By PRESTON McSWAIN, from Fiduciary Wealth Partners

We think most anyone would agree that you can’t compare apples to oranges.

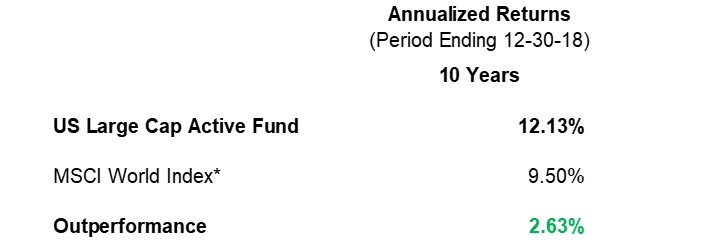

We also think most people in the investment world would agree that the following comparison would be a chart crime.

It would allow a salesperson for this U.S. large cap fund to boast that they had outperformed by over 2.5% per year net of all fees for 10 years.

The chart crime would be that the salesperson would be making an apples to oranges comparison of a U.S. large cap fund to an index that was made up of stocks from around the world.

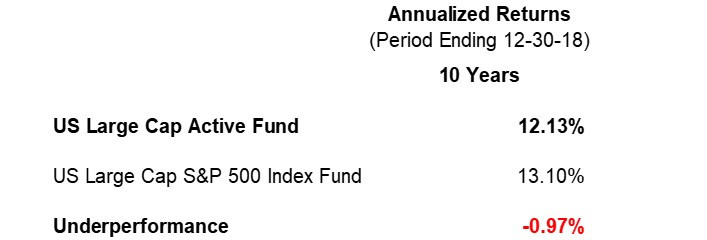

Below is how the same fund performed against a more comparable U.S. large cap S&P 500 index fund.

When comparing apples to apples, the fund didn’t outperform.

It underperformed a peer group index fund alternative by approximately 1% per year for 10 years.

Financial Twitter would likely be in an uproar over the apples to oranges illustration and regulators might also come calling related to the fund’s sales materials.

Why then do charts like the following circulate freely with little push back?

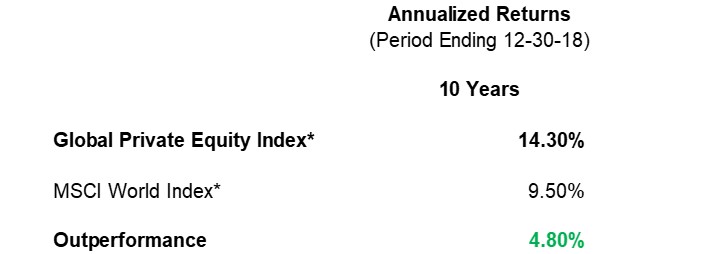

* The MSCI World index illustrations present the performance of the MSCI ACWI Index. Global Private Equity index performance represents the Cambridge Associates Buyout and Growth Equity Index

This “outperformance” illustration is a recreation of a chart from a private investment sales presentation that we recently received from a wealth manager.

It is impressive, and could create lines like the following, which is similar to a quote we heard not long ago:

“We have been able to deliver outperformance consistently, and on average across all years, we have provided 4.8% of annualised outperformance.”

What’s the problem?

The following summary of LinkedIn and Twitter posts from a top Private Equity (PE) researcher from the University of Oxford, Ludovic Phalippou, might say it the best:

“The same people who said that it was normal to compare Private Equity to the S&P 500, even though it was not comparable… [now say] that we should not use the S&P 500.

“[They] now advocate the MSCI world index, [which is one of] the worst performing indexes over the last ten years and… has even less to do with PE.

“Most PE is U.S. small and mid-cap..”

The MSCI World index used in the previous comparison is not predominately U.S. small and mid-cap.

In writing this we could touch again Ludovic and many others have warned that PE can be calculated and presented using an internal rate of return (IRR) methodology that can make direct comparisons to public market indices “IRRelevant” or “dangerous.”

Fund managers, investment publications and index providers should know this, however.

When the indices are published each quarter, they have this disclosure at the bottom of the page.

“Due to the fundamental differences between [how private equity and public market returns are calculated], direct comparison . . . is not recommended.”

This always makes us ask why they continue to be widely distributed in a direct comparison form every quarter, but alas, no answers yet.

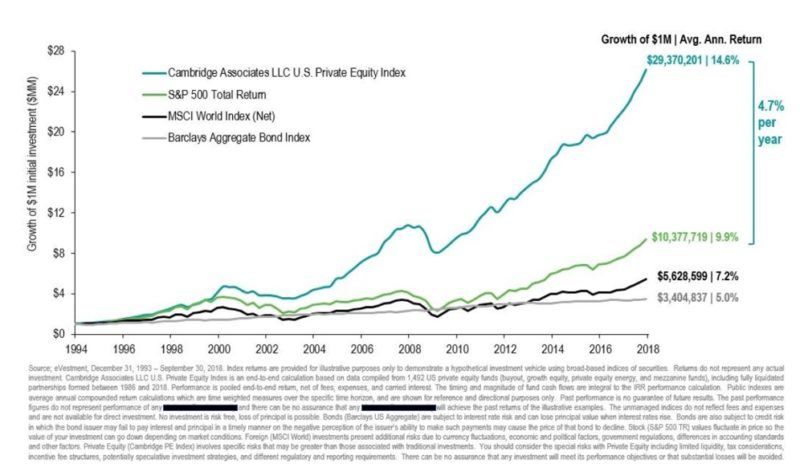

As an example of this, below is another chart we recently received from another investment adviser that was promoting their “fiduciary” approach to PE fund selection.

This firm did show the S&P 500 in addition to the MSCI World Index, and warned in small print that the “timing and magnitude of cash flows are integral” to the PE performance calculation.

I wonder, though…

Why didn’t this adviser include the “direct comparison… is not recommended” disclosure language that the index provider they used included in their direct comparisons?

New proposals to expand access to these types of presentations then bring me to this question:

How many investors will be able to apply the “complex multi-dimensional analysis” required to evaluate how the timing of cash flows can distort and often inflate PE returns as compared to returns investors have actually received?

Finally, should this “fiduciary” also disclose how lines of credit used by many PE firms might now be inflating these comparative returns that are “not recommended” even more – to the tune of 3-7% per year, depending on the age of the fund?

Looking back to the PE performance comparison chart…

If credit lines have been inflating what might be artificially high pooled IRRs by an additional 3-7%, has PE really outperformed more comparable U.S. small cap public equity index funds?

In a paper published in November 2019, researchers wrote that when PE is compared to U.S. small cap stock funds, “excess performance disappears” and is close “across all vintage years.”

Before some might think we are anti-PE, keep in mind that we write something like this each time we publish something on private equity.

We do not feel that private investing is bad or should not be part of investment allocations.

Many private investments are good and many good private equity managers exist.

On behalf of clients, we also have relatively large sums invested in private equity.

Non-apples to apples presentations, however, do no one any good.

They can make the industry look bad and could be setting false expectations, which might be driving long-term commitments into investments that are illiquid (limited to no liquidity = limited to no options for change).

For the good of all in the investment community (managers, consultants and investors) we hope comparisons like this will change or simply stop.

In the meantime, when you see PE return presentations, review all disclosures and ask questions to make sure benchmark comparisons are reasonable.

If presentations don’t have simple plain language disclosures, have little to no disclosures, or have notes stating that index comparisons are “not recommended,” check carefully.

Some of the apples you are being asked to compare and consume might be rotten.

PRESTON McSWAIN is a Managing Partner and Chief Investment Officer of Fiduciary Wealth Partners. Based in Boston, Massachusetts, FWP is an evidence-based financial planning firm that aims to provide transparency, simplicity and peace of mind for high-net-worth individuals.

Related articles:

Lies, damned lies, and private equity returns

Lies, damned lies, and private equity performance