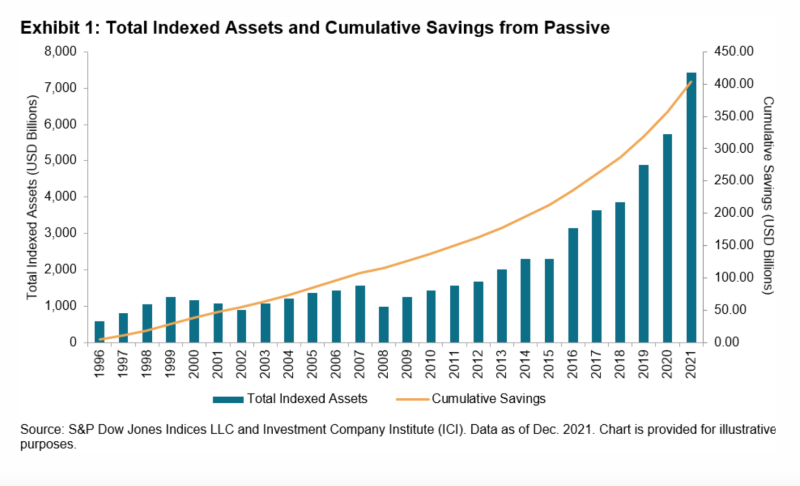

Asset management, as Robin Powell, recently wrote, is the scary bill you never see. It’s huge, and if investors were actually presented, every month, with a pounds-and-pence or dollars-and-cents figure for how much they’re paying, most would be horrified. The good news is, of course, that there is a very much cheaper alternative to traditional active funds, and that’s low-cost index trackers. As ANU GANTI from S&P Dow Jones Indices explains, indexing saved investors a staggering $403 billion since 1996.

One of the benefits of indexing is its low cost relative to active management. As indexing has grown, investors have benefited substantially by saving on fees and avoiding active underperformance. We can estimate the fee savings each year by multiplying the difference between the average expense ratios of active and index equity mutual funds by the total value of indexed assets for the S&P 500®, S&P 400® and S&P 600®. When we aggregate the results of these annual computations, we observe that the cumulative savings in management fees over the past 26 years is USD 403 billion (see Exhibit 1).

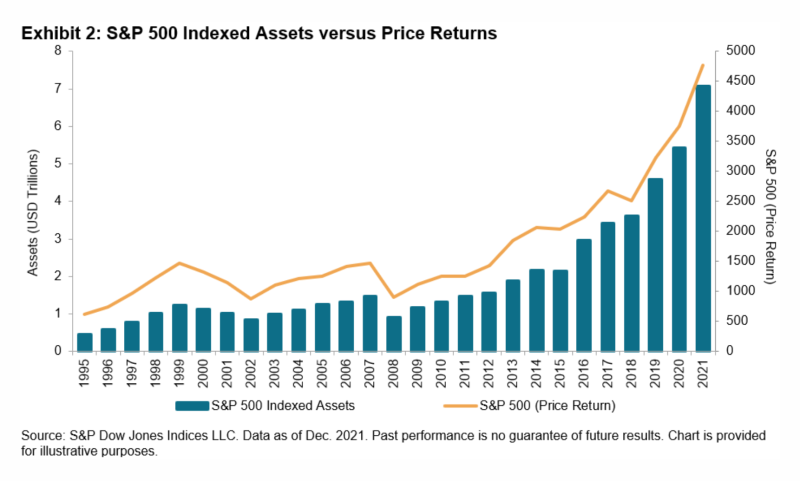

Of course, this USD 403 billion estimate understates the full cost savings of the index industry, since it encompasses indices only from S&P Dow Jones Indices (and not all of those). Our recent Annual Survey of Indexed Assets shows a 30% surge in assets tracking the S&P 500 since 2020 to USD 7.1 trillion as of December 2021. Exhibit 2 illustrates that since 1995, this growth (CAGR of 11.1%) has outpaced the growth due to market gains (CAGR of 8.2%), indicating a substantial increase in flows.

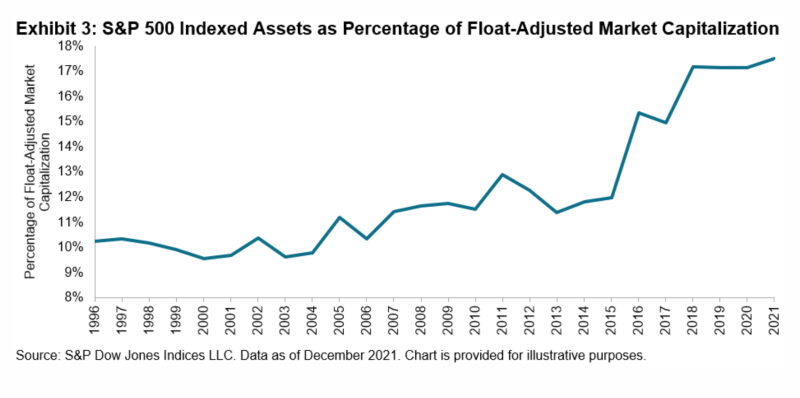

To provide context on the size of the passive market, Exhibit 3 divides S&P 500 indexed assets historically by the float-adjusted market capitalization of the S&P 500. This percentage has stabilised at approximately 17% since 2018, indicating that the potential for future passive growth is promising.

Obviously, the cost savings generated by the shift from active to passive management would be inconsequential if investors lost more in performance shortfalls than they gained in reduced fees. As readers of our SPIVA reports are well aware, of course, that’s decidedly not the case: most active managers underperform most of the time. In the 20 years ending in 2021, 94% of all large-cap U.S. managers lagged the S&P 500. Mid- and small-cap results were almost equally disappointing. The rise of passive management has been a notable consequence of active performance shortfalls.

ANU GANTI is Senior Director, Index Investment Strategy, at S&P Dow Jones Indices.

PREVIOUSLY ON TEBI

Mutual fund alpha as a predictor of stock returns

How good are analysts at forecasting earnings growth?

Valuations and earnings growth rates

Start planning the life you want to lead

The major incentive problem at the heart of active management

FIND AN ADVISER

Investors are far more likely to achieve their goals if they use a financial adviser. But really good advisers with an evidence-based investment philosophy are sadly in the minority.

If you would like us to put you in touch with one in your area, just click here and send us your email address, and we’ll see if we can help.

Picture: Alexander Schimmeck via Unsplash

© The Evidence-Based Investor MMXXII