By ROBIN POWELL

“The historical data support one conclusion with unusual force,” the late Jack Bogle once wrote. “To invest with success, you must be a long-term investor.” Yet most people aren’t.

I’m constantly struck at this time of year at how focused on the very short term most people in the financial world are.

People who should know better — professional investors, brokers, financial advisers and journalists — seem to be queuing up to give us their forecasts on what’s going to happen in the financial markets over the next 12 months.

Of course, in any one year, markets can go sharply up or down. But, in the great scheme of things, one circuit of the sun is a very short timescale. Investors should have a much kinder time horizon than that.

This is an appropriate time, then, to remind ourselves of some of the most important lessons from financial market history.

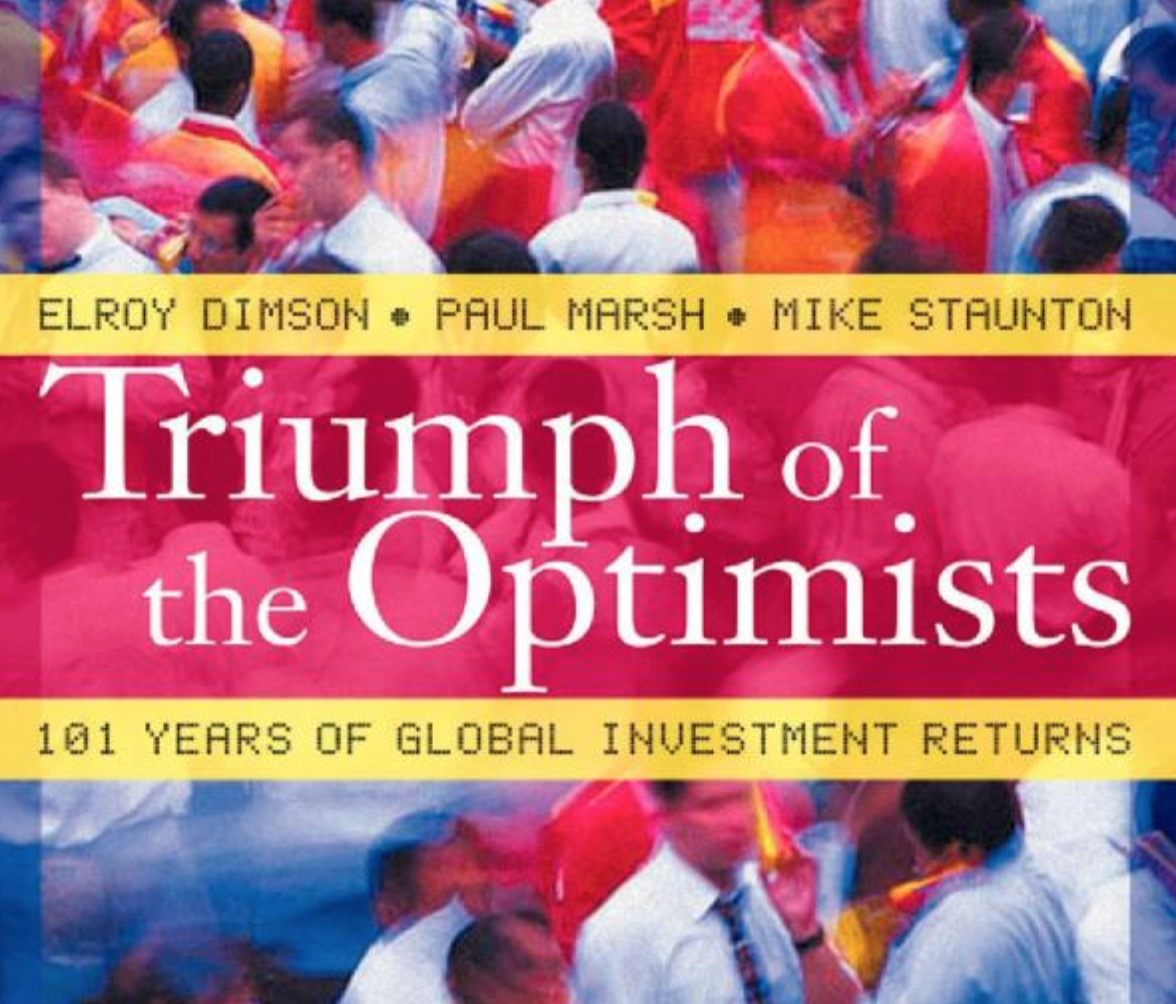

We’ve written several times about the work of Elroy Dimson from Cambridge Judge Business School and TEBI’s strategic partner, Sparrows Capital. Professor Dimson is probably best known for the book Triumph of the Optimists, which he co-authored with Paul Marsh and Mike Staunton.

The book analyses the returns of a wide range of asset classes in countries all over the world from 1900.

Here are eight key takeaways from Triumph of the Optimists, to help us put all those New Year market forecasts in perspective.

1. Most investors are over-exposed to their domestic stock market

“Most investors hold a disproportionate part of their funds in a less-than-fully-diversified portfolio of domestic securities. Investors, in whatever country they are located, should take account of the full range of future possibilities for capital market performance.”

2. The likely long-term returns from equities are worth having

“The likely rewards from equity market investing are worth having over the long haul. Downside risk is always present (but) the chance of underperforming government securities shrinks with a longer horizon.”

3. We can expect equities to provide higher returns than less risky assets

“(The outperformance of equities) is not simply a pattern from the past; it reflects the theory that risky securities should command a lower price than otherwise similar safe securities. Risky equities can therefore be expected to offer a higher expected return.”

4. The cost of investing is a significant contributor to underperformance

“The costs borne by investors… are largely avoided by tax-efficient index funds. It is no surprise that mutual funds around the world tend to underperform on an after-fees and -costs basis.”

5. Investment risk is reduced though global diversification

“While stock market anomalies may be illusory, one ‘free lunch’ is still on offer in the investment world — risk reduction through international diversification. Investment risk is lowered in a worldwide portfolio.”

6. Holding a diversified portfolio for the long term is a sensible strategy

“We favour holding stocks for the very long run… They should be held as part of a diversified portfolio, including multiple asset classes from more than one country.”

7. Failing to diversify and to control costs erodes investment returns

“Investors who fail to diversify efficiently and/ or who overpay for asset management services can expect to erode their reward for equity risk exposure.”

8. Long-term optimists have been amply rewarded

“By the middle of the twentieth century, investors had little cause for optimism… Who but the most rampant optimist would then have dreamt that over the next half-century, the annualised real return on equities would be 9%? Yet this is what happened.”

Robin is a journalist and campaigner for positive change in global investing. He runs Regis Media, a niche provider of content marketing for financial advice firms with an evidence-based investment philosophy. He also works as a consultant to other disruptive firms in the investing sector.