Robin writes:

Many years ago, at an investment conference at a prestigious Oxbridge college I sat next to the college bursar at dinner. The conversation inevitably turned to plans for managing the college’s endowment fund. I was too embarrassed to say anything — perhaps I should have done? — but it soon became apparent that the strategy was not in the least bit evidence-based.

It surprised me at the time, but it no longer would today. That’s because, in my experience, it’s not unusual for very clever people to struggle with investing. In many ways the sharpest minds are particularly predisposed to making flawed decisions.

SAM INSTONE sees this phenomenon all the time. Sam is the CEO of AES International, an evidence-based financial planning firm in Dubai which typically serves high-flying expats working in law, banking and management consulting. As Sam explains, the best investors aren’t those with the highest IQs or who’ve read the most books; it isn’t knowledge, but SELF-knowledge, that really sets them apart.

The law library at King’s College London was always quiet. Full of the brightest, hardest working and most driven individuals. (Different to the humanities and social sciences one where I was based!)

Law is a thinking profession and the Myers-Briggs personality types prevalent among international lawyers make fascinating reading. Statistically, thinking roles are most often done by introverts and the intellectual ferocity associated with high-performing lawyers would lead me to expect them to think their way to success.

But the evidence shows a starkly different picture.

Stressful work

Law is a highly stressful career. There’s the fear of missing billable targets, career track fears and often challenging colleagues to navigate.

Fear of failure, career fouling and lack of support to name just a few of the anxieties. Time pressure, balancing conflicting priorities and transitioning from being employed to self-employed. But, we’re all human.

We all succumb to all manner of cognitive traps. And lawyers are not exempt because of their high intelligence.

The lack of time, pressures of work, lifestyle choices, profit distribution mechanisms and the lack of space for slow, system-two thinking mean AES typically sees more compounded planning mistakes by international lawyers than any other profession we serve.

It shouldn’t come as a surprise that all successful investing is goal-focused and planning driven. All failed investing is market-focused and current outlook driven.

All successful investors act continuously on their plan. Failed investors react continually to the markets and normally in the wrong way.

It is not possible to react your way to investment success… Particularly if you haven’t got the time to document an actual plan.

Unique financial situation

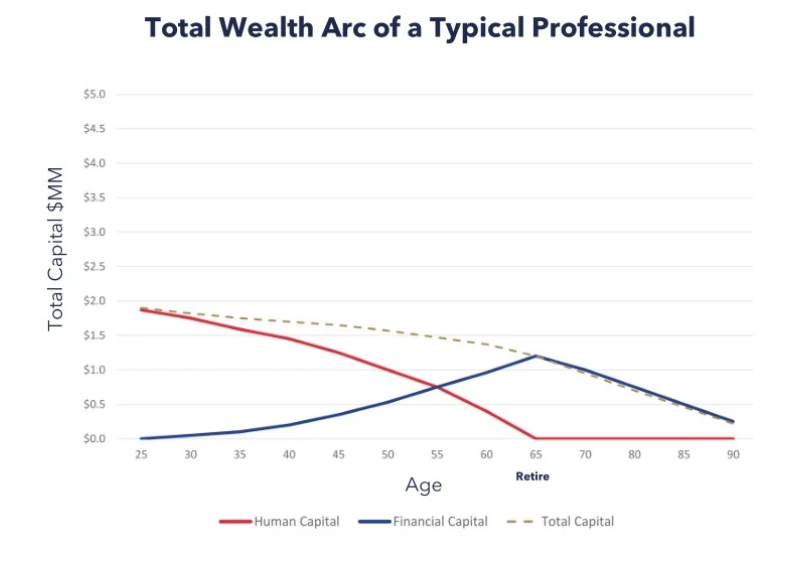

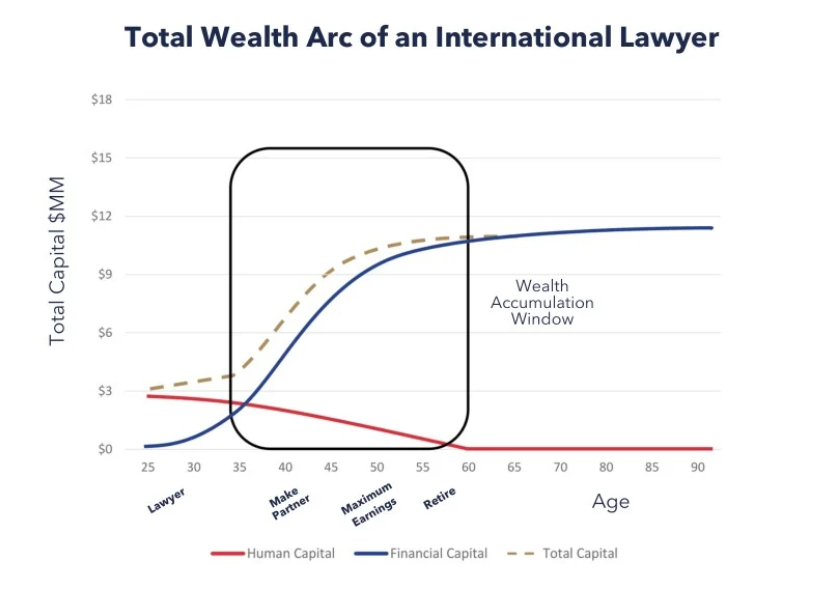

International lawyers have a unique financial situation. Many wish to earn high so they can retire early before they burn out.

The partnership structure, benefits, tax-related obligations, family responsibilities and a unique “wealth accumulation window” mean highly specific planning requirements exist.

Accelerated income-earning potential combined with the relatively short time period in which it will be earned, creates a rare saving window that doesn’t exist in other typical career paths.

Rapidly increasing gross compensation means international lawyers are likely saving more absolute dollars than ever before.

It’s therefore easy to become complacent, determine you are “probably saving enough” and leave it at that.

Destructive thinking

This way of thinking, however, can be destructive. Often, partners think they are saving enough but countless financial complexities exist within a professional services career track.

Biases or mental errors are some of the biggest things standing in the way of your financial success. That’s because they’re not easy to recognise in ourselves.

Here are some of the most common mental errors affecting lawyers’ decision-making – rainmaker, litigator, corporate lawyer or otherwise.

#1. The Dunning-Kruger effect

I’ve talked about this before. People tend to overestimate their own competency. This leads to overconfidence and underestimating the limits of their own understanding. You’ve heard it said, “a little learning is a dangerous thing”.

From an investor’s perspective, it often causes people to think they’re Warren Buffett when they’re not. They’re actually the people in this Dalbar study.

Ferociously intelligent people are irrational and hardwired to make sub-optimal decisions in areas outside their expertise. Not everybody can be above average, at least not all the time.

#2. Loss aversion

Investors are more sensitive to the pain of loss than they are to an equivalent gain. They feel a loss of 10% more than a gain of 10%.

Fear takes over, even after small losses, and distorts the decision-making process. Emotions can overpower intellect. This, in turn, causes investors to not take enough risk.

We see this all the time. People who have vast cash holdings with little or no exposure to stocks. This can add years of extra work to a lawyer’s ideal retirement age.

Obviously, that plan is a long-term loser. Playing it safe never yields real success.

#3. The endowment effect

People tend to overvalue the things they own. In particular their houses. Investors also find it hard to sell securities they own, even when the financials are deteriorating fast.

A good financial planner can help remind you: the security doesn’t know you own it. It’s not going to have its feelings hurt if you sell that stock and buy a better one.

#4. Anchoring

It’s difficult to admit our own historic mistakes. People get irrationally fixated on what they paid for something — regardless of what’s happening in the actual market.

We see it all the time. They don’t want to sell until they break even. Sometimes that doesn’t happen for decades. The Nikkei is still below where it was in 1991.

I’m not a fan of market timing but there is a time to move.

#5. Recency bias

People tend to overestimate the significance of recent events and irrationally discount longer-term trends. Those of us over a certain age remember Black Monday on October 19th, 1987. The stock market lost a quarter of its value in a single day. That spooked a lot of people – and many got out of the market right after.

Looking back at it now, Black Monday barely registers as a blip on the graph.

This is an example of recency bias. Recent losses play havoc on our emotions and cause us to lose perspective.

The long-term trend of the stock market makes any single day’s volatility look insignificant in comparison. So much so, that when we look back at a single day like Black Monday on a chart, we wonder how we could have panicked.

Keep your eyes on the prize.

#6. Status quo bias

Objects at rest tend to remain at rest. People are naturally resistant to change. It’s tough for them to pay small costs even for big gains.

A status quo bias minimises the risks associated with change. It’s easier to sit tight and do nothing even though the compounded impact of nothing might cost them millions in retirement.

It’s hard for the unaided human brain to picture “the future”, because evolution designed us to survive today.

However, this causes people to miss out on potential benefits that might even outweigh the risks.

#7. Failure to rebalance

This is closely related to status quo bias and recency bias. People are reluctant to take action to rebalance a portfolio.

It’s too much fun to let winners run. It’s also psychologically difficult to sell winners to buy losers.

But failure to rebalance quickly causes the client to be dangerously exposed to a downward turn in the markets.

The remedy? Remember that investing is all about buying low and selling high, while managing risk.

Rebalancing periodically takes care of all three imperatives.

#8. Neglecting taxes

Changing tax regimes lurk to catch international investors.

As an expat, my own UK property investments are now devoured by taxes. Better options simply exist elsewhere.

But where? Many investments domiciled in high-tax jurisdictions have hidden taxes.

Avoiding termites eating your future returns can be challenging and good planning is about finding the best after-tax returns possible.

#9. Watching too much TV

Many people spend way too much time watching investing shows on TV and reading the financial news. They should stop.

The financial media is constantly buzzing about the news – which creates massive recency bias.

It plays on your emotions and causes you to move with the mob instead of against it.

#10. Confusing historical returns with future expectations

Just because stock A has generated 15% returns per year for the last ten years doesn’t mean it will continue doing so.

In fact, the more stocks go up, the more cautious we should be.

#11. Abandoning the plan

Too many people encounter a short-term setback and then abandon the plan they carefully set up.

They get caught up in recency bias and lose sight of the bigger picture.

Think of it this way. You set off to drive from London to Edinburgh, but you run into a traffic jam in the first five miles.

Cyclists start passing you. Are you going to sell your car and take a bike? No.

You’re going to be patient and stick with your plan.

Because you know traffic jams are a normal part of driving and they won’t last long. You’ll soon be on the open road making progress towards your goal.

No matter how bad events seem, the market still grows in the long run.

#12. Ego

High-earning professionals are cannon fodder for private banks and investment brokers with posh-sounding names.

But it’s nice to feel important and be approached. Perhaps it helps us feel like we’ve “made it”.

These businesses aren’t interested in creating a plan and helping you stick with it. They’re interested in flogging you an in-house investment portfolio stashed full of hidden costs which no doubt performs poorly.

Even senior professionals (with under £10 million to invest) don’t get the same service as high net worth business owners and entrepreneurs. So, it’s likely you get a cookie-cutter approach which a logical, academic, independent analysis would utterly destroy.

It’s strange so many professionals value professional independence and fiduciary duties but fail to apply the same rigour when taking advice on their own finances.

That complimentary invitation to the prestigious sporting event simply isn’t worth the years of extra work required after the private banker has been paid for offloading all his products onto you.

What can be done?

Human nature is always and everywhere a failed investor.

The ability to create and document a robust lifetime investment plan — and the faith, patience and discipline to keep you from blowing up that plan at some fleeting moment — is not available to the unaided human mind.

Understanding the ferocious intellectual power of lawyers, I’d expect many to read around the subject and formulate their viewpoint.

But the question is…

Can you really become a smarter investor just by reading all these books, blogs and other resources out there?

Is there something else you need to become more educated and smarter as an investor?

J. Krishnamurti, one of the greatest teachers India has produced, writes this in his landmark book, Education and the Significance of Life:

“The ignorant man is not the unlearned, but he who does not know himself, and the learned man is stupid when he relies on books, on knowledge and on authority to give him understanding.

“Understanding comes only through self-knowledge, which is awareness of one’s total psychological process.

“Thus education, in the true sense, is the understanding of oneself, for it is within each one of us that the whole of existence is gathered. What we now call education is a matter of accumulating information and knowledge from books, which anyone can do who can read. Such education offers a subtle form of escape from ourselves and, like all escapes, it inevitably creates increasing misery.”

Krishnamurti’s thoughts, and what I have experienced myself, show that self-awareness or “knowledge about self” is the best education one can ever get.

“Self-knowledge is not a thing to be bought in books, nor is it the outcome of a long painful practice and discipline; but it is awareness, from moment to moment”.

I believe the right kind of investment education comes with the transformation of ourselves. This entirely depends on our awareness about our behaviour, risk-taking capacities, and habits.

When we are aware of ourselves, we are in a better position to behave well. And make good decisions about whether or not we have the time, expertise and inclination to plan our ideal financial futures.

A planner can’t help you accumulate wealth in the way you have as a result of your professional hard work, achievements and success.

But they can help you preserve and gradually grow the accumulated wealth you have and give you the clarity, confidence and control to get and keep the future you want.

This is where the inestimable value of an intelligent and empathetic professional planner can make all the difference to that wealth arc and perhaps save many a lawyer those years of extra work.

This article was first published on the AES blog and is republished here with permission.

Also by Sam Instone:

Avoiding mistakes with your finances

Here are some recent TEBI posts you may have missed which we think you’ll find interesting:

Is Vanguard the Tom Hanks of asset management?

Market timers are fooling themselves

Stop admiring your successful trades

Three truths about ESG investing

Hedge fund fees are much worse than you thought

Should you invest with Baillie Gifford?

Is there such a thing as a “normal” stock market?

Active or passive — which is more volatile?

Can we help you find a financial adviser?

The evidence is clear that you are far more likely to achieve your financial goals if you use an adviser and have a financial plan.

That’s why we’re trialling a new service called Find an Adviser.

Wherever they are in the world, we will put TEBI readers in contact with an adviser in their area (or at least in their country) whom we know personally, who shares our evidence-based investment philosophy and who we feel is best able to help them. If we don’t know of anyone suitable we will say.

We’re charging advisers a small fee for each successful referral, which will help to fund future content.

For compliance reasons, this service is currently unavailable to readers in the US.

Need help? Click here.

Picture: Hunters Race via Unsplash