Inflation is the parent of unemployment and the unseen robber of those who have saved.

— Margaret Thatcher

We have all seen news stories explaining that in this inflationary environment cash is generating negative returns when adjusted for inflation. Cash is also generating negative returns when adjusted for my weekly grocery bill. Both are true statements so why the intense focus on the former?

The corrosive power of inflation is garnering a lot of headlines lately, and is one of the most frequent reasons people cite for being concerned about meeting their current and future spending needs. Inflation is clearly a component of our financial planning, but only one of many moving parts. Let’s put inflation into perspective and hopefully relieve at least some of the angst.

What is inflation?

The US Bureau of Labor Statistics (BLS) reports Consumer Price Indices (CPI) which measure changes in the price level of the economy over a period of time. The CPI measures a basket of goods and services trying to represent a typical household’s spending on various common items such as food, clothing, housing, transport, utilities etc. Inflation is a general rise in these price levels. Simply put, ‘stuff’ will cost more in the future.

Real rate of return

As a result, economists and financial pundits talk about the loss of purchasing power and the need to consider the “real” rate of return (i.e., nominal investment return minus the inflation rate) when projecting growth of investments. As an example, if your investment return is 5% and inflation is 3%, the “real” rate of a return is 2%.

Economists use the real rate of return to help explain economic trends and their impact on global populations over time. I agree with this macroeconomic view of the world, but when it comes to personal financial planning, the “netting” of inflation with returns unnecessarily muddies the water.

When I have a future purchase to make and $100 in my pocket, I don’t think in terms of how much less the one-hundred-dollar bill will buy next year, but rather how much more the goods I seek might cost. Personal financial planning should follow this same intuitive thought process.

Avoid netting variables

While planning and projecting out cash withdrawals, I view inflation as simply another expense (one more retirement spending need) rather than a negative or “contra” rate of return. Rather than deflating your investment return, inflate your expenses.

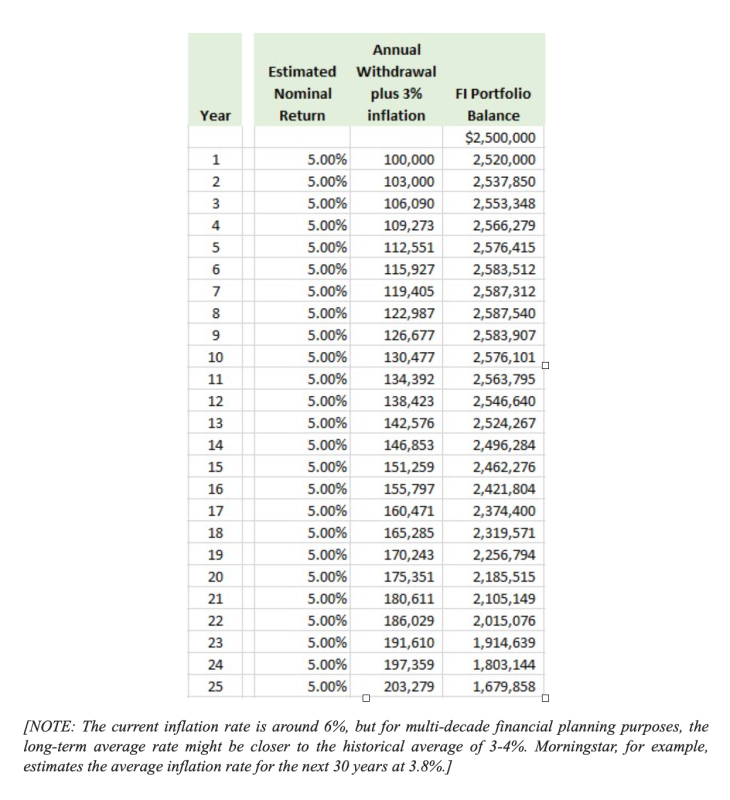

For example, let’s say you have projected to start withdrawals with a $2.5m portfolio, expected nominal investment return of 5%, a long-term annual inflation estimate of 3%, and an annual spending goal of $100,000. If all assumptions prove correct, in year two your total spending needs would increase by your inflation rate, so you would need to withdraw $103,000; year three would be $106,090 and so on. See the chart below.

As you can see in the chart, by year 25, the 3% inflation has doubled your annual spending need from $100,000 to more than $200,000! That is the corrosive power of inflation that garners the headlines. But it is not the complete story.

Notice that with a 5% nominal return, your portfolio would generate more than enough to cover your spending for the entire 25-year period and beyond (including your inflated expenses). And just as importantly, the $1.67m balance in year 25 is the projected actual dollars in the portfolio, not a hypothetical inflation-adjusted balance.

Obviously, the above is a simplistic example of a multi-variable projection. Your results will vary (it’s called personal finance for a reason). The point is, as you dutifully go about your planning process, avoid netting variables whenever possible. Keeping gross expenses on one side of the ledger, and gross returns on the other is simpler, and simple beats out complex every time.

What, specifically, is inflated?

The BLS publishes monthly averages for 211 spending categories across 38 urban geographical areas and uses that data to calculate several variations of CPI that are used for different purposes. I, however, have far fewer spending categories and I live in just one urban area.

Inflation is individualised and each person feels inflation to different degrees. What really matters in our financial journey is your “personal inflation rate” or in other words, the annual increase in your total retirement spending. Financial author Jason Zweig likes to call it ‘meflation.’

Studies have shown that changes in retirement spending can vary dramatically among retirees, and while some expense categories increase, others eventually decrease. A national average inflation rate might be a starting point, but the actual increase (or decrease!) in your total spending needs is much more informative and of practical use, as you plan out your current spending, and retirement withdrawal strategies.

Keep inflation in perspective

The sum of all your personal expense categories will add up to 100% of your spending needs. Long-term inflation, on average, has been approximately 3% of that total. The remaining 97% of your spending deserves equal billing, or just maybe, a little more of your attention.

‘Real’ returns are useful when evaluating macro-economic trends across a large population, but when getting down to personal financial planning for a population of one, keep the process intuitive. Do not let inflation rob your plan of its simplicity.

As always, invest often and wisely.

COSMO DeSTEFANO is a retired CPA and tax partner based in Massachusetts. He is the author of a new book called Wealth Your Way: A Simple Path to Financial Freedom.

ALSO IN THIS SERIES

Don’t miss out on your only free lunch

Market cycles teach us, but do we learn?

One definition of risk for all of us

LISTEN TO ROBIN POWELL SPEAK IN LONDON

TEBI founder Robin Powell and his co-author Jonathan Hollow will be speaking about the murky world of investment fees and charges in London at 5.30pm next Wednesday, 17th May.

They’ll be explaining you may be paying for a nice retirement for people you don’t even know, and what you can do start funding YOUR dream life instead.

The event is free, but places are limited, so book early to avoid disappointment:

FIND AN ADVISER

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

© The Evidence-Based Investor MMXXIII