By JOACHIM KLEMENT

Every language has words that are not translatable into other languages. I have written about the German term “abgeschossene Halbbildung” before, but today, I want to focus on an English expression that is unknown in German (and I think in many other languages): Property ladder.

Why are Brits and Americans so obsessed with owning their own home and getting on the property ladder as soon as possible?

A few years back, I conducted a little experiment with audiences in the UK and the US. I would ask them to raise their hands if they thought stocks are riskier than real estate. Most hands went up. Then, I asked them to raise their hands if they thought stock returns were higher than real estate returns. Less than half raised their hands. In effect, people were telling me that stocks were riskier than real estate and provided less return. I cannot do that exercise anymore today, because after a 10-year bull market in stocks, perceptions have shifted – until the next bear market, when they will change once more.

If you think that property has lower risk but similar or higher returns as stocks, it makes sense to buy a house and use it as the main vehicle to build wealth as so many people in the UK and the US do. But finance theory tells us that in the long run the assets with the higher systematic risks (stocks) should also have the higher return. And this is indeed what we observe empirically.

David Chambers and his colleagues collected the data of the property investments of four large UK universities from 1901 to 1970. What they found was that property investments for these elite colleges that were run by some of the brightest minds of the 20th century (John Maynard Keynes managed the Endowment of King’s College, Cambridge, from 1921 to 1946) were far lower and more volatile than previously thought.

Real capital returns for commercial property was -1.5% per year and for residential property -0.2%. It was only the sizeable net yield of property investments that created a positive total return after inflation. For commercial property, they calculated a total real return of 2.1% and for residential property of 2.8% per year. That doesn’t sound great to me.

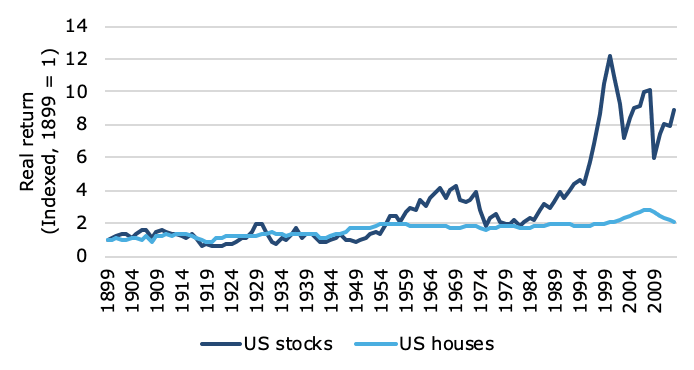

The picture is the same if you take a longer-term view. Òscar Jordà and his colleagues measured house prices and stock market developments for seven countries from 1870 to 2015. The chart below shows the real return of US stocks vs. US houses since 1900. The annual real return of stocks was more than three times the return of houses. And in the UK, you find stock returns that are about twice that of property returns.

Real US stock and house prices since 1899.

Source: Jordà et al. (2019)

Why do people think that property investments are so much better than stocks?

Because they don’t see the volatility of property prices on a daily basis. Real estate is so illiquid that people tend to have only two price points: the amount they paid for it when they bought the house and the amount they sold it for. And because most people don’t buy and sell houses on an annual basis (at least not since the US housing bubble burst in 2006), they don’t see how prices went up and down over time. All they see is a sale at a higher price than what they paid for it some ten years ago or so. And hardly anybody bothers to calculate what the actual annual return was. So they are fooled into believing that property has high returns and very little volatility.

But this illiquidity of real estate does not only have disadvantages. In fact, from a behavioural perspective, the Anglo-Saxon obsession with owning your house might make perfect sense for two reasons:

1. Because houses are illiquid, you can’t just sell them whenever prices decline. Unlike in stock markets, people are forced to hold on to their investment for many years. And because we know that investors tend to buy and sell stocks at the worst time (and thus destroy performance), the realised returns of their property investments might be higher than their realised returns from their stock market investments.

2. Because people use a lot of leverage to buy a house, they are forced to pay a certain amount each month on the mortgage. If the mortgage is not an interest-only mortgage but amortises over time, then this is like forcing yourself to save for the future. We know that people tend to save too little for retirement. But we also know that people tend to buy the biggest and nicest house they can afford. And by doing so, they might inadvertently force themselves to save a lot of money for the future that they can tap into if they sell their house.

With these two behavioural effects in mind, I think that getting on the property ladder might not be the worst idea for many investors, even though the actual returns of properties are lower than we might think.

JOACHIM KLEMENT is a London-based investment strategist, who also writes on the topic for his blog: Klement on Investing.

Image: Tierra Mallorca (via Unsplash)