By LARY SWEDROE

The greatest advantage from gambling comes from not playing it at all.

— Girolamo Cardano, 16th century physician and mathematician

My good friend Bill Schultheis, author of The Coffeehouse Investor (it was a privilege to write the foreword to an updated edition of his classic book), devised a game called “Outfoxing the Box” to help investors understand that the winning investment strategy is to accept market returns. It depicts a game that you can choose to either play or not play.

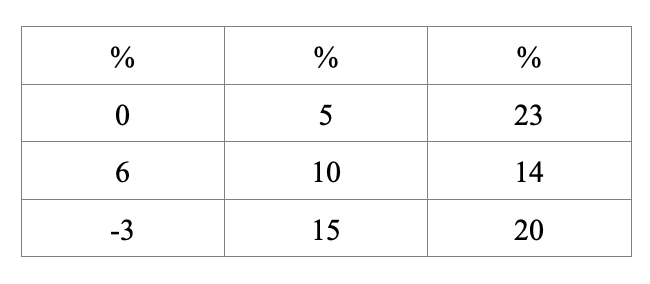

In this game you are an investor with a choice to make. The table below contains nine percentages, each representing a rate of return your financial assets are guaranteed to earn for the rest of your life.

In my years as an investment adviser, whenever I present this game to an investor, never once has the investor chosen to play. Everyone chooses to accept par, or ten percent. While they might be willing to spend a dollar on a lottery ticket, they become more prudent in their choice when it comes to investing their life’s savings.

You are told that you have the following choice: You can accept the 10 percent rate of return in the center box; or you will be asked to leave the room, the boxes will be shuffled, and you will have to choose a box, not knowing what return each box holds. You quickly calculate that the average return of the other eight boxes is ten percent. Thus, if thousands of people played the game and each one chose a box, the expected average return would be the same as if they all chose not to play. Of course, some would earn a return of negative three percent per annum, while others would earn 23 percent per annum.

This is like the world of investing. If you chose an actively managed fund and the market returned ten percent, you might be lucky and earn as much as 23 percent per annum, or you might be unlucky and lose three percent per annum. A rational, risk-averse investor should logically decide to outfox the box and accept the average (market) return of ten percent.

Now consider the following. In the “Outfoxing the Box” game, the average return of all choices was the same 10 percent as the 10 percent that would have been earned by choosing not to play. Fifty percent of those choosing to play would be expected to earn an above-average return and 50 percent a below-average return. The academic research on the performance of actively managed mutual funds, as presented in my book The Incredible Shrinking Alpha, co-authored with Andrew Berkin, shows that the odds are far worse than 50 percent. In fact, today only about 2 percent of actively managed funds generate statistically significant alphas on a pre-tax basis. If you would choose to not play a game when you have a 50 percent chance of success, what logic is there in choosing to play a game where the most sophisticated investors have a much higher failure rate? Yet, that is exactly the choice being made by those playing the game of active management.

The research, including studies such as Richard Ennis’ 2020 study on the performance of public pension plans and university endowments, Institutional Investment Strategy and Manager Choice: A Critique, has found that even the big institutional investors, with all of their resources, fail to outperform appropriate risk-adjusted benchmarks. In addition to their other advantages, the major one institutional investors have over individual investors is that their returns are not subject to taxes. However, if your equity investments are in a taxable account, the returns you earn are subject to taxes. Let’s look, then, at the odds of success of outperforming par (a simple indexing strategy) for those individuals who invest in actively managed mutual funds.

The study How Well Have Taxable Investors Been Served in the 1980s and 1990s?, investigated the likelihood of after-tax outperformance. The benchmark used was Vanguard’s S&P 500 Index Fund. For the 20-year period 1979 to 1998, just 14 percent of the funds outperformed their benchmark on an after-tax basis. And importantly, the average after-tax outperformance was just 1.3 percent per annum. On the other hand, the average after-tax underperformance by the 86 percent that failed to beat par was 3.2 percent per annum.

In other words, if you had chosen to play that game, you had a slim chance of winning, and even then you would likely have won only a relatively small amount. On the other hand, you faced the high likelihood of failure. And when you did fail, you underperformed by a large amount. The conclusion of the study was that the high odds of failure with large losses combined with the low odds of success with small gains produced risk-adjusted odds against outperformance of over 15 to 1.

The story is actually even worse than it appears because the data above contains survivorship bias. 33 funds disappeared during the timeframe covered by the study. Thus, the risk-adjusted odds of outperformance were even lower than the dismal figure presented above. Compounding the problem is that, as documented in The Incredible Shrinking Alpha, the markets have become much more efficient over time — the percentage of active managers generating statistically significant alpha has collapsed since the period covered by the study. Thus, the risk-adjusted odds of outperforming would be much worse today.

The moral of the tale

You don’t have to play the game of active investing. You don’t have to try to overcome abysmal odds. The odds of outperforming through active management make the craps tables in Las Vegas seem appealing. Instead, you can outfox the box and accept market returns by investing passively.

Charles Ellis, author of Investment Policy: How to Win the Loser’s Game, put it this way: “In investment management, the real opportunity to achieve superior results is not in scrambling to outperform the market, but in establishing and adhering to appropriate investment policies over the long term — policies that position the portfolio to benefit from riding with the main long-term forces in the market.”

Important Disclosure: The opinions expressed by featured authors are their own and may not accurately reflect those of Buckingham Strategic Wealth®. This article is for general information only and is not intended to serve as specific financial, accounting or tax advice. While reasonable care has been taken to ensure that the information contained herein is factually correct, there are no representations or guarantees as to its accuracy or completeness. No strategy assures success or protects against loss. The story about Rick and Phil is hypothetical and should not be interpreted as representative of any individual’s actual experience.

LARRY SWEDROE is Chief Research Officer at Buckingham Strategic Wealth and the author of numerous books on investing.

ALSO BY LARRY SWEDROE

The implications for investors of shrinking markets

Does investor sentiment predict market movements?

The impact of Morningstar ratings on fund flows and returns

How do target-date funds affect the markets?

Is there a whelk in your fund portfolio?

PREVIOUSLY ON TEBI

Which is best for corporate bonds — active or passive?

Do financial marketplaces provide enough protection?

Who should carry the can for the Woodford blow-up?

The implications for investors of shrinking markets

Woodford underlines the need for proper advice

NEED AN ADVISER?

If you need a financial adviser, we may be able to help:

Let’s find you an adviser. Click here to get started.

© The Evidence-Based Investor MMXXI

Robin is a journalist and campaigner for positive change in global investing. He runs Regis Media, a niche provider of content marketing for financial advice firms with an evidence-based investment philosophy. He also works as a consultant to other disruptive firms in the investing sector.