As times get tighter, keeping to a budget is becoming important for more and more people. JONATHAN HOLLOW is an enthusiastic user of the digital tools banks are now providing to help you budget. Here he reviews the best ones out there and explains how to make the most of them.

Banking in the UK has changed so much in the last decade. Even five years ago, leaders from established banks may have said “probably not” or “definitely not” to the question of whether they should provide budgeting tools. Some would have claimed that if they offered budgeting support, this might stray across the regulatory boundary and become high-risk “financial advice”. Others would have seen no need to add any bells and whistles to their existing business.

Then — as the saying goes — Monzo, Revolut and Starling “ate their lunch”. The vibrant fintech (financial technology) scene in the UK spawned nimble, creative and customer-hungry challenger banks and electronic money providers. They have become a huge hit with customers. And they offer some of the best budgeting tools in the UK.

This article is going to be a little Monzo-centric because it’s the bank I use for everyday spending and budgeting. Please don’t take it as an advert for Monzo. Firstly, they don’t know I’m writing it and definitely aren’t going to pay me for it! Secondly, I’m keen to use the example of Monzo to draw out some principles about good practice that you’ll find in a host of other banks.

Even the big, old banks these days.

Understand how safe your money is

Not all of the new kids on the block are banks. Some are “electronic payment” or “electronic money” providers. Comparison and review lists (to shop around, see this one from the Guardian and this from Which?) will widen your choices even more. If the provider you choose is not a bank, the safeguards on your money from the regulatory system will be weaker.

However, if you use your provider for a quick “throughput” of spending, fed from a fatter, better protected account, the amount of money at risk at any one time may well be tolerably low.

Monzo began as an electronic money provider and is now a fully-fledged bank, so things will change over time.

The curse of legacy systems

When Estonia was freed from the shackles of the Soviet Union, little of its government business was being done on computers. The computer systems that did exist were either withdrawn from Estonian use, or simply discarded by the Estonians. It’s no coincidence that Estonia is now one of the world’s most exemplary digital-first economies, with stunning e-government services. They had no IT legacy and were able to build everything from scratch.

New banks have exploited the same advantages. Unlike the big four established banks, legacy systems imposed no constraints. They started coding with revolutionary customer needs in mind. They get their ideas for new features from customers, and introduce them frequently, to the drumbeat of a rapid development cycle.

But the lumbering big-bank beasts, with their legacy systems, have begun to follow. Their current accounts are pre-loaded with more and more features that can help you to:

- set a monthly budget

- track your spending

- and anticipate what will be left after regular bills have gone out.

Budgeting should not be passive!

A word of warning, though, before I look a little bit more at features. I do believe our banks should help us to budget, but I also believe that in the ideal world it is we who should budget. The algorithms can only get us so far. Robin Powell and I have set out a user-friendly approach to taking control of your budgeting in our book, “How To Fund The Life You Want”, forthcoming from Bloomsbury this autumn.

Budgeting should be an active process. You need to set the overall amounts, and check in regularly to make sense of what’s going in and out. The tools I have seen are not smart enough (yet) to categorise spending automatically and generate insightful warnings. They are, however, very good at showing you what is going on, so that you can keep on track.

The most important basic technique to budgeting is to have more than one bank account if you possibly can. This is known as “jamjarring” – following the metaphor of saving coins in different jam jars for different purposes.

For example, I have an account for everyday spending, one for all regular bills, and one for holidays.

If you know how much should be going into each one, and you can see whether it’s running out, you’re already doing 80% of the basics of budgeting.

Once you have your jam jar system set up, the digital tools banks provide will become much more useful. They have at-a-glance ways of showing whether you are on track.

Some budgeting tools under the microscope

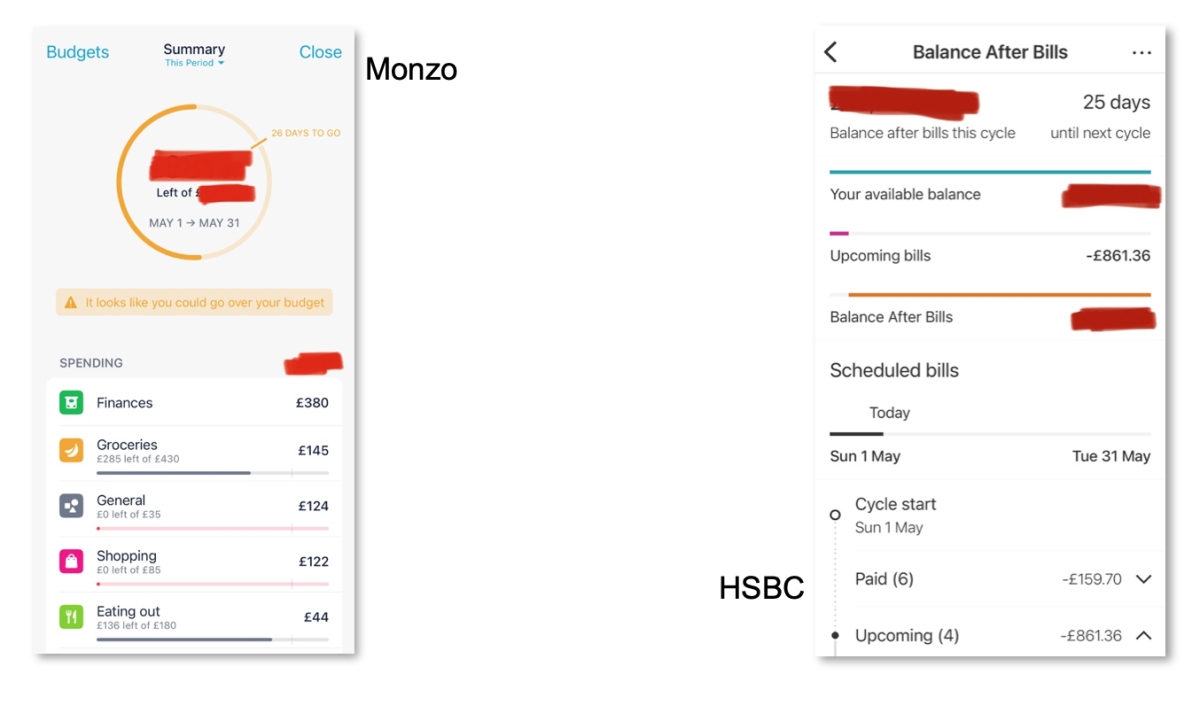

Monzo is a great example. In the screenshot below, you see how the dial is clearly showing where I should be within my monthly budget (the vertical line crossing the dial) versus where I am (the thicker line). And a suitably cautious warning: It looks like you could go over your budget. (Don’t worry, I’m not going to open a Gofundme — it was to do with a large cash payment for a holiday that same month).

You’ll also see automatically generated spending categories below. These are based on assigning the shops and services where I have spent money to general categories. I have never found these useful, because they are too imprecise. I just keep my eye on the main headline figures.

HSBC (also below) doesn’t offer this same visualisation. But it does have a nifty view of how your regular bills affect the overall balance. And it has a line that shows you where you are in the monthly spending cycle. This is a bit less easy to interpret with some key figures concealed, but I’m hoping you can get the overall idea.

Beyond information

Everything I have talked about so far is just the gathering and display of data. But there are plenty of tools going beyond that:

- Monzo, Starling Bank, and Revolut all offer to round up your transactions, for example to the nearest pound, and put the “change” in a savings pot.

- Monzo has introduced a free “pay in 3” feature, where you can split purchases into three monthly payments. These are interest-free. (It also offers longer payment splits if you are prepared to pay interest.) Provided you are able to resist overspending, this is a great tool for smoothing “lumpy” spending.

- Emma highlights subscriptions you may not need, in case you want to trim them.

Which is the best budgeting app?

You won’t see the real value of these tools until you have a few months’ data in them. This makes “shopping around” to choose the best app quite difficult. For most people, budgeting tools won’t be reason enough to switch banks completely. However, if you use a bank with good tools for everyday spending, switching will be much easier, because you won’t have too many direct debits and subscriptions attached like limpets to your account.

My sense is that the more data customers put into these tools, the better their providers will make them. Given that most of them are free or very cheap, they are a great bonus for consumers.

Could banks go further?

In my next article, I’m going to put forward a “modest proposal” for the Chancellor of the Exchequer. I believe banks in the UK could make a radical difference to people’s everyday budgeting habits with some relatively simple, technology-driven changes. I look forward to developing that theme next time.

JONATHAN HOLLOW worked for the UK Government’s Money and Pensions Service and is a writer and commentator on consumer education and protection.

ALSO BY JONATHAN HOLLOW

Bitcoin is not an investment — I’m glad I sold it

Money shouldn’t be “dark matter” for today’s children

Have you discovered MoneyHelper yet?

Money lessons from the Ukraine crisis

Keeping your digital life secure

THE PODCAST

Have you discovered The TEBI Podcast? You’ll find it on SoundCloud, Spotify, Apple Podcasts, Podbean or your preferred podcast provider.

© The Evidence-Based Investor MMXXII