Mention the value premium to investors and chances are their eyes will glaze over. Most have never heard of it — and many who have head of it probably can’t remember what it is.

But, believe us, this stuff is important, so please bear with us while we give you a quick update.

This article was produced for Global Systematic Investors, an evidence-based fund management company that combines systematic factor investing with an ESG overlay.

OK, just remind me what the value premium is.

Academic researchers have shown that, in the long run, value stocks have historically produced higher returns than stocks trading at higher prices, otherwise known as growth stocks. This pattern is known as the value premium.

The value premium has been shown to be persistent over time, cost-effective to capture and prevalent across markets. Over time, therefore, portfolios that have a heavier weighting in value stocks should outperform the broader stock market.

Ah yes, I remember now. So, how have value stocks performed in recent years?

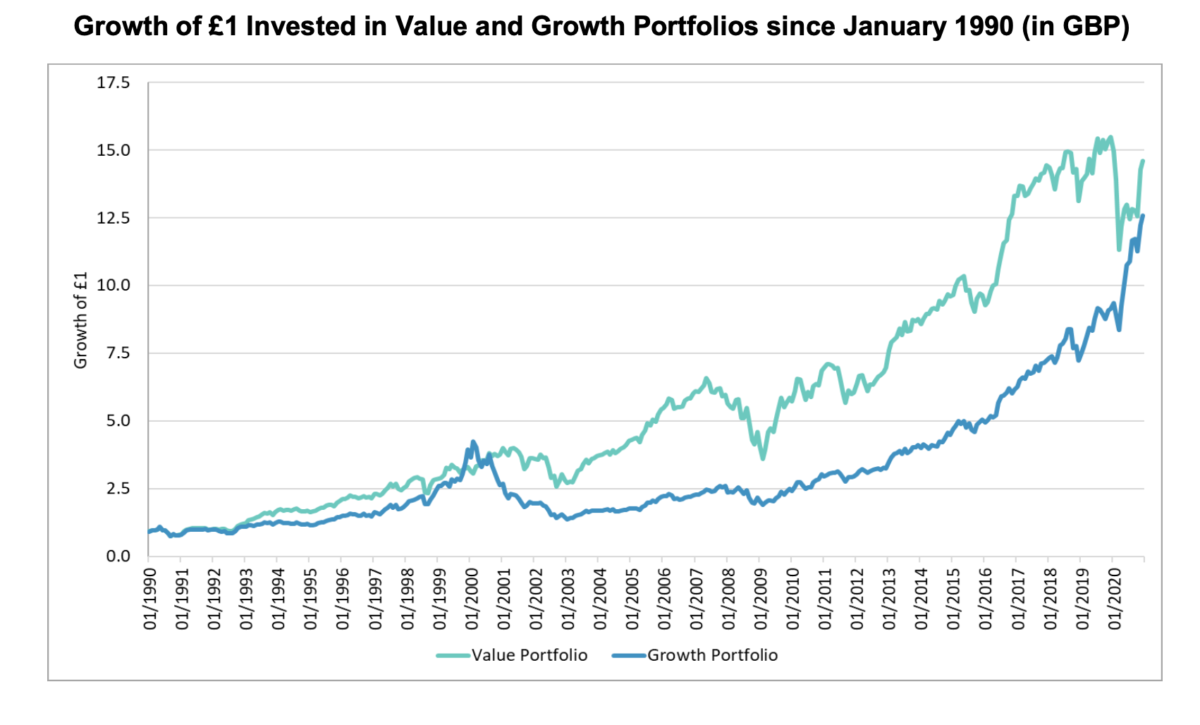

They’ve done OK. Apart from the occasional steep decline like the one we saw in March last year, equities generally have been on an upward trajectory since the end of the global financial crisis. Since the start of 2010, value stocks specifically have performed in line with their longer-run average since 1990 (8.7% vs. 9.0%).

That said, growth stocks have been doing even better. As you can see from the chart below, they have outperformed value stocks since the year 2000. In other words, investors with a heavier exposure to value stocks have not seen any benefits for the last two decades.

Source: GSI

Source: GSI

What about recently? How did value compare with growth in 2020?

Yet again last year, growth stocks produced a higher return than value stocks. Interestingly, this was largely driven by the so-called FAANG stocks — Facebook, Apple, Amazon, Netflix, and Google (now called Alphabet). As you can imagine, these technology stocks benefited greatly from the global pandemic and the fact that most of us were stuck at home for long periods.

Another standout case was Tesla, which rose 743% during 2020. This may have been partly driven by its inclusion in the S&P 500 index, which meant that US index funds that are benchmarked to this index had to buy it, even at what was widely regarded as an elevated price.

Hmmm… I’ve got value funds in my own portfolio. Is this something I should be worried about?

For an investor, worrying is never a good idea. The important thing is to stay rational and focus on the long term.

There are no guarantees in equity investing, and it’s by no means certain that value stocks will produce long-term outperformance in the future. But successful investing is all about putting the odds in your favour. On average, since 1927, value has provided a premium in the region of 4% a year. It’s highly likely that the value premium will reappear at some stage, and possibly sooner than you think.

You’re always going on about evidence. Is there any evidence to back that up?

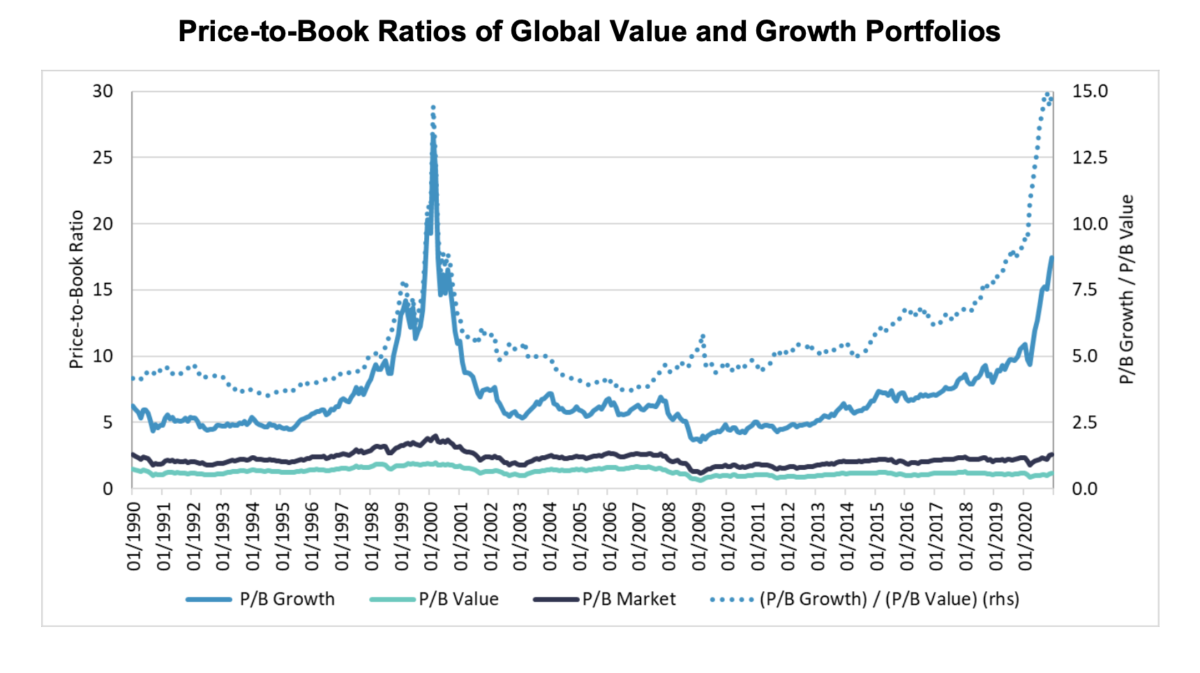

Well, a useful guide to future expected returns is what we call the price-to-book (or P/B) ratio. Simply put, the P/B ratio measures the market’s valuation of a company relative to its book value.

You’ll see from the chart below that the P/B ratio of growth stocks has been trending up since the onset of Quantitative Easing (QE) in early 2009. However, in 2020, the price of growth stocks was pushed up much further so that their weighted average P/B ratio at the end of the year was 17.4. This compares to a long-run average of 7.0 since 1990. Though somewhat below the peak of 26.6 reached in February 2000 during the tech boom, 17.4 is still very high.

Source: GSI

Source: GSI

Ah, so what you’re saying is that, compared to growth stocks, value stocks appear to be relatively cheap?

By historical standards, yes — that’s certainly what the relative P/B ratios suggest. But again, there are no guarantees when it comes to future performance.

Whether the valuation spread between growth and value stocks continues depends on things we can’t predict with any uncertainty. For example, will the new Biden administration have any impact on the strong earnings and dominant positions of those FAANG stocks we mentioned? And for how much longer will interest rates remain at such low levels?

Because investors are human, they naturally tend to attach more weight than they should to the recent past. We call that recency bias. One of the most important lessons from market history is that nothing lasts for ever. And that includes the seemingly ever-increasing valuation spread between growth and value.

Should I just sit tight, then?

As we always point out, we are not financial advisers, and we strongly encourage people to seek the help of an adviser before making any significant changes to their portfolio.

Suffice it to say, abandoning value now is probably not a shrewd move. And for those who don’t yet have exposure to value stocks, this might turn out to be an excellent time to talk to their adviser about getting some.

PREVIOUSLY ON TEBI

Baroness Altmann: UK investors need better protection

Trading on a phone increases risk-taking, study finds

Three things to remember about emerging markets

12 common mistakes people make with money

Is equal weighting worth considering?

How do target-date funds affect the markets?

Does a well-paid job make you happy?

People need advisers because they’re human

Is there a whelk in your fund portfolio?

CONTENT FOR ADVICE FIRMS

Through our partners at Regis Media, TEBI provides a wide range of content for financial advice and planning firms. The material is designed to help educate clients and to engage with prospects.

As well as exclusive content, we also offer pre-produced videos, eGuides and articles which explain how investing works and the valuable role that a good financial adviser can play.

If you would like to find out more, why not visit the Regis Media website and YouTube channel? If you have any specific enquiries, email Sam Willet, who will be happy to help you.

Picture: Andrea Piacquadio via Pexels

© The Evidence-Based Investor MMXXI