There has been a large increase in recent years in the number of specialised ETFs that offer exposure to different investment themes. But a new study has confirmed that thematic funds tend to underperform — and the very worst time to buy them is when they launch. That is mainly because specialised ETFs usually launch just after their theme has peaked, and immediately before a steep fall in returns. LARRY SWEDROE has the details.

Since the introduction of the first ETF in 1993, more than 3,400 exchange-traded funds (ETFs) have been launched in the U.S. alone, with more than 1,000 investing in U.S. equities. By mid-2021 ETFs had captured more than $9 trillion in assets globally. ETFs have captured market share by offering investors the ability to track various indexes (or invest in various asset classes or thematic strategies) at lower costs (with expense ratios as low as 3 basis points), lowering fees, providing greater tax efficiency for taxable investors and allowing investors to trade during the day.

In their December 2021 study Competition for Attention in the ETF Space, authors Itzhak Ben-David, Francesco Franzoni, Byungwook Kim and Rabih Moussawi examined how the interplay between investors’ demand and providers’ incentives has shaped the evolution of ETFs. Their data sample included ETFs traded in the U.S. from the Center for Research in Security Prices (CRSP) between 1993 and 2019. Although all U.S. equity ETFs were included in the sample, some of the data items (e.g., holdings data) had limited availability in the pre-2000 period. Given data limitations, most of their empirical analysis began in January 2000, including all ETFs launched earlier, and ended December 2019. The sample contained 554 broad-based (90 broad index and 464 smart beta) ETFs and 526 specialised (411 sector/industry and 115 thematic) ETFs. Following is a summary of their findings:

- The ETF industry evolved along two separate paths. Early ETFs invested in broad-based indexes (mean/median expense ratio of 0.42 percent/0.35 percent), providing diversification at a low cost. Later products tracked niche (specialised, thematic, sector-based) portfolios and charged higher fees (mean/median expense ratio of 0.55 percent/0.58 percent) — investors who buy these ETFs are willing to overlook the higher fees or loss of diversification as long as they can gain exposure to their desired investment themes or can attempt to gain alpha.

- The specialised offerings cater to investor demand (sentiment) for popular, yet often overvalued, investment themes — stocks that are included in specialised ETFs have been favourably covered in the media. For example, in 2019 new ETFs included products focusing on cannabis, cybersecurity and video games. In 2020 new specialised ETFs covered stocks related to the Black Lives Matter movement, COVID-19 vaccines and the work-from-home trend. In 2021, tracking the recovery after the COVID recession, new specialised ETFs covered the travel industry and space travel as well as real estate and construction. The sentiment of the media, however, drops sharply after the time of ETF launch.

- The portfolio of specialised stocks displayed significantly higher earnings growth forecasts on average. These forecasts became increasingly more positive in the period leading up to the launch. However, after the ETF launch, these stocks experienced a marked downward revision in growth expectations. No such pattern was found for the stocks in the broad-based portfolios.

- While competition in the broad-based index category has led to a trend toward even lower fees, specialised ETFs fees have remained at higher levels.

- In 2019 specialised ETFs managed 18 percent of the industry’s assets, yet they generated about 36 percent of the industry’s fee revenues.

- Specialised ETFs generated more volatile returns than did broad-based ETFs—not surprising, as they hold fewer names.

- Flows to broad-based ETFs displayed a significantly higher sensitivity to fees, whereas flows to specialised ETFs were unrelated to fees and responded more strongly to past performance. Their low fees allowed the broad-based ETFs to show risk-adjusted returns after fees to be just slightly negative, though statistically indistinguishable from zero, versus the Fama-French-Carhart four-factor model (-0.24 percent per annum after fees).

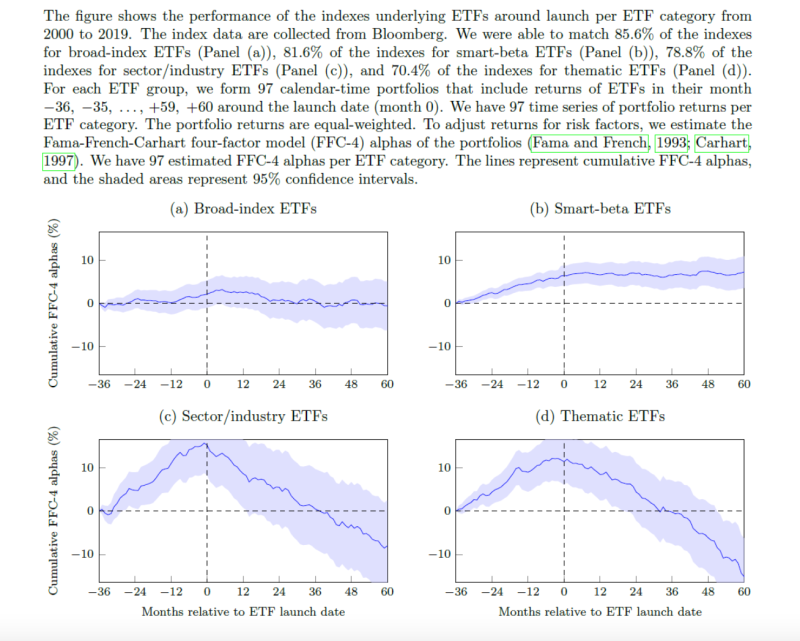

- ETF providers are unable to identify sectors and themes that deliver positive risk-adjusted returns. A portfolio of all specialised ETFs achieved risk-adjusted (relative to the four-factor model) returns of -3.24 percent per annum after fees. The results were only about half as bad when benchmarked against the Fama-French five-factor model. The underperformance could not be explained by high fees or hedging demand—they were driven by the overvaluation of the underlying stocks at the time of the launch (subject to recency bias, investors are performance chasers) that was reversed post-launch.

- The underperformance of specialised ETFs is especially severe in the first few years after their launch. Over their first 60 months, specialised ETFs generated four-factor alphas of -6.0 percent (t-stat = 4.0). Beyond 60 months alphas were -1.4 percent, a significant improvement, though still economically (though not statistically) significant (t-stat = 1.5).

- Specialised ETFs that were launched following lower prelaunch returns and media sentiment underperformed less—by “only” -2.4 percent per year. In contrast, specialised ETFs with portfolios in which stocks experienced prelaunch high returns and high media sentiment underperformed by 6.4 percent a year.

- There was no evidence of hedging motives for the specialised ETFs, for which investors were willing to pay an insurance premium.

- Specialised ETFs were more likely to experience capital outflows over their existence and experienced closures at a significantly higher rate (and the likelihood of closure was more sensitive to past performance).

- The price impact of flows could be sizeable under certain assumptions — negative flows could amplify the underperformance of specialised ETFs by up to 2.7 percent per year over the five-year horizon since inception.

- Retail investors are likely to own a greater share of the specialised ETFs universe than that of the broad-based ETF universe — unsophisticated investors are more likely to be attracted to specialised ETFs. As an example, the number of Robinhood users scaled by market capitalisation was substantially higher for specialised ETFs than for broad-based ETFs in their first year of existence.

Overall, the cumulative evidence in the study supports the hypothesis that ETF providers cater to performance-chasing investors. Specifically, they launch new ETFs focused around themes that are popular among naive investors. The excitement around these popular investment themes, however, means that the related securities tend to be overvalued. As a result, the portfolios of new specialised ETFs tend to contain overvalued securities. As illustrated below in Figure 6 from the paper, the overvaluation dissipates over time, delivering poor returns to investors who chased performance.

Performance of the indexes underlying newly-launched ETFs

Their findings led Ben-David, Franzoni, Kim and Moussawi to conclude: “Our results are consistent with providers catering to investors’ extrapolative beliefs by issuing specialised ETFs that track attention-grabbing themes. … Before ETFs inception, smart beta, sector/industry, and thematic ETFs, experience a price run-up.”

The authors noted that their findings are consistent with prior literature showing that “mutual funds cater to investor sentiment in order to attract flows by heavily weighting past winners and changing their names to trendy ones.” They found that their measure of media sentiment (the sum of each news article’s composite sentiment score from RavenPack scaled by market capitalisation) was 0.22 for broad-based ETFS but almost three times that, at 0.64, for specialised ETFs.

Ben-David, Franzoni, Kim and Moussawi also found that the stocks held by specialised ETFs displayed more positive skewness (0.17 versus 0.01), which would be appealing for investors who have a preference for stocks with lottery-like payoffs (that have subsequently delivered poor returns historically). Finally, they noted that specialised ETFs tend to have more exposure to small growth stocks that have high valuation multiples (notably the market-to-book, price-to-sales, and enterprise value-to-earnings before interest, taxes, depreciation and amortisation ratios) and higher short interest: “All these characteristics are associated with lower future returns.”

Investor takeaways

The evidence presented demonstrates that specialised ETFs at inception tend to own popular stocks about which investors are very enthusiastic (due to recency bias, resulting in performance chasing). Relative to broad-based portfolios, stocks in specialised ETFs experience greater media exposure with more positive sentiment. However, investor enthusiasm fades over time as performance deteriorates because sentiment has driven prices to excessive levels.

The above findings demonstrate that the ETF industry is great at capitalising on naïve retail investors’ preference for investment fads. In general, they are issued in response to the demand for trendy investment themes — the fund sponsors are responding to investor sentiment, which studies such as Global, Local, and Contagious Investor Sentiment, The Short of It: Investor Sentiment and Anomalies, Investor Sentiment and the Cross-Section of Stock Returns and Investor Sentiment: Predicting the Overvalued Stock Market have found to be a negative predictor of future returns. The high fees and cash flows into these poorly performing securities is just another example of retail investors behaving badly.

While broad-based and factor-based ETFs have brought investors the benefits of lower costs and greater tax efficiency, the specialised ETFs have created negative value — except for their sponsors, of course.

The evidence demonstrates that specialised ETFs, on average, do not create value for investors. In other words, popularity is a curse in investing, not a blessing. Investors are best served by having a well-thought-out investment plan and, like a stamp to a letter, adhere to it until they reach their destination. Forewarned is forearmed.

For informational and educational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. Certain information is based upon third party data which may become outdated or otherwise superseded without notice. Third party information is deemed to be reliable, however its accuracy and completeness cannot be guaranteed. By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party websites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them. The opinions expressed by featured authors are their own and may not accurately reflect those of the Buckingham Strategic Wealth® or Buckingham Strategic Partners®, collectively Buckingham Wealth Partners. Neither the Securities and Exchange Commission (SEC) nor any other federal or state agency have approved, determined the accuracy, or confirmed the accuracy of this article. LSR-22-2

LARRY SWEDROE is Chief Research Officer at Buckingham Strategic Wealth and the author of numerous books on investing.

ALSO BY LARRY SWEDROE

Disposition effect hampers active managers, study shows

Should investors fear rising public debt?

Climate alphas as predictors of future returns

Lifestyle funds: Do they add or subtract value?

New evidence on how investor emotions affect markets

© The Evidence-Based Investor MMXXII