Many investors choose to save for retirement in so-called “lifestyle funds”. Alternatively, they may choose a “lifestyling” option. Either way, it means that your investments are diversified and have varying risk levels, depending on your age or how close you are to retirement. The logic behind reducing your risk as you approach retirement is sound, and lifestyle funds can be a sensible solution. But, as LARRY SWEDROE explains, the evidence suggests that there is a penalty to pay for investing in lifestyle funds, particularly for US taxpayers, and you can achieve better results, relatively simply, using low-cost index funds.

One thing the mutual fund industry does well is to create product and then create demand for it, even when the product may not be in investors’ best interests. Variable life insurance, most variable annuities and hedge funds generally fit into the category of products that are meant to be sold, not bought. One mutual fund product that has proliferated in recent years is the balanced, or lifestyle, fund. A lifestyle fund manages a diversified portfolio across assets with varying risk levels based on the individual investor’s risk tolerance, age and investment goals.

The idea of the product is fundamentally sound—create a fund of funds that invests in various asset classes. These funds can be structured to accommodate investors covering the full spectrum from aggressive (100% equity allocation) to very conservative (20% equity allocation). And these funds provide the following benefits:

- Allow investors to hold in one fund a diversified portfolio that can include exposure to both U.S. and international (typically developed markets and possibly emerging markets) equities.

- The fund automatically rebalances its assets to the targeted exposures, providing discipline. Thus, the fund’s allocation stays the same over time, unlike target-date funds, which become more conservative and shift most of their allocation from stocks to bonds as the person approaches retirement.

- If the fund is not an all-equity fund, it will also rebalance between equities and fixed income, again, providing discipline.

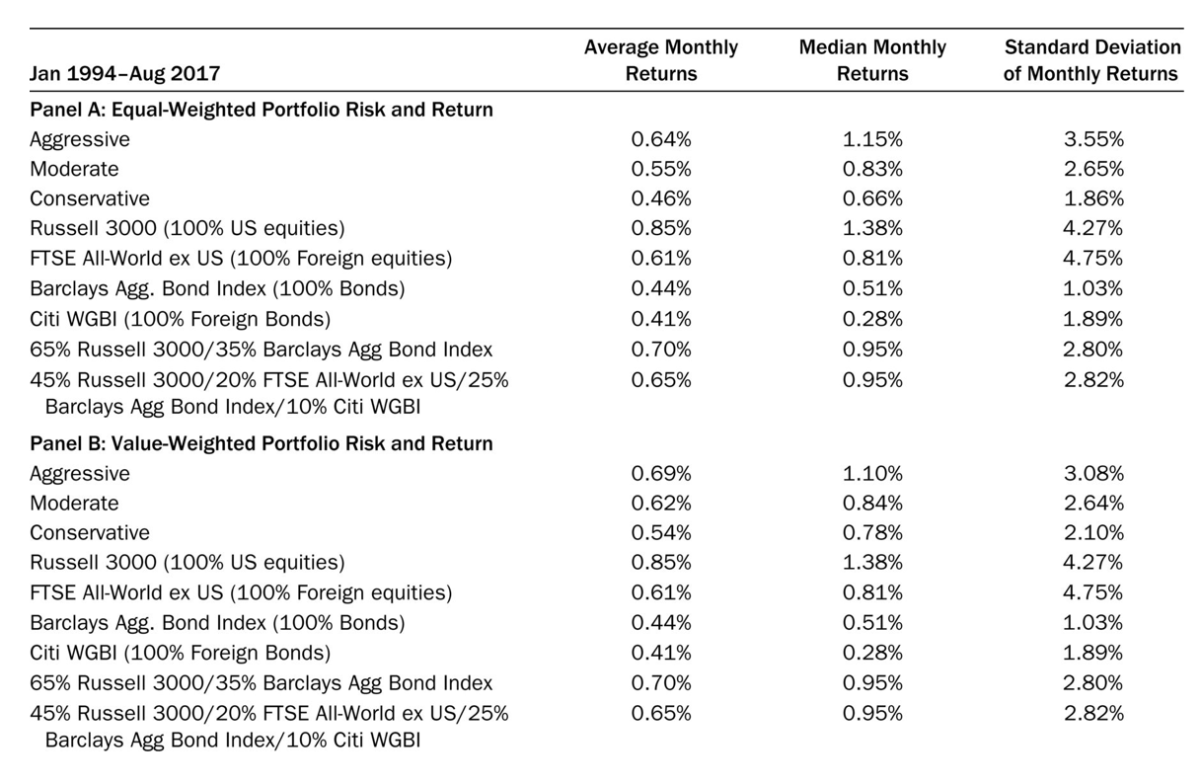

Have the benefits been worth the costs (the expense ratio of the lifestyle fund)? Srinidhi Kanuri, author of the paper An Empirical Examination of Lifestyle Mutual Funds, published in the Winter 2022 issue of The Journal of Retirement, examined the performance of a comprehensive list of all lifestyle funds (surviving as well as dead) from the Morningstar Direct database from January 1994 through August 2017. Morningstar classified these funds as:

▪ Aggressive funds, which have a 70% to 85% equity allocation

▪ Moderate funds, which have a 50% to 70% equity allocation

▪ Conservative funds, which have a 30% to 50% equity allocation.

While the lifestyle fund maintains the same allocation over time, investors do have the ability to switch to lifestyle funds with different allocations as they age or if there is a change in their ability, willingness or need to take risk. At the end of the period, these funds were managing about $1.4 trillion dollars in assets.

Kanuri compared the returns of the lifestyle funds to the performance of the U.S. stock market (the Russell 3000 Index), the bond market (Barclays Aggregate Bond Index) and the foreign stock market (FTSE All-World ex US Index). Two portfolios were formed:

▪ 65% US equities (Russell 3000)/35% bonds (Barclays Aggregate Bond Index)

▪ 45% US equities (Russell 3000)/20% foreign equities (FTSE All-World ex US Index)/25% bonds (Barclays Aggregate Bond Index)/10% foreign bond (Citi WGBI)

Kanuri also evaluated the performance relative to a seven-factor model: the Carhart four-factor model (beta, size, value and momentum) plus the excess returns of the Barclays Aggregate Bond Index, Citi World Government Bond Index and FTSE All-World ex US Index to account for the fact that lifestyle funds have a significant chunk of their portfolios allocated to foreign bonds and foreign stocks. Following is a summary of his findings:

- Fund expense ratios were very high compared to benchmark index funds. The average expense ratio for aggressive, moderate and conservative funds was 0.85%, 1.16% and 0.93%, respectively. This has negative implications for returns.

- Fund turnover was high across all three categories. Average turnover for aggressive, moderate and conservative fund categories was 47%, 125% and 71%, respectively. This has negative implications for trading costs and tax efficiency (if held in a taxable account).

- All three styles held significant cash, creating a drag on returns: conservative funds (12.8%), aggressive funds (6.2%) and moderate funds (10.3%).

- On both an equal-weighted or value-weighted basis, all lifestyle fund categories underperformed all benchmark indexes.

- The benchmark indexes used had a higher risk-adjusted performance (Sharpe, Sortino and Omega ratios) compared with all three lifestyle fund categories.

- Relative to the seven-factor model, the monthly net alphas of equal-weighted portfolios were negative for all three categories over both the full period (January 1994-August 2017) and two sub-periods (January 1994-December 2006 and January 2007-August 2017). The R-squared values were all above 0.966, indicating the model did a good job of explaining returns. Results were statistically significantly at 1% for all three categories. For value-weighted portfolios, the results were insignificantly negative and the R-squared values were all above 0.92.

- On a gross basis, all three lifestyle fund categories still underperformed but with alphas insignificantly different from zero—lifestyle mutual funds are successful in security selection, but fees charged to deliver outperformance are too high.

- In terms of market timing, none of the three categories showed evidence of the ability to generate alpha.

- Vanguard’s S&P 500 and Vanguard Bond funds outperformed all three lifestyle fund categories with superior risk-adjusted performance (Sharpe, Sortino and Omega ratios).

His findings led Kanuri to conclude: “All of these results indicate that lifestyle funds have underperformed the passive benchmark indexes and index funds with lower absolute and risk-adjusted performance.”

Investor takeaways

Kanuri’s evidence demonstrates that actively managed lifestyle funds are likely to subtract rather than add value and that investors are better off building their own “lifestyle” portfolio using low-cost index funds or other low-cost systematic strategies. While the evidence is compelling, unfortunately there are still other negative features of lifestyle funds that should be not be ignored, which is discussed in my book, co-authored with Kevin Grogan and Tiya Lim, The Only Guide You’ll Ever Need for the Right Financial Plan: Managing Your Wealth, Risk, and Investments.

- For investors with the ability to choose their asset location (taxable versus tax-advantaged accounts), combining equities and fixed income assets in one fund could result in the investor holding one of the two assets in a tax-inefficient manner. If the lifestyle fund is held in a taxable account, the investor is holding the fixed income assets in a tax-inefficient location. If the fund is held in a tax-deferred account, the equities are being held in a tax-inefficient location (losing the benefits of long-term capital gains treatment, the ability to loss harvest, the ability to use the asset as a means of making a charitable contribution and avoiding the capital gains tax, and the potential for a step-up in basis upon death).

- If the fund is held in a taxable account, the investor loses the ability to loss harvest at the individual fund level.

- If the fund is in a tax-deferred account, the investor loses the ability to use any foreign tax credits that are generated by the international equity holdings. Even in a taxable account, as a fund of funds, the investor loses the ability to utilise the foreign tax credit.

- If the fund is held in a taxable account, the equities should be in funds that are tax managed, or in ETF instead of mutual fund form. I am not aware of any lifestyle or balanced fund that tax manages the equity portion (which makes sense because the fund does not know which location it will be held in).

- For investors who manage their own IRA accounts, the fixed income allocation will not include CDs or MYGAs (multi-year guaranteed annuities), both of which can provide higher yields than Treasuries without incurring credit risk (if one stays within insurance limits) while also avoiding the lifestyle fund’s expense ratio. In addition, Treasury bonds, a typical lifestyle fund holding, can be purchased by individuals without any expense ratio.

Individually, each of the above are important negative features that impact the after-tax return of the fund. Collectively, they can be very damaging. The bottom line is that unless an investor is holding all their investable assets in a tax-deferred account, lifestyle funds are not likely a good choice. The more efficient investment strategy is to hold the individual assets in separate funds and in the most tax-efficient location. The key is to then have the discipline to rebalance and adhere to your well-thought-out plan.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, however its accuracy and completeness cannot be guaranteed. Indices are not available for direct investment. Their performance does not reflect the expenses associated with the management of an actual portfolio nor do indices represent results of actual trading. Information from sources deemed reliable, but its accuracy cannot be guaranteed. Performance is historical and does not guarantee future results. Total return includes reinvestment of dividends and capital gains. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of the Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the accuracy of this article. LSR-22-237

LARRY SWEDROE is Chief Research Officer at Buckingham Strategic Wealth and the author of numerous books on investing.

ALSO BY LARRY SWEDROE

New evidence on how investor emotions affect markets

Are short sellers’ target prices too pessimistic?

How funds change benchmarks to flatter their performance

Value versus glamour stocks: a regime shift in the making?

We’re seeing a virtual repeat of the dot-com crash

© The Evidence-Based Investor MMXXII