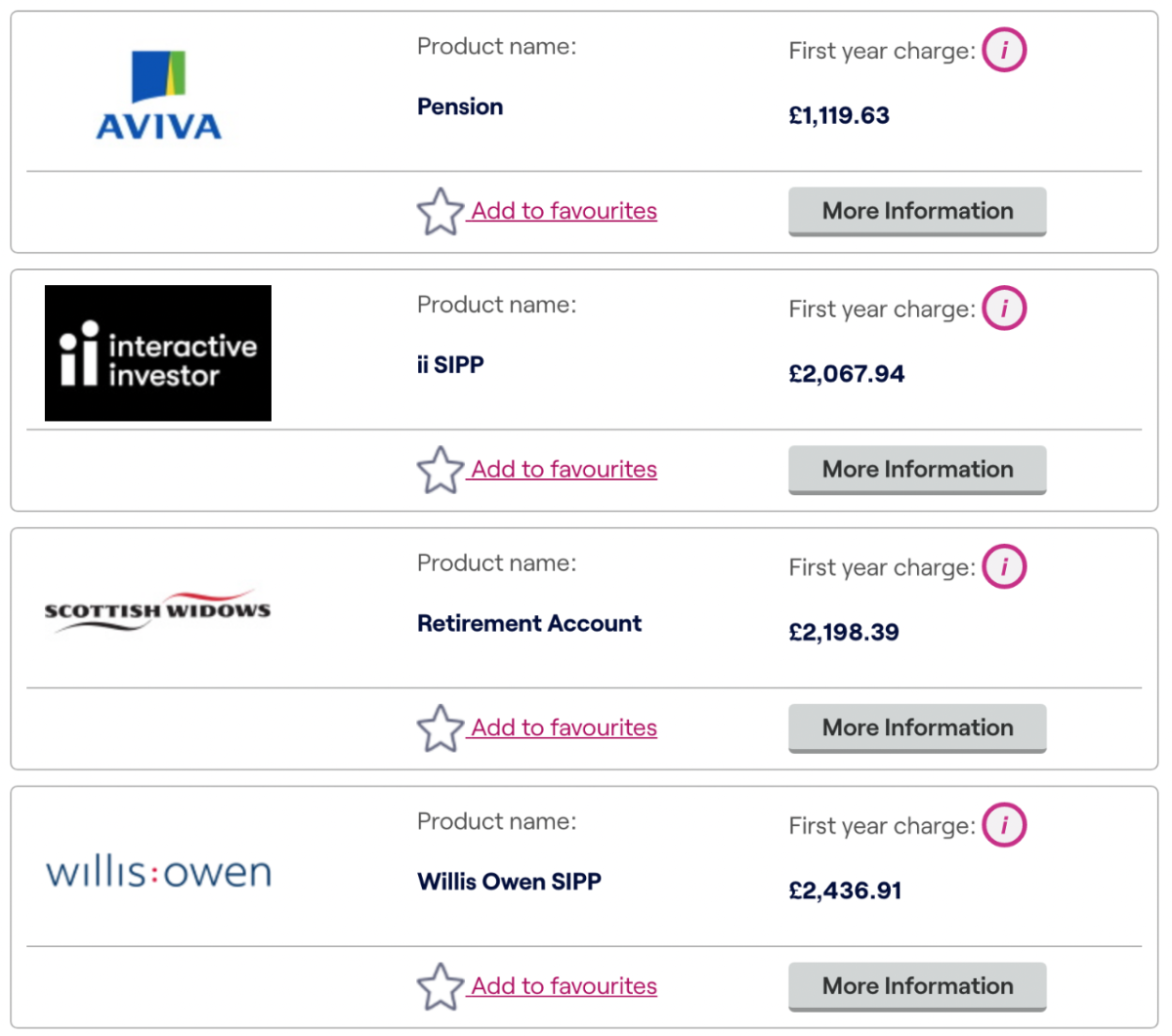

The great thing about MoneyHelper tools is not only are they free, but they ask for few personal details – the absolute bare minimum — before they give up the goods. This tool will take less than five minutes to fill in. It then provides results like the screenshot below. MoneyHelper automatically sorts the results in alphabetical order of provider. But you can re-order them by fees (low to high), as I have done.

Look at this pension fees comparison: for broadly comparable investment management, the lowest-cost provider costs 50% less than the fourth on the list!

This tool does make it clear that it isn’t “whole-of-market”. That’s a potentially frustrating limitation. But in practice, the brands above show that it includes some of the most important providers in the market. Even if you end up finding a better provider, one not represented on this tool, you could use the costs the tool displays to haggle down your fees.

A free tool to help you compare guaranteed annuity rates

An annuity is a guaranteed retirement income paid for with a large up-front sum. They have fallen out out of fashion. In recent years, compared to drawdown pensions, they have offered a lower income for the same money.

But in our forthcoming book, Robin and I recommend people reconsider guaranteed annuities as they approach age 75. As you get older, you get a better annuity income for the same money. And if cognitive decline (or even dementia) should ever take hold, guaranteed annuity rates give you one less thing to worry about.

The MoneyHelper annuity comparison tool makes it easy and hassle-free to check whether an annuity could be worth your while. Unlike commercial provider sites, it doesn’t draw you into an intimate relationship before you get the results you need. (Some commercial providers require you to enter contact details, then email you your results. This is then followed by the dreaded sales calls.)

The tool states that it compares quotes from all providers.

It does require a few personal questions to be answered – for example, about your health. These will shape the terms of any annuity.

Along the way, it offers useful explanatory videos, which put the questions and options in context. To make best use of these, set aside 30 minutes for using the tool.

To give you sample results from the tool:

- A healthy, single 65-year-old spending £250,000 to buy an inflation-linked annuity, with no inheritance, could expect to get roughly £6,500 a year guaranteed income for the rest of their life.

- But a healthy, single 85-year-old spending £250,000 on the same type of annuity could get roughly £21,200 a year for the rest of their life.

You can save and retrieve the quotes the tool gives you. This is a useful feature, as it takes a little more input to get them. And you may not remember exactly which choices you made along the way.

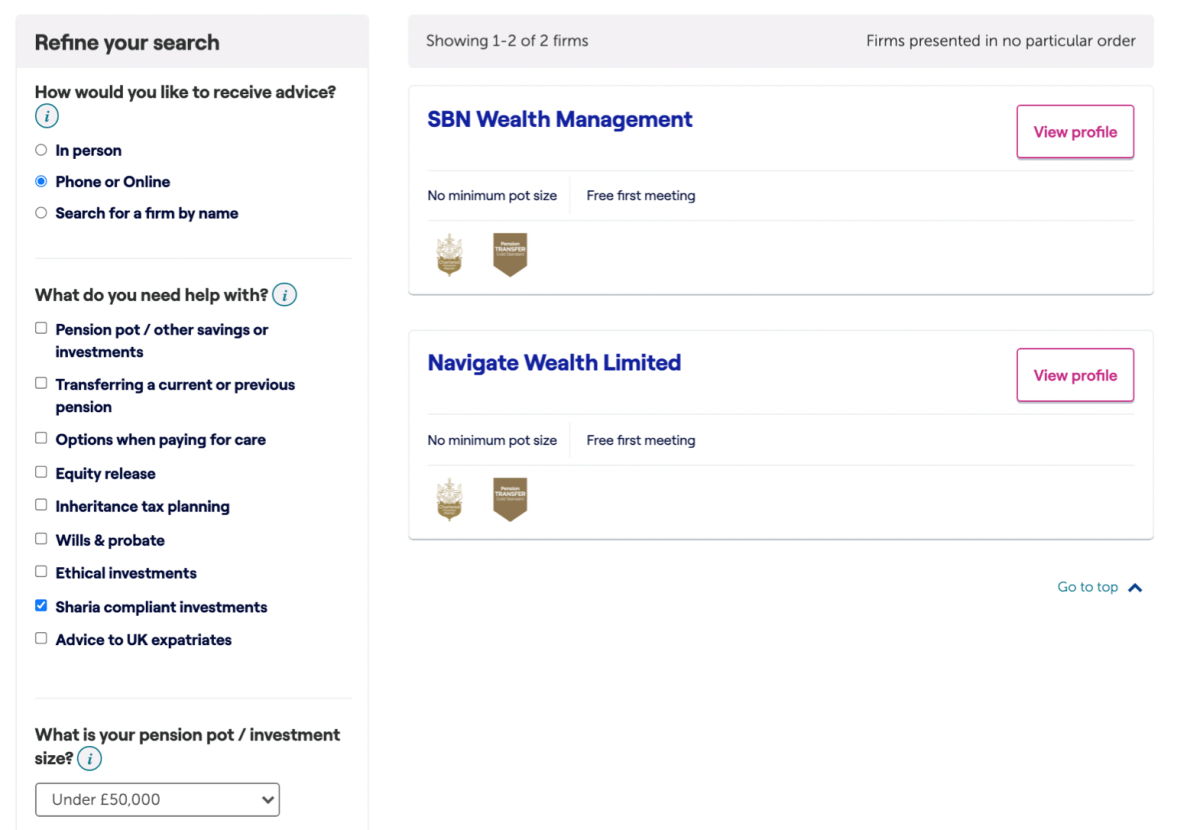

A free tool to help you find an independent financial adviser

Unbiased.co.uk and vouchedfor are commercial directories that help you to find an adviser. And The Evidence-Based Investor site will also help you find an adviser — one who sticks to evidence-based principles.

So the final MoneyHelper tool I’m going to mention has plenty of competitors. But similar to its other tools, you don’t have to hand over your contact details before you get a good list of independent financial advisers.

This can be quite helpful for people (like me) wary of handing my email address to any site that might result in a volley of sales calls.

It has a speedy, simple interface, offering quick results. You can then filter them in helpful ways. My screenshot has found independent financial advisers who can advise on Sharia-compliant investments and are willing to deal with investments of less than £50,000. (The directory was set up above all to serve investors with smaller pots, but its coverage is wide.)

The retirement adviser directory is the quickest of the three tools to give you your results, but all three are pretty slick

You can also filter advisers by which financial qualification they have. (Unfortunately, the tool doesn’t provide any detailed background information to help you understand the difference between these qualifications.)

Sadly, but not surprisingly, the tool doesn’t offer a fee comparison. To find out fees, you will have to do a lot more digging with the individual advisers that you decide to check out. But this says more about the independent financial adviser market than MoneyHelper.

No adviser tool could ever hope to capture 100% of advisers at any one time. But the MoneyHelper tool aims to cover the whole market and will give you more than enough choice before you find your own independent financial adviser.

MoneyHelper is now… helping

Given the bad reputation of the Money Advice Service, a rebrand was probably wise. Tools like these existed under the Money Advice Service brand, but I think they will be better accessed and more trusted in their new livery. I was party to the brand research and was impressed by the cut-through the MoneyHelper name had with target audiences.

Tools like these give you complex comparisons and calculations after an investment of minutes, not hours. It’s never been easier to take the hard maths and the slow slog out of managing your own investments. All you need to know is which tools are worth using.

And we live in a golden age of free tools, not just from public-minded organisations, but commercial organisations as well. In a later article in this series, I will point out further valuable tools, celebrating the fact that individual investors can call on calculators, tax checkers and price comparisons galore.

JONATHAN HOLLOW worked for the UK Government’s Money and Pensions Service and is a writer and commentator on consumer education and protection.

ALSO BY JONATHAN HOLLOW

Money lessons from the Ukraine crisis

Keeping your digital life secure

How to avoid investment fraud and scams

FIND AN ADVISER

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

© The Evidence-Based Investor MMXXII