Most indexers choose the S&P 500 when seeking exposure to US equities. But is it possible to track the Dow Jones Industrial Average, the oldest and (at least outside the US) most famous American index? And if you could, is there a case for doing so? TIM EDWARDS, Managing Director, Index Investment Strategy, at S&P Dow Jones Indices, takes a closer look.

The growth of index funds has, in the main, helped to lower the costs and improve the performance of the average investor’s portfolio. Now, some are seeking to improve upon even the relatively low costs of conventional index funds via so-called “direct indexing”, by which investors purchase securities to match an index themselves, dis-intermediating the middlemen entirely. In fact, directly constructing a market-tracking portfolio might be easier than you think, and the concept is almost certainly much older than you realise.

Spoiler alert: this is really a post about replicating the 125-year old Dow Jones Industrial Average near-perfectly, with a little more than $5,000. But, first, let’s consider replicating three possible benchmarks for U.S. equities, ordered by their increasing breadth: the S&P 500, the S&P Composite 1500, and the S&P U.S. Total Market Index (TMI).

In practice, an investment manager tracking any of these indices — particularly the S&P TMI — will likely only approximate the index’s holdings. Indeed, doing so while still delivering benchmark-like returns is one of the central skills of passive portfolio management. To illustrate, consider just two conditions that might be applied:

1. If a security is in the index, we must hold a non-zero position in that security.

2. Each position must consist of a whole number of shares.

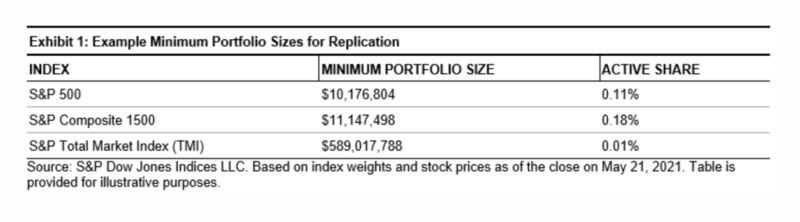

Conditions 1 and 2 effectively set a minimum size on the portfolio: if we need 1% weight in a stock priced at $100, for example, we need a portfolio of a least $10,000 (equal to the price, divided by the weight). Ranging across all constituents, the largest price-to-weight ratio gives us an indication of how large a portfolio must be to replicate the index fully. Based on this simple calculation, Exhibit 1 displays the minimum portfolio size to replicate each index, assuming that the stock with the highest ratio of price-to-weight has an allocation of exactly one share, and every other constituent is allocated the whole number of shares closest to the target weight. We also report the active share of the resulting portfolio versus its benchmark.

In this simplified estimation, around $10 million would seem a reasonable starting point for an index-tracking portfolio for the S&P 500 or the S&P Composite 1500. For the S&P TMI, considerably more might be needed.

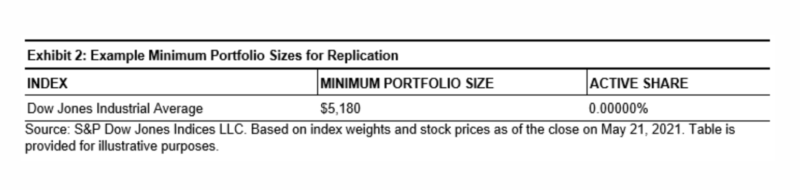

But what about the Dow Jones Industrial Average? By construction, the index comprises a representative set of 30 names designed to reflect the overall U.S. market, so we already start with a handily modest number of positions. And it has another helpful property: because the DJIA is price-weighted, the ratio of price-to-weight is the same for every stock!

In other words, there is a simple way to build a portfolio that meets conditions 1 and 2: buy exactly one share in each constituent. That would (as of May 21, 2021) require a grand total of only $5,180. And even better, ignoring any trading costs or rebalances, this portfolio will, by definition, exactly match the performance of the benchmark.

“Direct indexing”, perhaps using fractional shares and perhaps also employing the full capabilities of an expert portfolio manager, is an exciting new frontier in passive investing. But as the venerable Dow approaches its 125th anniversary, it may still have a role to play at the frontiers in making disciplined, diversified investing available at a lower cost for everyone.

This article was first published on the Indexology blog.

MORE FROM S&PDJI

For more valuable insights from our friends at S&P Dow Jones Indices, you might like to read these other recent articles:

A diverse portfolio is a strong portfolio

Why even Buffett has been buffeted by the index

The case for looking beyond the S&P 500

The impact of style bias on the latest SPIVA data

Three reasons for active managers to feel positive

What does GameStop mean for market efficiency?

PREVIOUSLY ON TEBI

The all-important pension question

Advising on life’s big changes

How to avoid foolish behaviour

Taking on the dependency problem

The endowment effect and difficult decisions

A diverse portfolio is a strong portfolio

OUR STRATEGIC PARTNERS

Content such as this would not be possible without the support of our strategic partners, to whom we are very grateful.

TEBI’s principal partner is Sparrows Capital, which manages assets for family offices and institutions and also provides model portfolios to advice firms. We also have a strategic partner in Ireland — PFP Financial Services, a financial planning firm in Dublin.

We are currently seeking partnerships in North America and Australasia with firms that share our evidence-based and client-focused philosophy. If you’re interested in finding out more, do get in touch.

Image: Aditya Vyas via Unsplash

© The Evidence-Based Investor MMXXI

Robin is a journalist and campaigner for positive change in global investing. He runs Regis Media, a niche provider of content marketing for financial advice firms with an evidence-based investment philosophy. He also works as a consultant to other disruptive firms in the investing sector.