We’ve looked several times on TEBI at the question of whether ESG funds outperform traditional funds over the long term, and the jury still appears to be out. Morningstar recently analysed the performance of 4,900 funds in an attempt to answer the question. Again, there isn’t an obvious winner. But, as HORTENSE BIOY explains, the fees that sustainable investors pay are a crucial factor in their chances of success.

Despite the increased popularity of sustainable funds, concerns remain about a potential performance trade-off. A growing body of research shows that sustainable investing has a positive effect on investment performance, but other research shows, as well, that there isn’t a clear link between firms’ environmental, social and governance attributes and performance.

To find out how these funds stack up, Morningstar has analysed the performance of sustainable funds in seven Morningstar Categories, comparing average returns, success rates, and survivorship rates over 10 years for sustainable funds versus traditional funds.

What you need to know about sustainable investing

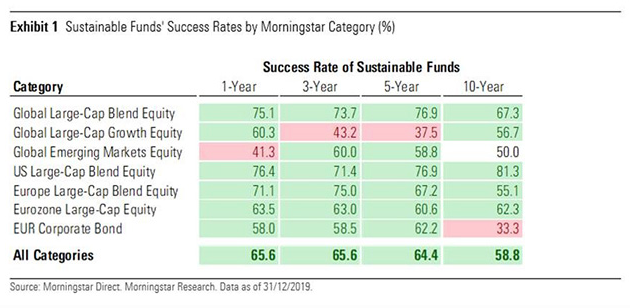

A majority of surviving sustainable funds (those that existed ten years ago and still exist today) outperformed their average surviving traditional peer. The above-50% success rates for surviving sustainable funds in most categories over multiple time periods indicate that investors taking the ESG route were less likely to miss out on returns than if they had invested in traditional funds.

Over the ten-year period through 2019, 58.8% of surviving sustainable funds across the seven categories considered have beaten their average surviving traditional peer.

The odds of picking a winning sustainable fund over the past 10 years were greatest in the US large blend category. More than seven out of ten live sustainable US large-cap equity funds delivered higher returns than their average surviving conventional counterpart.

But the same can’t be said about global large-cap growth investors who would have seen their odds of success fluctuate significantly over time. Barely four sustainable global large-cap growth funds out of 10 selected five years ago and still available today beat the average surviving traditional peer.

Meanwhile, sustainable funds have consistently exhibited higher survivorship rates than traditional funds over the past 10 years, meaning fewer sustainable funds have closed, in relative terms.

On average, 77.3% of sustainable funds available to investors 10 years ago have survived, compared with less than half (46.4%) of traditional funds.

Fees are crucial

While the majority of sustainable funds across the seven categories considered here have beaten their average traditional peer over the past 10 years, success rates have varied depending on fees.

Selecting a fund in the lowest-fee quartile five years ago would have improved the odds of picking a winner in all but one category — Global large-cap growth, where just 33% of the cheapest sustainable funds beat the cheapest traditional funds.

The growing proportion of passive (or tracker) sustainable funds may have helped this trend, as passive funds tend to be cheaper than their active counterparts.

In some categories, for example the global and US large-cap blend categories, where sustainable funds’ success rates have the highest, the percentage of passive sustainable funds has been higher than that of traditional funds. Lower fees offered by passive funds have contributed to the higher success rates.

What about global ESG funds?

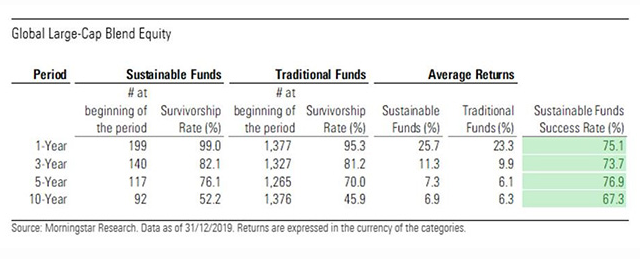

The success rates for sustainable funds in the Global Large-Cap Blend Equity category have been among the highest over multiple time periods. Over 10 years the average sustainable fund in the category has delivered annualised returns of 6.9%, compared with 6.3% for traditional funds. Over three years, they have delivered 11.3% and 9.9% respectively.

Investors in this category should, however, be mindful of the low survivorship rate over the long term. Only 52.2% sustainable funds available 10 years ago have survived to today. Although it’s worth pointing out that this is still a better ratio than for traditional funds (45.9%).

Meanwhile, the success rates for surviving sustainable US large-cap blend equity funds have been among the most consistently high over multiple time periods. The survivorship rate of sustainable funds have been also very high, especially in comparison with traditional peers’ in this category. Some 84.2% of US large-cap blend funds available 10 years ago remain open. This contrasts with only 46.9% for conventional peers.

ESG funds in the COVID-19 sell-off

Sustainable funds held up better than their traditional counterparts during the Covid-19 sell-off in the first quarter of the year, outperforming in all but one category considered in the study. The global large-cap growth category was again the exception, with less than half of sustainable funds in that category beating their average conventional peer, on average they lagging by 0.11%.

The overall outperformance of sustainable funds during the Covid-19 sell-off in the first quarter can be explained by a combination of factors. Firstly, being underweight in less ESG-friendly sectors like oil & gas and overweight in technology and healthcare benefitted many sustainable portfolios. Traditional factors such as quality and low volatility have also played a role.

Finally, companies that score high on ESG tend to be well-run businesses that treat their stakeholders well, address their environmental challenges, enjoy more conservative balance sheets, and have lower levels of controversies. Many such companies tend to be more resilient during market downturns.

HORTENSE BIOY is Director of Sustainability Research for Morningstar’s EMEA division. This article was first published on the Morningstar blog.

For more insights from Hortense’s colleagues, take a look at these other recent articles:

US fund fees cut in half in 20 years

Three risks you take when choosing a thematic fund

Is market-cap indexing a form of momentum investing?

A critical look at the arguments against index investing

US value and growth performance under the microscope

What are the world’s highest fund fees?

Picture: Karsten Würth via Unsplash