By JOACHIM KLEMENT

In the world of business, I don’t think there is any job where in some instances the incentives for an employee or business owner are not in conflict with the ethically right thing to do. Doctors have an incentive to prescribe certain drugs even though they know that another drug may be more effective or has fewer side effects. Lawyers have an incentive to drag a lawsuit out for longer even though they know it could potentially be resolved. Financial advisers have an incentive to recommend some products even though these products may be riskier than others.

This is not evil capitalism in action. It is simply impossible to create incentive systems that are always fair and never create conflicts of interest. And the people who work in these businesses are not evil or deceptive. The vast majority are ethical and honestly believe they give the best advice they can.

Deceiving themselves first

So, what happens when advisers give advice that may not be in the client’s best interest? According to a new study Uri Gneezy and his colleagues, many advisers have to deceive themselves before they can deceive their clients. In other words, they have to make themselves honestly believe that the course of action they recommend is indeed the best advice possible.

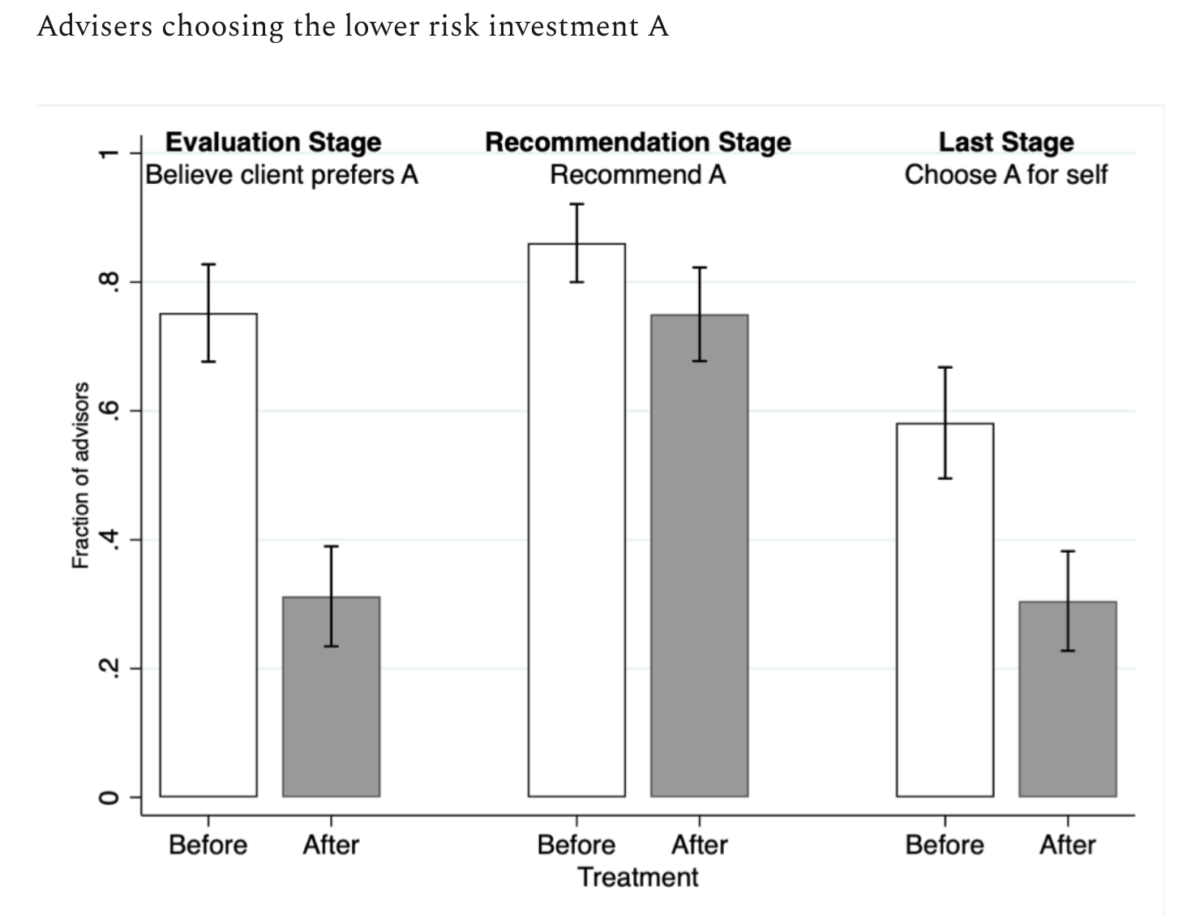

To show how this self-deception works they did a series of experiments where financial advisers were asked to look at two products A and B with different risk and return characteristics. In the initial setup, product A was less risky than product B but also had lower expected returns (think a bund fund vs. an equity fund).

Then, people were randomly selected into three situations. In the control group, the advisers had to simply evaluate which one of investments A and B would be more suitable for their client and then recommend it to a client. They were also asked which of the two investments they would choose for themselves. In the “before” treatment, the advisers were informed that they get an extra incentive in the form of a bonus if they recommend investment A to the client but no bonus if they recommend investment B. Then they were again asked to evaluate which investment they thought was more suitable for their client, recommend an investment, and then decide which investment they would choose for themselves. Finally, in the “after” treatment, the advisers were told about the incentive to recommend investment A only after they had assessed if A or B were more suitable for the client.

The chart below shows how many advisers chose investment A in each situation.

Source: Gneezy et al. (2020)

If we look at the “after” treatment, the cynical observer immediately notices how few advisers think that investment A is the best choice for the client, but once they are made aware of the incentive to recommend A, the number of advisers who do recommend A increases dramatically. Yet, when asked what they would prefer for themselves, very few would invest in A.

Fair enough, but that’s not how incentives work in real life. Instead, they work more like in the “before” case. There, the advisers know about the incentive to recommend investment A before they think about what is best for their client, and hence a larger number of advisers think that investment A is indeed better for them. They afterward go on and recommend investment A to their clients. But look at what happens when they are asked to invest in A or B? 60% of the advisers choose to invest in A, a much larger number than in the “after” treatment. They really believe that investment A is the better investment and they would buy it for themselves.

In successive experiments, the researchers increase the stakes and the interesting thing is that advisers would gladly buy an inferior investment for themselves and recommend them to their clients as long as they have some way to justify to themselves and their clients that investment A really is the better and more suitable investment. Only when it becomes absolutely impossible to deceive themselves do advisers give in and stop recommending the incentivised product. Few advisers are comfortable with lying to their clients. And that is a good thing.

I have previously written about how advisers recommend to their clients what they invest in themselves — often to the detriment of the client’s performance. But in the light of this research, it appears to me that this is just a natural outcome of us being human and being able to look ourselves in the mirror.

We’re all guilty of it

And before you think that advisers are anyway crooks who have learned to deceive themselves to keep up their self-image, ask yourself what incentives you have in your job that may be in conflict with your clients’ best interests? How do you resolve these conflicts?

I know that I have been guilty of self-deception in the past and I might be today. I am trying my best to live up to my fiduciary duty and give the best advice to my clients I can (which in my current job means recommending the best stocks possible and being transparent about the performance of my recommendations). But I have no way of knowing if I am deceiving myself.

And if you read these lines and think to yourself you are not guilty of this, I would say there is a pretty good chance you are deceiving yourself into thinking that. Because we all are deceiving ourselves in one way or another.

JOACHIM KLEMENT is a London-based investment strategist. This article was first published on his blog, Klement on Investing.

ALSO BY JOACHIM KLEMENT

Transparency is good for business for asset managers

Another sign that market efficiency is increasing?

How hard is it to find the next Amazon?

Practitioners still pay too little attention to academia

Stocks have lagged bonds since 1970. Why?

No more room at the factor zoo

PREVIOUSLY ON TEBI

What happens AFTER fund managers crush it?

Woodford: Was the writing on the wall at Invesco?

Do you really want to be a landlord?

Even smart people make mistakes

Is your star striker really a “top investor”?

OUR STRATEGIC PARTNERS

Content such as this would not be possible without the support of our strategic partners, to whom we are very grateful.

We currently have three partners in the UK:

Bloomsbury Wealth, a London-based financial planning firm;

Sparrows Capital, which manages assets for family offices and institutions and also provides model portfolios to advice firms; and

OpenMoney, which offers access to financial advice and low-cost portfolios to ordinary investors.

We also have a strategic partner in Ireland:

PFP Financial Services, a financial planning firm in Dublin.

We are currently seeking strategic partnerships in North America and Australasia with firms that share our evidence-based and client-focused philosophy. If you’re interested in finding out more, do get in touch.