Financial downturns are unpleasant for just about everyone. As this article from DIMENSIONAL FUND ADVISORS explains, it’s at times like these that investors should remember the basic principles of investing their adviser taught them when they started working with them.

A famous American football coach once said, “You don’t rise to the occasion, you sink to the level of your training.” The implication is that, in times of great stress, the most reliable recipe for success is sticking to a set of fundamental principles.

From February 20 to March 20, the S&P 500 Index returned –37.4%, with daily returns ranging from –12.0% to +9.4%. A drop of nearly 40% in the stock market combined with a spike in volatility can make many investors reconsider their investment approach.

Some might suddenly find stock-picking approaches more alluring. After all, who has not heard the claim that a volatile market is precisely the environment in which many traditional active managers thrive? But is there any truth to this claim?

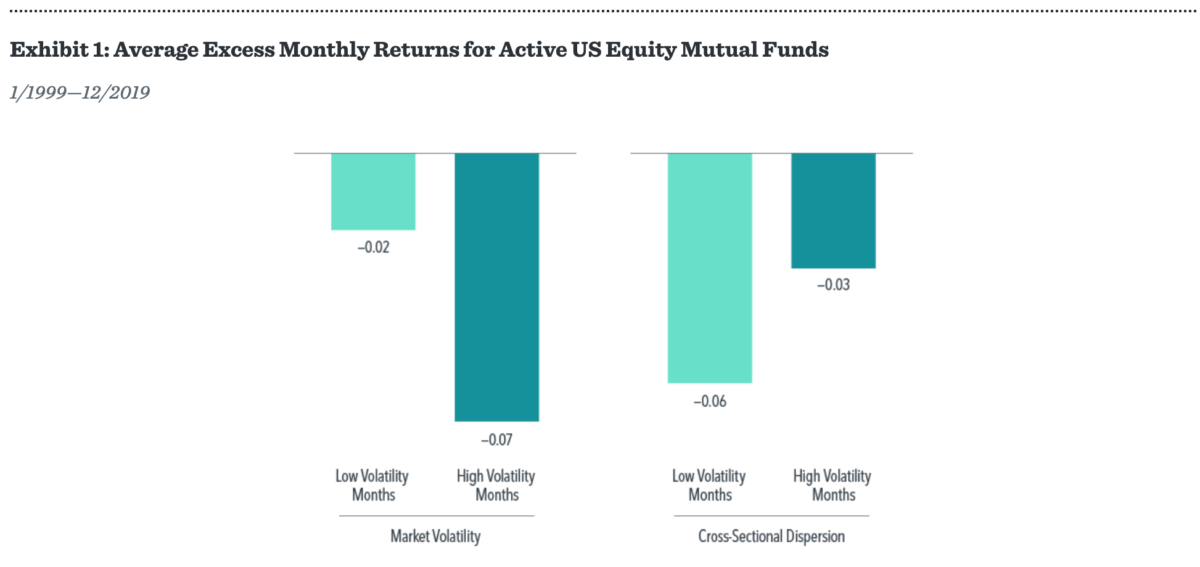

To explore this issue, we looked at the performance of active US mutual fund managers over the past two decades. We considered two different ways of measuring stock market stress: market volatility (or how much stocks rise or fall in a given month) and return dispersion (or the range of returns across all US stocks). In each case, active managers underperformed their index benchmarks.

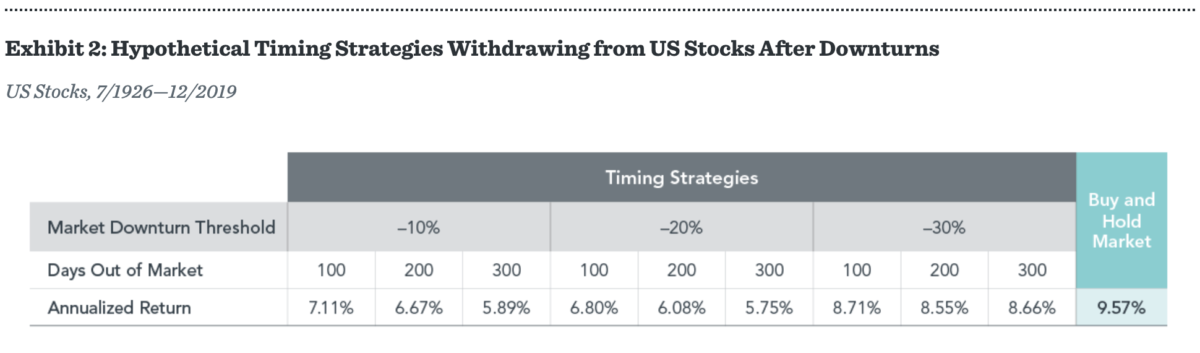

Another way some investors might react to a falling market is by jumping ship and selling out of stocks. The intuition may be that sitting out of the market for a period of time can help avoid further losses. However, the data suggest this type of market timing may instead reduce investors’ gains over time.

Exhibit 2 illustrates this point using hypothetical timing strategies that switch from US stocks into US Treasury bills after market downturns of various magnitude and switch back to US stocks following different lengths of time out of the market. Compared to the market’s long-term annualized return of 9.57%, nearly all of the timing strategies underperform the simple buy-and-hold strategy.

Should these results be surprising? One of the challenges with trying to outguess markets is the unpredictable nature of outcomes. For example, how many pundits would have expected the equity market in China, ground zero for the COVID-19 outbreak, to outpace global equities by over 10% year to date, as of March 31?

Financial downturns are unpleasant for all market participants. Investors can reduce exacerbating the experience by adhering to core principles. Two such principles supported by a long history of research are broad diversification and maintaining a consistent asset allocation. Investors who deviate from these principles by pursuing stock picking or market timing may undermine their ability to achieve their investment goals.

GLOSSARY

Return Volatility: A statistical measure of the variability of returns for a given security or portfolio. Volatility is often measured using standard deviation.

Cross-Sectional Return Dispersion: A statistical measure of the variability of individual stocks’ returns.

Standard Deviation: A measure of the variation of a set of data points. Standard deviations are often used to quantify the historical return volatility of a security or portfolio.

Market Downturn Threshold: Magnitude of the US stock market’s decline used to determine when to switch from US stocks to US Treasury bills.

Days Out of Market: Number of days during which the hypothetical strategy is invested in US Treasury bills instead of US stocks.

Fama/French Total US Market Research Index: The value-weighed US market index is constructed every month, using all issues listed on the NYSE, AMEX, or Nasdaq with available outstanding shares and valid prices for that month and the month before. Exclusions: American Depositary Receipts. Sources: CRSP for value-weighted US market return. Rebalancing: Monthly. Dividends: Reinvested in the paying company until the portfolio is rebalanced.

This article first appeared on the Dimensional Fund Advisors blog, Dimensional Perspectives.

Interested in more insights from Dimensional? Here are some more articles from this series:

Study provides fresh insight on bond returns

The outsize rewards for owning the top-performing stocks

You can’t predict market movements: 2019 is a case in point

DFA’s new investment factor explained

Has value really lost its vigour?

Booth & Fama: a friendship that changed investing