Robin writes:

I originally wrote this article for the Suitable Advice Institute and would like to acknowledge the input into it from Paul Resnik, the SAI’s founder. Paul is undoubtedly one of the industry’s good guys, and consumers in the UK and Australia, and indeed around the world, owe him a huge debt of gratitude.

I had an interesting response to one of my recent posts from a financial adviser in Italy. “I wish journalists wrote articles like this in my country,” he wrote. “Our financial industry is never seriously questioned.”

It set me thinking. Compared with some countries, Britain must seem like a consumer champion when it comes to investing and financial advice, a beacon of fairness and transparency. But the reality is very different. I’m constantly frustrated at the glacial pace of positive change here, and the fact our feeble regulator, the FCA, seems permanently wrapped around the industry’s little finger.

It’s a similar story across the Atlantic. Yes, the US has the lowest fund fees in the world, and a growing number of advisers there are embracing fairer fees and value propositions based on proper financial planning rather than selling products. Yet the fund industry continues to use its financial and political muscle to retain its colossal profits and its dominant position in American life.

The power of Bay Street, Canada’s Wall Street equivalent, is arguably even more entrenched, thanks to some of the world’s highest fund fees and consumers who seem far too meek to question why they should carry on paying them.

So what about Australia? How does it compare with other English-speaking countries on the sorts of issues that we at the Suitable Advice Institute are interested in?

Credit where it’s due

On the face of it, Australia appears to be doing not badly. Every year the Mercer CFA Institute Global Pension Index compares retirement income systems in 39 countries. The most recent index placed Australia third, immediately ahead of Israel, but behind the Netherlands and Denmark. That puts it well ahead of Canada in 9th place, the UK in 11th and the US in 16th.

Australia also has the fourth largest private pension pool in the world, at A$3 trillion — not bad for a country of just 25 million people.

Now there are plans to cement Australia’s reputation as a world leader for retirement provision by increasing the amount that employers pay into “superannuation”, or super for short, a defined-contribution savings scheme introduced in 1992 by the then Labor government. These payments, currently set at 9.5% of the employee’s income, paid by the employer, are due to rise to 12% in half percentage point increments by 2025.

But before you start getting jealous and planning a new life Down Under, beware: there is definitely another side to the story.

Second thoughts

Many Australian governments have ‘reformed’ retirement savings — but the endless fiddling has meant that superannuation has become intensely political.

The current conservative government has been having second thoughts about increasing employers’ super contributions — increases that were legislated in 2011 by the then Labor government.

The labor movement in Australia effectively controls the largest portion of managed super, through the ‘Industry Super’ sector, where employer contributions generally end up, which runs ‘Industry funds’. They initially arose from the union movement, with a focus on particular industries, but are now broadly offered to all.

The ‘not-for-profit’ industry funds now manage A$818 billion and are built around low fees of around 1% pa. The broad view of the left is that contributions must be mandated, and that the fees charged by for-profit managers are a theft of workers’ eventual retirement pot.

The Conservatives have a different view. Generally, they hate the industry funds because of their union roots — and the competition they create for retail funds managers, who are traditionally aligned with the political right.

That’s why the conservative government has commissioned a series of inquiries structured to give it the ammunition it needed to fight industry fund growth & influence.

One report has questioned the wisdom of workers stashing even more retirement savings when wages growth is stagnant. Another found that while the current system is effective, further increases in super payments would result in lower wages growth and affect living standards during people’s working lives.

The latest report also noted that a number of vested interests have grown increasingly powerful as a result of superannuation, which generates a staggering $AU30 billion fees in fees each year.

On this occasion the Conservatives appear to have lost heart to pursue a change to the legislated contribution increase, after losing the public argument to a very effective advertising campaign by industry funds.

Conflicted advice

The compounding growth in super has certainly created a large and thriving financial services sector. It’s built around banks, asset managers, consultants, wealth distribution platforms, and financial advisory networks.

Sadly, though, the industry is riddled with conflicts of interest.

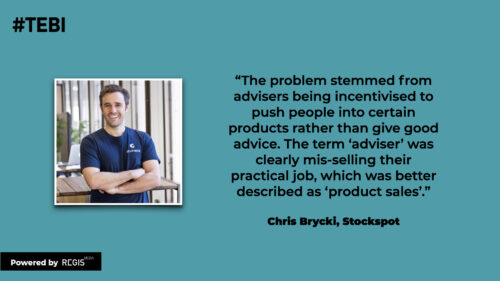

“The problem,” says Chris Brycki, founder of robo-adviser Stockspot, “stemmed from financial advisers, including those at the big four banks and (the fund management company) AMP, being incentivised to push people into certain products rather than give good advice.

“To me this broke their fiduciary duty to their clients. The term ‘adviser’ was clearly mis-selling their practical job, which was better described as “product sales”.

For Brycki, the most obvious example of this focus on sales has been the use of Approved Product Lists, or APLs, which are similar to the recommended fund lists produced by Hargreaves Lansdown and other B2C platforms in the UK. These are marketed as lists of carefully researched funds from which their advisers can make recommendations, but in reality, says Brycki, “they are a thinly veiled way to ensure they can earn revenue on every part of the transaction.”

Unfortunately, low-cost index funds and ETFs are usually not included in these lists because they won’t pay banks for distribution — even though the evidence shows that those are the products that most investors should be using.

“Rather than cut costs and re-invent themselves to adjust to this reality,” says Brycki, “the banks and AMP doubled down on their outdated models by investing hundreds of millions on more bells and whistles for their distribution platforms. This may be helpful for their advisers, but is in no way better for clients.”

What about the Royal Commission?

There were hopes that the damning report of the Royal Commission into Australia’s financial services industry would help to address some of these conflicts.

The report, published in February 2019, found that customers were routinely charged for services they never actually received, and sold products they didn’t need. The extreme examples had life insurance premiums charged against dead customers account balances. It also highlighted a culture of greed, fuelled by huge sales bonuses, which generally led to poor consumer outcomes.

But politics again looms large in this story.

For many years the current Prime Minister and Treasurer consistently rejected calls for a Royal Commission into the banks — denying that there was even a hint of a problem. It was only when they faced losing a vote in Parliament over establishing a commission that they reluctantly agreed

It is of little surprise then that two years on from the report, 45 of the Royal Commission’s 76 recommendations have not be implemented. Four have been abandoned. Gerard Brody from the Consumer Action Law Centre told the newspaper that the government was “just walking away from some of the core recommendations”.

Coronavirus has played a part in this inertia — possibly a rather convenient part, for a government that really just wants to forget.

Last year, the Australian Securities and Investments Commission (ASIC) delayed implementation of the recommendations for which it is responsible up to six months, citing the Covid-19 crisis. The pandemic also meant parliament was unable to sit for long periods, delaying the progress of legislation.

But with life in Australia now almost back to normal, there are no signs that addressing conflicts of interest in financial services is back on the agenda.

Lobbying drives action

If political lobbyists were basketballers each Australian bank could boast an entire team filled with Michael Jordans. They can open every door in Parliament on the left and right – they are feared, heard and influential.

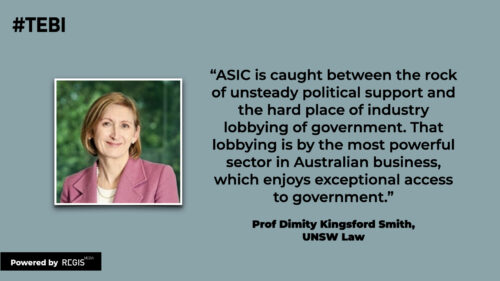

In a recent article in the Australian Financial review, financial regulation expert Professor Dimity Kingsford Smith, said ASIC finds itself caught “between the rock of unsteady political support and the hard place of industry lobbying of government”.

That lobbying, she said, “is by the most powerful sector in Australian business, which enjoys exceptional access to government. The leading lights are four of the six top Australian corporate taxpayers.”

The banks, of course, claim to have acted on the Royal Commission’s findings.

It is true that they were publicly contrite — and that they are paying reportedly almost A$10 billion in remediation for past sins (mind you, not by choice). It’s also true that a number of sacrifices were offered up at both senior executive and board levels.

The Commission’s findings also triggered an unwinding of the ‘vertical integration’ model, which Australian banks had pursued for almost 30 years, that saw the bank become the manager, product issuer and employer of the advisory sales-force. This model never delivered the super-profits it promised, while the commission revealed it exposed them to multiple levels of culpability.

Banks have rapidly divested the wealth management and advisory arms — removing the any future liabilities from their balance-sheets. It was easy for banks to carve off a few rogue divisions, as their core business remained intact. But they are not out of selling financial products, with several immediately doing distribution deals with the purchasers of their former assets.

But AMP had nowhere to hide — its only business is that vertically-integrated, conflicted model. That’s why it has been dying a slow death, with its carcass soon to be divided.

Meanwhile, the banks’ lobbyists are back in Canberra — as are their counterparts from the increasingly powerful industry fund sector.

As always in Australia, pension policy is a political football. And a 1% fee on almost one trillion dollars buys you a lot of good head kickers.

Rewards for failure

Meanwhile, there is no end in sight to excessive boardroom pay. Take AMP, for example. The company has lurched from one scandal to another over the last 12 months, and now it has emerged that two senior executives involved have received huge pay-offs.

Boe Pahari was paid more than $1.3 million for the 53 days he served as CEO of AMP Capital before stepping down over allegations of sexual harassment. Alex Wade was paid around $3.5 million for the ten months he served as CEO of AMP Australia, before resigning last August after a series of complaints about explicit photos.

“The dismal performance of the business over a long period of time damns the board and management more than I or any analyst could ever do,” analyst Gaurav Sodhi told Yahoo Finance.

“Here is a company shown to be acting poorly for its customers and that has already lost billions for its shareholders. Is it really a surprise to see large, questionable remuneration being paid to executives? I’d say it fits the script rather perfectly of an organisation that has been poorly run and in decline for a long time.”

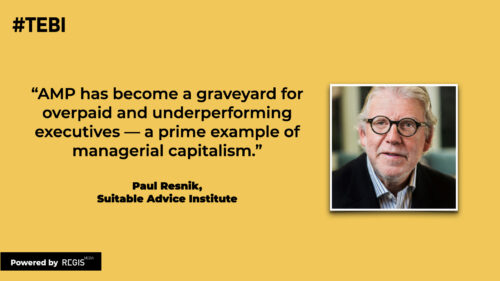

Those sentiments are shared by Suitable Advice Institute founder Paul Resnik. AMP, says Resnik, has become “a graveyard for overpaid and underperforming executives — a prime example of managerial capitalism.”

Conclusion

Australia, then, should be applauded for its superannuation system. There are further improvements in the pipeline too. From July 1st this year, reforms will be introduced aimed at improving efficiency, reducing fees and holding super funds to account for underperformance.

Another reason why Australia deserves credit is the fact that it had a Royal Commission in the first place. The UK government and regulator, by contrast, have refused to hold an independent inquiry into the Neil Woodford scandal which encapsulates the dysfunctional nature of the investing industry in Britain.

But there’s still plenty of room for improvement. As recent developments at AMP show, parts of the system remain rotten to the core. Without fundamental reform, investors will continue have a large proportion of their returns siphoned off by product providers and other third parties who do very little to earn it. Australians surely deserve better than that.

PREVIOUSLY ON TEBI

Be prepared for the next black swan

Why even Buffett has been buffeted by the index

How to manage your cashflow properly

Why financial wellbeing matters

Are we in a financial asset bubble?

How useful are risk tolerance questionnaires?

The case for looking beyond the S&P 500

Is ESG a factor like size or value?

WOULD YOU LIKE TO PARTNER WITH US?

TEBI’s work would not be possible without the support of our strategic partners, to whom we are very grateful.

We currently has three partners in the UK:

Bloomsbury Wealth, a London-based financial planning firm;

Sparrows Capital, which manages assets for family offices and institutions and also provides model portfolios to advice firms; and

OpenMoney, which offers access to financial advice and low-cost portfolios to ordinary investors.

We also have a strategic partner in Ireland:

PFP Financial Services, a financial planning firm in Dublin.

We are currently seeking strategic partnerships in North America and Australasia with firms that share our evidence-based and client-focused philosophy. If you’re interested in finding out more, do get in touch.

Image: Vectors via Unsplash

© The Evidence-Based Investor MMXXI

Robin is a journalist and campaigner for positive change in global investing. He runs Regis Media, a niche provider of content marketing for financial advice firms with an evidence-based investment philosophy. He also works as a consultant to other disruptive firms in the investing sector.