By ROBIN POWELL

This article was originally written for the Suitable Advice Institute.

“Successful investing takes time, discipline and patience,” Warren Buffett once wrote. “No matter how great the talent or effort, some things just take time. You can’t produce a baby in one month by getting nine women pregnant.”

The problem for advisers is, you might be able to convince a client, intellectually, that good outcomes do indeed take time; but most people simply lack the discipline and patience that a long-term approach requires.

That’s why behavioural coaching is one of the ways — arguably, in fact, the most important way — in which an adviser adds value. Thankfully, this crucial aspect of advice is finally now being given the recognition it deserves.

Elephant in the room

But there is still, in my view, an elephant in the room — namely the type of funds that advisers tend to use.

If we really are serious about helping clients to control their emotions and to stay the course, shouldn’t we also be directing them towards solutions that make it more, not less, likely that they will manage to do so?

Despite all the evidence that clients are better off using low-cost index funds, most advisers around the world continue to favour active funds instead.

Studies have shown us time and again that on a cost- and risk-adjusted basis only a very small fraction of actively managed funds beat heir benchmarks over the long term. But another, lesser known drawback with active funds is that they also require those who invest in them to have even more discipline and patience than if they invested passively.

New research from Vanguard

This downside of active management is illustrated in a new research paper from Vanguard. Chris Tidmore and Andrew Hon wanted to discover how much “pain” active investors have to endure in order to benefit from staying invested with a long-term outperformer.

Tidmore and Hon analysed more than a thousand US-domiciled active equity funds, across different style categories, in the 25-year period up to the end of 2019. They focused purely on the most successful funds — the long-term outperformers.

Specifically, they set out to calculate the frequency, magnitude and duration of the underperformance which investors in these successful funds endured along the way.

Here are their principal findings:

Almost all long-term winners underperformed at some stage

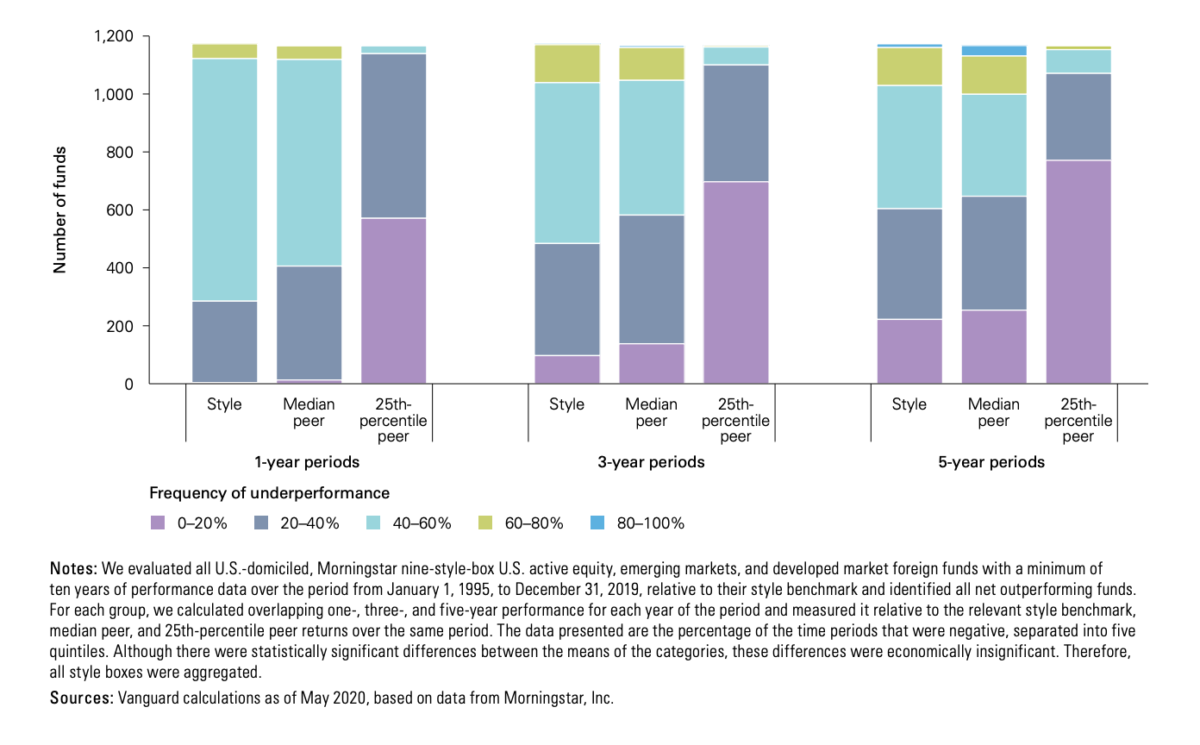

The researchers found that close to 100% of the outperforming funds they looked at experienced a drawdown relative to their style and median peer benchmarks over one-, three- and five-year overlapping time periods. 80% of outperforming funds had at least one five-year period where they were in the bottom quartile.

Underperformance was a frequent occurrence

Even among these successful funds, the researchers found, underperformance was not infrequent. About 70% of long-term outperformers underperformed their style benchmark between 40% and 60% of all one-year evaluation periods.

Figure 1: Even funds with very good records are likely to frequently underperform compared to their benchmarks

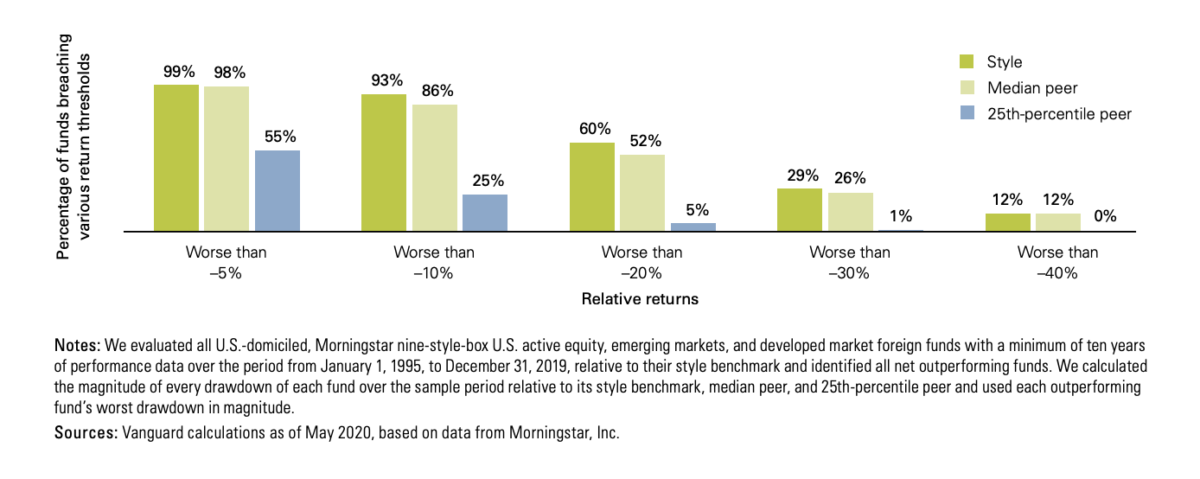

Most funds had drawdowns of more than 20%

Between 50 and 60% of the funds analysed underperformed their style and media peer benchmark by more than 20%. The average maximum drawdown was 24%.

Over a ten-year period, Tidmore and Hon discovered, investors should expect their fund manager to have, on average, one continuous drawdown relative to their style and median peer benchmark lasting two years or more.

Figure 2: The majority of outperforming funds had drawdowns greater than 20%

Remember too, that we’re talking here about the most successful funds. These are, in effect, best-case scenarios. Almost all advisers who advocate active management will occasionally pick funds that aren’t long-term winners; by doing so, they end up testing their clients’ (and ended their own) patience even more.

What about smart-beta funds?

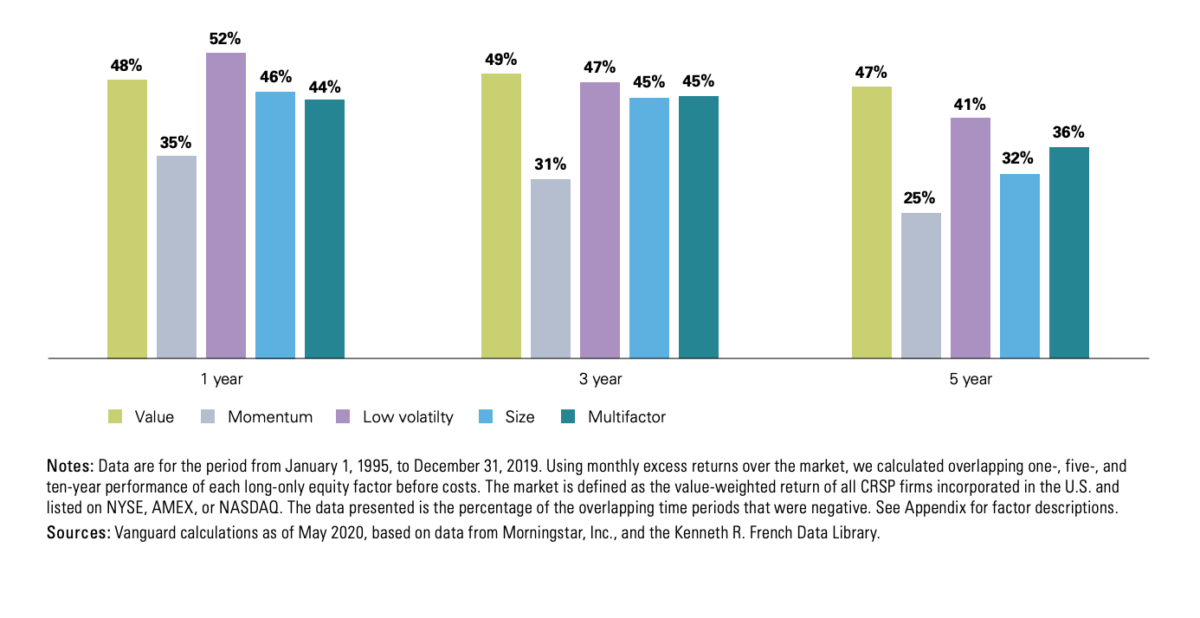

Of course, it’s not just traditional active mutual funds that investors use to try to to beat the market. So-called factor, or smart-beta, funds aim to do the same by capturing certain risk premia, such as size or value.

When Tidmore and Hon analysed these different risk factors, they found that they mostly underperformed the broader market for about half of the overlapping one-year periods.

Figure 3: Frequency of factor underperformance, as measured by percentage of overlapping time periods for which factors underperformed the market (1995-2015)

As with traditional active funds, the researchers found that underperformance occurred frequently. Value underperformed the most frequently, momentum the least.

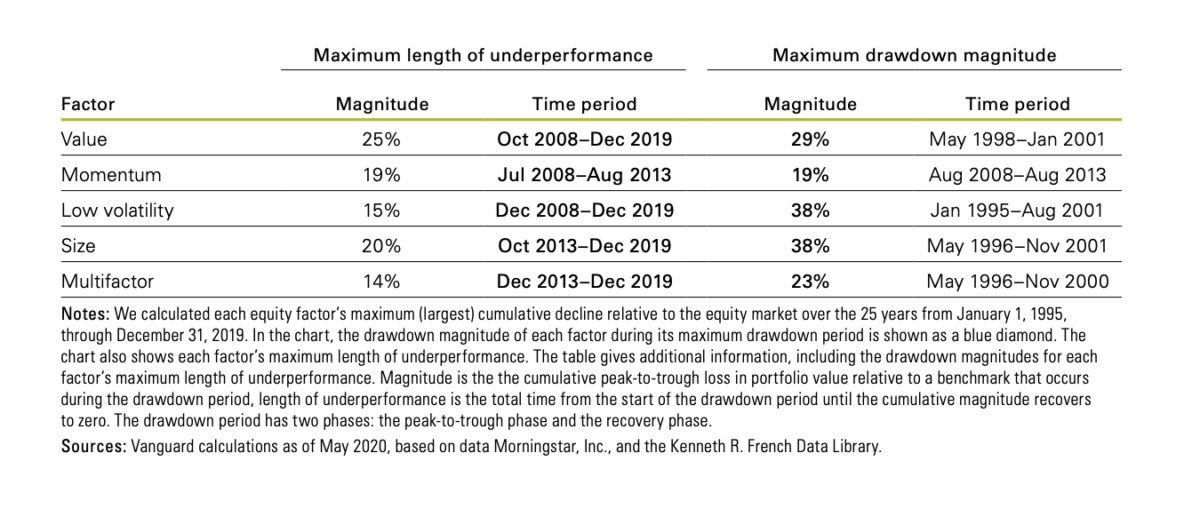

Finally, investors in factor funds also had to endure long periods of underperformance — typically around five or six years. Value, of course, has underperformed since the global financial crisis and continues to do so.

Figure 4: Across equity factors, the lengths and magnitudes of the worst periods of underperformance can be quite large

The passive alternative

There is, of course, a simple and ready-made alternative to active investing.

By putting your clients in low-cost index funds, you are effectively accepting what the evidence overwhelmingly tells us — that identifying outperforming fund managers is extremely difficult, if not impossible.

The whole philosophy of indexing is built on taking the long view. Simply by the law of averages, there are bound to be managers who beat the market from time to time. But, over long periods, only a tiny fraction of them will succeed in outperforming the market after costs.

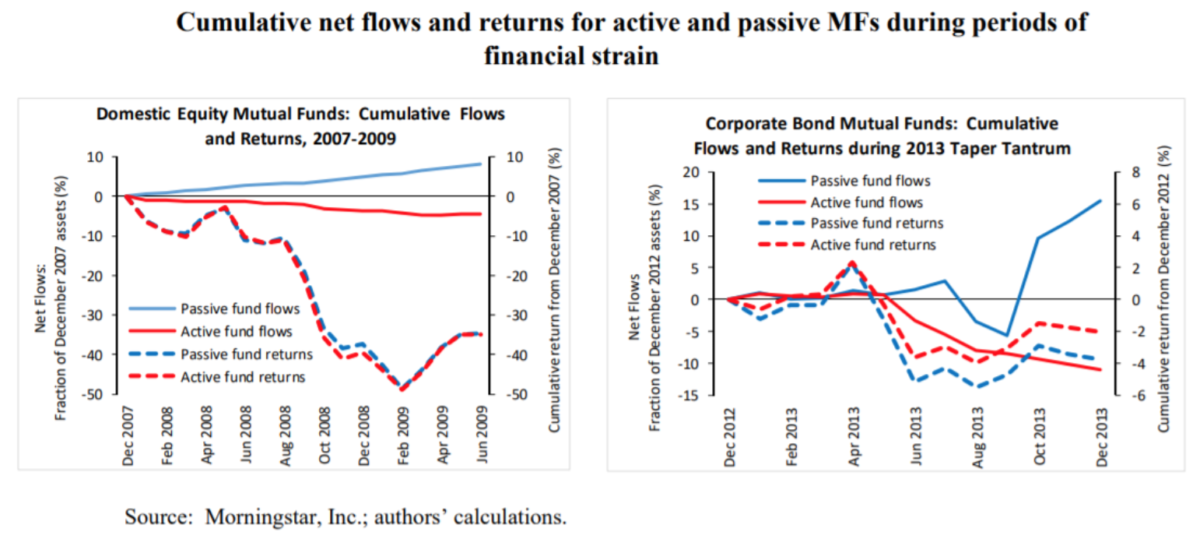

This focus on the long term perhaps helps to explain the finding in a recent research paper put out by the Federal Reserve Bank of Boston that passive investors tend to have more discipline and patience than their active counterparts.

The researchers found that flows into passive investments were less sensitive to performance than those into actively-managed alternatives. In other words, investors in index funds were more likely to stay there for the long term.

This is illustrated in the two graphs below, which show investor behaviour during the financial crisis in 2008, and the market dip that occurred during the s0-called “taper tantrum” of 2013.

Figure 5: Passive investors are better at sticking with it when market volatility strikes

Implications for advisers

So, what does this research mean from a suitability perspective? And what lessons can advisers learn from it?

The most important takeaway is that clients need to be especially patient if they use actively managed funds. An adviser may therefore decide that a particular client simply isn’t cut out for active investing.

Even if the client does have the right temperament, it is even more important when using active funds that the adviser ensures that they are properly educated about the risks involved, and that they receive the ongoing behavioural coaching they need.

There is, in short, more work for the adviser to do with active management. And that applies equally to factor investing as it does to investing on traditional active funds.

Yes, certain factors have outperformed in the past, but there is no guarantee that they will do so in the future. Advisers have to ensure that clients investing in factor funds have the temperament, education and coaching required to keep them invested for the long haul.

As Tidmore and Hon explained, advisers can reduce capitulation risk by adopting a multi-factor approach — in other words, by diversifying across different factors — but that still won’t protect clients from long periods of underperformance. Multi-factor investing has underperformed the broader market since December 2013 and still does so today.

Conclusion

Unless human nature changes, discipline and patience will continue to play a far bigger part in investor outcomes than effort, knowledge or skill.

As an adviser, therefore, one of the biggest challenges you face is persuading your clients to stick with their investments through thick and thin. And it’s not easy.

Why, then, would you choose funds for your client that will only make your job even harder than it needs to be?

ROBIN POWELL is the founding editor of The Evidence-Based Investor. He works as a journalist and consultant specialising in finance and investing. You can find him here on here on LinkedIn and here on Twitter.

PREVIOUSLY ON TEBI

Here are some other recent posts you may have missed:

Getting comfortable with your enough

Always confident but often wrong

Cost is a huge factor for non-profit endowments

CONTENT FOR ADVICE FIRMS

Through our partners at Regis Media, TEBI provides a wide range of content for financial advice and planning firms. The material is designed to help educate clients and to engage with prospects.

As well as exclusive content, we also offer pre-produced videos, eGuides and articles which explain how investing works and the valuable role that a good financial adviser can play.

If you would like to find out more, why not visit the Regis Media website and YouTube channel? If you have any specific enquiries, email Sam Willet, who will be happy to help you.

Picture from A Saint of the Eastern Church (formerly called A Greek Acolyte), 1867-8

Simeon Solomon (d.1905), via Birmingham Museums Trust