Investing in bonds is about the last thing you feel inclined to do just now. After all, bonds are supposed to provide protection from stock market falls, and this year they have singularly failed to do that. As a result, cautious portfolios have been badly hit. But just because bonds have had a bad year, that doesn’t make them a bad investment. Giving up on them now would be like avoiding shares after the dotcom bust, or never buying a home after a property slump. This brilliant article first appeared on the Monevator website and is republished here with kind permission.

Across the Monevator comments and beyond, a cry has gone up: “Bonds are bad! Down with fixed income! Duration is for dummies! Stick your equity cushion where the sun don’t shine!”

It’s not hard to see where the hate comes from.

2022 has been a terrible year for bonds.

I don’t mean terrible ‘for bonds’ in the sense that bad years for bonds are less common than for shares, meaning you’re disappointed with, say, a minus 5% annual return.

It has not been a bad year for bonds like Oswald Mosley wasn’t that bad for a Nazi.

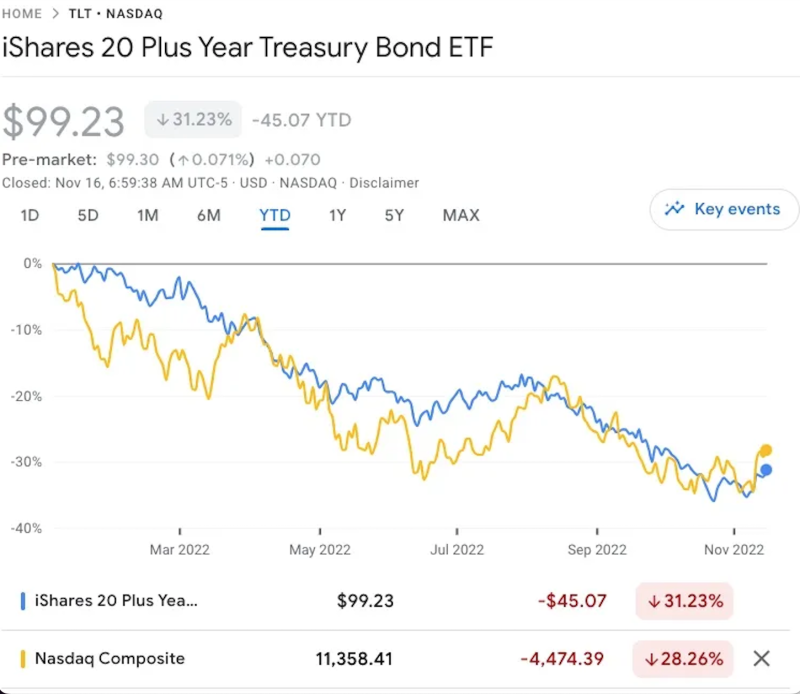

No, it’s been a bad year in the sense that some bonds and bond funds — those of lengthier duration — have done even worse than the risky US Nasdaq index – which itself has had a rotten year:

Clued-up investors know equity declines come with the territory. Fair enough.

However we own bonds mostly because we hope they’ll do better than shares when that happens.

That’s why 2022 stings so much. It’s not just that bonds have fallen a lot. It’s that they’ve fallen when shares are down too.

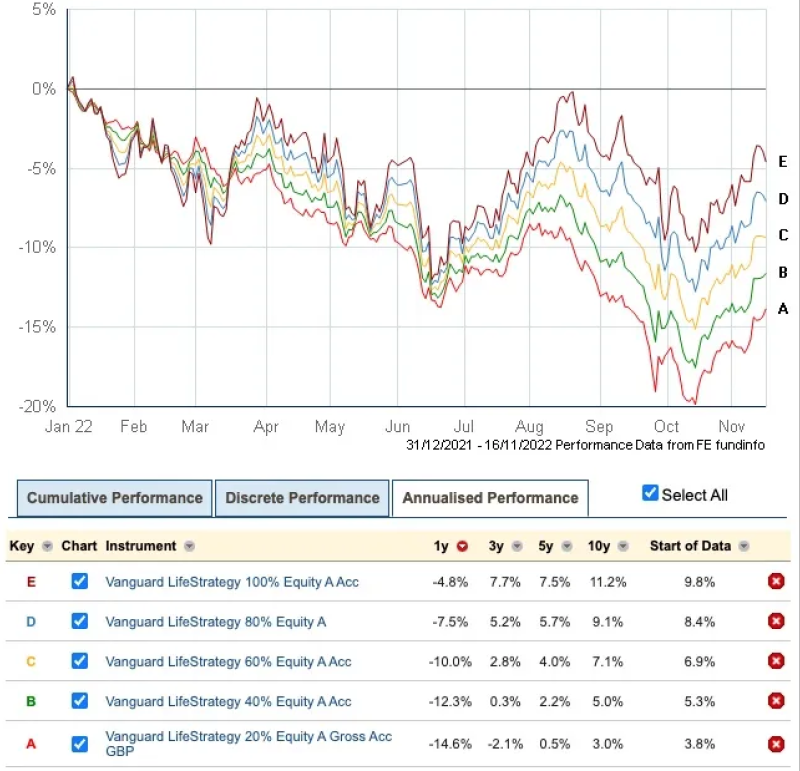

Bad for bonds is worse for LifeStrategy

Because long-duration bonds have done so much worse than shares — especially US shares, juiced by currency gains for UK investors — we see surprising and ghastly results like this:

The chart shows how Vanguard’s popular LifeStrategy funds have put in a Bizarro World performance this year.

- The supposedly lowest-risk LifeStrategy option — the 20/80 fund, with just 20% in shares and 80% in bonds — has done the worst.

- The best LifeStrategy fund to own in 2022 was 100% in shares.

This is the opposite of what we’ve come to expect from balanced funds like LifeStrategy.

And let’s be honest — it sucks.

It’s one thing to lose money in the hurly-burly of the stock market.

High risk, high reward, right?

It somehow feels far worse when your pension is battered by boring old bonds.

The trouble is the same unwelcome double act has done for both bonds and shares this year — high inflation and rising interest rates — with lofty starting valuations for both asset classes having a supporting role.

Hence in 2022 bonds and shares have moved down together.

So are the newly-converted bond-o-phobics right? Have bonds been unmasked as wolves in sheep’s clothing? Ripping your face off just when you could really use some comfy woollens?

Should we junk our bonds faster than Tories getting rid of a Prime Minister?

Not so fast.

Not such a bolt from the blue

The potential for bad years for bonds was always in the small print — and the history books.

Moreover the risk of a bad spell for bonds only rose as prices climbed and yields fell.

Of course, we human beings tend to think the opposite way. The longer something bad doesn’t happen, the more we dismiss the risk.

(This is also why every outdoor activity with children eventually ends in tears…)

And after a 40-year bull market for bonds – longer than many City careers – complacency was at an all-time high.

But the risks were still there, if you wanted to see them.

Way back in 2012 I explained how bonds looked more vulnerable as Central Banks lowered rates:

What makes bonds particularly risky at the moment is the low yields you get for holding them.

As we’ve seen, this increases duration, and so makes them much more vulnerable to interest rate shocks.

I held no government bonds myself, preferring cash. As I wrote then, gilts “gave me the willies”.

This was my stance for a decade. Seems a good call now — but the fact is until this year it was a losing trade to prefer cash over bonds for safety.

In my 2012 piece I also said I couldn’t imagine yields on a ten-year bond would go much lower than the prevailing 2%.

But they eventually went to near-zero, boosting returns for bond owners.

Moderation in all things (even bonds)

My co-blogger The Accumulator has also flagged the issue many times before this annus horribilis.

Like me in 2012, he also suggested holding more cash as one response to very low yields. But being the grown-up in the room, The Accumulator also urged readers not to dump bonds entirely.

Instead he stressed you could choose lower duration bonds to make your portfolio less vulnerable to an interest rate shock.

Why didn’t we bail on bonds?

What none of our articles did was declare in 72pt bold font:

SELL YOUR BONDS — NEXT YEAR WILL BE TERRIBLE

Indeed you’ll wait a long time to read an article like that on Monevator.

That’s not because we keep such secrets to ourselves. Rather it’s because we have no idea exactly when crashes of any kind will happen.

For The Accumulator, knowing your limits is a key plank of the passive way.

For me, a naughty active investor, it’s a perspective hard-won from years of trying to second-guess the market.

But this is not a cue for you to read a different website – let alone turn to TikTok – instead of sticking with us.

Because I don’t believe anyone can tell you exactly when to get in and out of markets, consistently.

Sure, you will find thousands of people making comically precise market predictions all over the Internet. Some of these people are quite popular. But that doesn’t mean they’re any good at it.

Everyone has a hunch now and then. And after a drink, I’ll tell you I think I do better than average.

For example here’s a bottom. And here’s a top.

I think I do okay, by the standards of a scurrilous game. But the fact is it’s hard to distinguish skill from luck – or more importantly to bank on it.

I don’t urge you to avoid making wholesale moves in and out of different asset classes (as opposed to judicious tweaks or re-balancing) not because I don’t trade my portfolio. But because I do.

Mugged by the market

Since 2010, some commentators — including me, as we’ve seen above — were saying bonds were over-priced and bound to crash when yields rose.

But as it turned out, bonds delivered solid returns for many years to come. Culminating in a final flourish in the 2020 Covid crash.

How many people held themselves — or their preferred pundits — accountable for getting those predictions of a bond crash wrong, year after year?

Of course you might argue it didn’t matter exactly when the bond crash happened. It’s been so deep you could have bailed on bonds in 2015, say, and still dodged a lot of pain.

True — but that statement is neck-deep in hindsight bias.

Once you’d sold your bonds, you had to put the money somewhere.

Maybe into low-to-zero yield cash?

It’s taken a crash of 2022 proportions for that bet to come good. There was no certainty it would.

Equities?

Sure, if you chose US or global equities then these have beaten bonds over the past decade.

But (a) you were and are always likely to get a higher return from equities than bonds, and (b) the risk is you don’t. Equities are far more volatile than bonds.

In some parallel universe, we saw a huge equity crash in 2016 that we’re only now limping out of. For the past six years in that alternate reality, even low-yield bonds did better than shares.

Or maybe there’s a universe where we’re still looking for a Covid vaccine, and the world is mired in a 1930s-style depression.

I don’t want to think about what our portfolios would look like in that reality. But I’m confident that bonds would be doing better than shares.

Investing: probably, likely, could, might, may, should

The trouble is we’re not good — as humans — in thinking about probabilities as a basket.

Something with a one in 50 chance of happening will happen, given enough throws of the dice.

Whereas people try to mentally transform risk like this:

Relatively lower risk = lower risk = low risk = no risk

That’s totally wrong. Bonds being relatively lower risk than shares never meant there was no risk.

It’s better to think of a diversified portfolio as a basket of relatively higher and lower risks, where something is definitely going to happen. But you don’t know what will happen in advance.

So 2022 should not be teaching you that bonds are bad, just because they’ve had a terrible year.

That would be like avoiding shares after the Dotcom bust of 2000, or never buying your own home after the early 1990s property crash.

The better lesson we should take from 2022 is very bad things can happen to our portfolios.

And that if a lot of things can happen, then some of them will.

This year it was bonds that blew up. But plenty of other historically rare but perfectly possible things are waiting to derail us in the future.

And in some of those situations, high-quality government bonds will be your best friends — especially now they have a meaningful yield again.

When you’ll be glad you chose to invest in bonds

Here are a few plausible scenarios where you’d probably be glad you kept some bonds:

Deflation – Strictly a regime of falling prices, deflation tends to be associated with higher unemployment, lower economic growth, stagnant or falling wages, and weak or negative stock market returns. But the best paper assets — government bonds and cash — can hold their value as the rest of your portfolio tanks. If yields fall then bonds can give you a capital gain to offset losses elsewhere. Whereas cash is likely to be yielding nothing.

A big and prolonged equity market crash — I’m not talking about a wobble like late 2018 or early 2020. Even 2022 hasn’t been particularly painful compared to the worst stock market crashes of all-time. Rather, imagine if your shares drop 70% and stay down for years. Bonds will probably do much better, at least in nominal terms. (However some very bad bear markets for shares coincided with big inflation-adjusted declines for bonds. You’ve been warned!)

A short sharp meltdown – Think the Global Financial Crisis or another deadly pandemic. This overlaps a bit with the previous entry. But the distinction is that a meltdown or confidence ‘flash crash’ is short-lived. Bonds may give you speedy gains upfront. You can then re-balance into rebuilding your battered equity exposure for the long-term.

You’ve retired — If you quit work to live off a 20/80 portfolio, pregnant with bonds, I excuse you a hollow laugh. 2022 has been awful. But over longer spans of time, bond returns are much less volatile than shares. When you’ve no new money coming into your portfolio and less time to sit out the declines, that’s valuable.

So yes, the long-awaited bond crash has finally happened. But we’re probably through the worst. If anything, it’s less likely to happen again anytime soon. At least not to the same awful extent.

One very bad year doesn’t entirely destroy the logic of owning some bonds, no more than the sinking of the Titanic killed the need for global travel.

Better days ahead for bonds

As we’ve explained before, falling bond prices have a silver lining. When bond prices fall, yields rise. And that bodes well for future returns.

As of early October, Vanguard’s models suggested that between 30 June 2021 and 30 June 2022:

… projected 10-year annualised returns for UK aggregate bonds have risen from 0.6%-1.6% to 2.4%-3.4%, while return expectations for global bonds ex-UK (hedged) have increased from 0.5%-1.5% to 2.3%-3.3%.

Again, low returns had been baked-in. Now they look a lot better.

On a related note, the fund behemoth has also modelled how future expected returns from a 60/40 portfolio improved from the end of 2021 compared to late September 2022:

According to the latest forecasts from the Vanguard Capital Markets Model, the projected 10-year average annualised return for a 60/40 portfolio has increased considerably since the start of the year, from 3.3% to 6.8% — a rise of 350 basis points.

I will triple underline these are expected returns. They are not guarantees!

However the mathematics of fixed interest means that models can be more confident about future returns from bonds, compared to shares.

And those future returns look brighter.

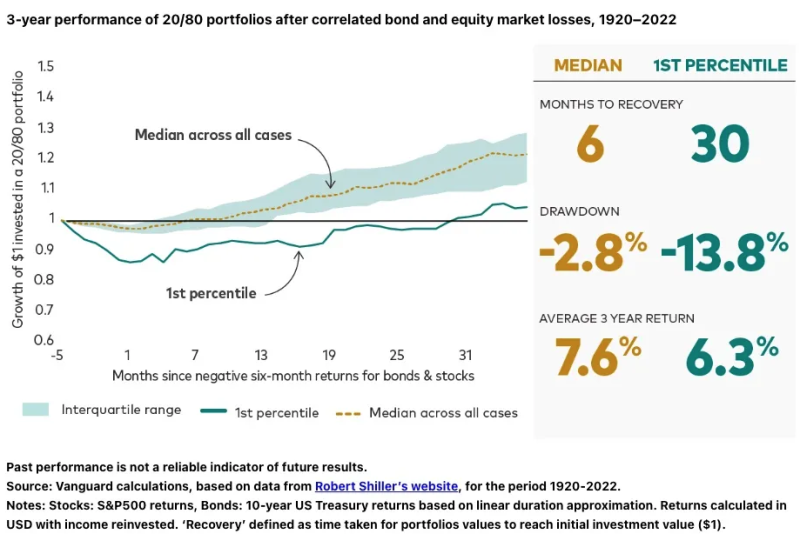

If history is any guide it probably won’t be too long before even the battered 20/80 LifeStrategy fund is back in the black:

Again, you can’t be certain with a forecast. But at the least it shows you why I’m so wary of all the pessimism about bonds right now.

If anything, I’d be buying them. (In fact I am).

Bonds are not bad, but prices can be

I would be a hypocrite if I said you should always own bonds. I didn’t invest in bonds for a decade and perhaps in the future I’ll be out of them again.

But equally I’m not a supposedly passive investor now bailing on bonds after a very bad year.

If that’s you, then ask yourself:

- What do you know better than the multi-trillion dollar bond market?

- If the answer is ‘nothing’, then aren’t you just responding emotionally to recent losses?

This isn’t a call to excessively load up on long-duration bonds. Interest rates could go still higher. If they do then after a recent mini-recovery, bonds could decline once more.

There’s even an argument that bonds tend to move in long secular cycles. If that’s the case then we might be in for decades of rising yields and mediocre returns.

It’s also perfectly possible for bonds and equities to both keep doing badly for years – especially in real terms.

Again, no guarantees.

But let’s learn the right lessons from 2022. By all means diversify your lower-risk assets with cash and gold. Stick to intermediate or lower-duration bonds if you’re concerned about interest rate risk.

Or even be a naughty active investor like me. Own what you like, but be ready to sell on a whim!

(Just know you’ll probably do far worse for trying, and you’ll definitely be more stressed.)

But you should probably own some bonds

Frankly, if you’re someone who now thinks bonds are bad — full stop — then you’re probably the sort of person who most needs bonds in their portfolio.

Ideally tucked inside an all-in-one fund where you can’t see how the sausage is made. Because something is always doing badly in a well-diversified portfolio.

I don’t mean this unkindly. The opposite. I know it’s been a rotten year.

However I’m worried some people are going to load up on equities, only to sell out at the bottom when the next deep stock market crash comes and they have no safety cushion at all.

Shares are riskier than bonds. Not this year, but most years.

And there are pros and cons for every asset class.

You think bonds are bad? That’s a shame, because they haven’t looked this good for ages.

Never say never again.

PREVIOUSLY ON TEBI

Eight takeaways from 20 years of SPIVA

Put options: Do they actually achieve anything?

Is the growth of passive investing messing with markets?

Active money management is like a love song

Understanding volatility and risk

PLEASE NOTE: The value of investments can go down in value as well as up, so you could get back less than you invest. It is therefore important that you understand the risks. This article, as with all of our content, is for general financial education purposes only and does not constitute personal advice based on your circumstances. If you are unsure about the suitability of a particular investment or course of action, we strongly recommend that you speak to a suitable professional adviser.

© The Evidence-Based Investor MMXXII